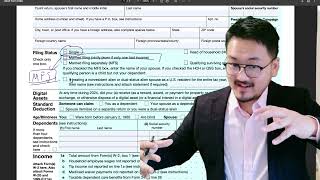

Married Filing Separately: When and Why to Choose MFS

Key Takeaways

- MFS separates tax liability — each spouse is only responsible for their own return

- Best for: distrust situations, pending divorce, or one spouse's aggressive tax positions

- Can optimize medical deductions when one spouse has low income and high bills

- Community property states may require splitting income 50/50 even with MFS

- Always run the numbers both ways before choosing MFS

Legal and Liability Reasons for MFS

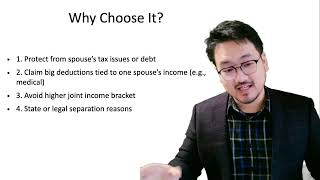

The primary reason to choose MFS is to separate tax liability between spouses. Under MFJ, both spouses are jointly and severally liable for the entire tax on the return. If one spouse has unreported income, aggressive deductions, or potential audit issues, the other spouse can be held liable for the entire resulting tax, interest, and penalties.

MFS eliminates this risk — each spouse is only responsible for their own return. This is particularly relevant in situations involving distrust, pending divorce, or when one spouse's business activities create uncertain tax positions.

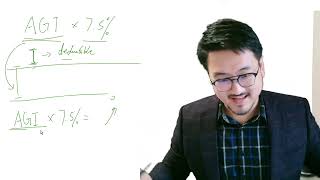

Medical Expense Optimization

The second major reason for MFS is medical expense optimization. When one spouse has a very low income and high medical bills, MFS lowers their AGI threshold, making more of the medical expenses deductible. The math must be run both ways, as the benefits of higher medical deductions must outweigh the costs of lost credits and narrower brackets.

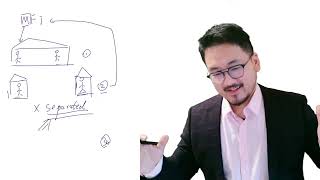

Community Property State Complications

In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin), income earned during the marriage may need to be split equally between spouses even when filing separately. This can significantly complicate MFS calculations and reduce its benefits.

Frequently Asked Questions

Is MFS a red flag for audits?

MFS itself is not an audit trigger. However, because it is less common, some IRS systems may apply additional scrutiny. The decision should be based on tax savings and liability protection, not audit concerns.

Can we switch from MFS to MFJ later?

Yes. You can amend from MFS to MFJ within 3 years of the original due date. However, you generally cannot switch from MFJ to MFS after the filing deadline.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Filing Status Guide

9:51

9:51Married Filing Separately: MFS Tax Calculation with Medical Bills and AGI Changes

5:58

5:58Married Filing Separately: Pros and Cons of MFS Filing Status

5:15

5:15Married Filing Separately (MFS): Introduction and Overview

5:43

5:43Filing Status Comparison: Single vs Married Filing Jointly vs Separately

4:23

4:23Same-Sex Spouse Filing Status: IRS Rules for Married Couples

4:08

4:08