Installment Sales (Form 6252) for Foreign Sellers of US Assets

How the IRC section 453 installment method actually works for foreign sellers of US real estate, businesses, and partnership interests — the gross-profit ratio, Form 6252, the FIRPTA full-withholding-at-first-payment trap, recapture, related-party and section 453A rules, imputed interest, and California sourcing.

Disclaimer: This is independent research and educational analysis, compiled from IRS Publication 537, Form 6252 and its instructions, the Form 8288 and 8288-B instructions, the IRS FIRPTA and partnership-withholding pages, and the Internal Revenue Code, current to mid-2026. It is not legal or tax advice. Installment sales by foreign sellers turn on intensely fact-specific questions — asset characterization, treaty position, withholding certificates, and state sourcing — and applicable federal rates and the section 453A thresholds change. Anyone selling a US real property interest, business, or partnership interest on the installment method should consult a qualified attorney or tax adviser before signing.

Key Takeaways

- The installment method under IRC section 453 lets a seller spread gain across the years payments are received: each principal dollar is split into return of basis and gain using the gross-profit ratio (gross profit divided by contract price). Stated interest is always reported separately as ordinary income.

- It is not available for dealer or inventory sales, for publicly traded stock and marketable securities (section 453(k)), or for a loss — and depreciation recapture (sections 1245/1250) is recognized in full in the year of sale under section 453(i), no matter how slowly cash arrives.

- For U.S. real estate, FIRPTA sits on top of section 453: absent a withholding certificate, the buyer must withhold the full 15% of the entire amount realized at the first payment — not 15% per installment. Form 8288-B is the relief valve that lets the IRS approve installment-based withholding.

- Partnership-interest sales are the least forgiving: section 864(c)(8) can make part of the gain effectively connected, section 1446(f) can require 10% withholding on amount realized, and section 897(g) independently reaches the U.S.-real-property piece.

- Watch the accelerators: related-party rules in section 453(e)/(f)/(g), the section 453A interest charge and pledge rule (sales price over $150,000 and obligations over $5 million), imputed interest under sections 1274/483 (with no 6% cap when a party is a nonresident alien under 483(e)(4)), and California's aggressive installment sourcing.

1. Why section 453 is only one layer for a foreign seller

Section 453 is the baseline deferral rule for any sale of property where at least one payment is received after the close of the tax year of the sale. The mechanics — the gross-profit ratio applied to each payment — are the easy part. For a foreign seller, the hard part is the overlay of rules stacked on top: FIRPTA for U.S. real property, section 864(c)(8) and section 1446(f) for partnership interests, depreciation recapture, related-party acceleration, imputed interest, and state sourcing. Form 6252 is one layer of the compliance stack, not the whole analysis.

Reporting follows the seller's federal tax classification, because Form 6252 is attached to the seller's own return. The IRS lists Form 1040-NR and Form 1120-F among the returns used with Form 6252, so a foreign individual generally reports on 1040-NR, a foreign corporation on 1120-F, and a fiscally transparent structure pushes the economics to the owner. Withholding never excuses the foreign transferor from filing a U.S. return for the sale.

The asset class drives everything downstream. A direct U.S. real-estate sale sits inside sections 453, 897, and 1445. A business sale usually needs an asset-by-asset allocation, so land, building, and goodwill can stay in the installment pool while inventory and recapture items fall out. A partnership-interest sale brings in section 864(c)(8) and section 1446(f), with section 897(g) layered on where the partnership holds U.S. real property. Identify the asset class before deciding which withholding track applies.

2. Core installment-method mechanics

Gross-profit ratio, contract price, and year-by-year gain

Section 453(c) recognizes, in each year, the same proportion of the payments received that year as gross profit bears to total contract price. Publication 537 and Form 6252 break each installment into three components: interest, recovery of basis, and gain. Interest is always reported separately as ordinary income and never enters the selling price used on Form 6252.

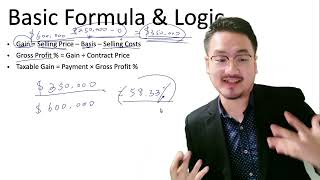

The practitioner formula falls out once the inputs are right. Start with selling price, including liabilities the buyer assumes, but excluding stated or unstated interest. Compute adjusted basis, add selling expenses, and add any recapture shown through Form 4797 Part III — that is the installment-sale basis. Gross profit is selling price minus that basis. Contract price generally strips out the assumed liabilities, except to the extent liabilities exceed basis, in which case the excess is treated as a payment in the year of sale. The gross-profit percentage is gross profit divided by contract price, and each year's installment gain is principal received times that percentage.

The regulations' classic mortgage example shows it cleanly. A seller with a $160,000 selling price, a $60,000 mortgage assumed by the buyer, and a $90,000 basis has a $100,000 contract price and $70,000 gross profit, so the ratio is 70%. Each $10,000 of principal then produces $7,000 of gain and $3,000 of basis recovery, while stated interest stays ordinary income outside the fraction.

Contingent-price deals need extra care. Form 6252 line 4 asks whether total selling price can be determined by the close of the year of sale; a No pushes you into Temporary Regulation section 15a.453-1(c), which can require stated-maximum-selling-price rules or ratable basis recovery and a recomputed ratio as facts develop. For foreign sellers exiting earnout-heavy U.S. businesses, this is often where the tax model first breaks from the purchase agreement.

3. The foreign-seller timing trap — section 864(c)(6) and (c)(7)

A critical trap sits outside section 453. Section 864(c)(6) says deferred income or gain is tested as if it were recognized in the year of the underlying sale, not the later year the cash arrives. Section 864(c)(7) has a parallel rule for certain property that ceases to be used in a U.S. trade or business and is sold within ten years.

The practical effect: if the gain would have been effectively connected in the year of sale, later installment payments stay inside the U.S. tax net even if the foreign seller has since changed activities, wound down operations, or is no longer engaged in a U.S. trade or business in the collection year. You cannot defer your way out of effectively-connected character simply by stretching the note over quiet years.

4. When the installment method works — and when it does not

The method applies by default unless the seller elects out under section 453(d), but several categories are removed entirely. Section 453(b)(2) excludes dealer dispositions and inventory of personal property. Publication 537 says the same: regular inventory sales do not qualify, and real property held for sale to customers in the ordinary course fails too — except the specialized timeshare and residential-lot regime in section 453(l), which permits installment reporting only if the seller pays an additional interest charge.

Publicly traded stock and marketable securities are a hard stop. Section 453(k) says the installment method does not apply to obligations from sales of stock or securities traded on an established market; the full gain is reported in the year the trade date controls. For a foreign owner selling publicly traded U.S. stock, that usually means no installment deferral even before any treaty or FIRPTA analysis.

Loss sales do not qualify. Both Publication 537 and the Form 6252 instructions say you cannot report a loss on the installment method — a loss on business or investment property belongs in the year of sale, not spread forward.

Depreciation recapture is not a full disqualifier but a character override that strips deferral from the ordinary-income slice. Section 453(i) requires section 1245 and 1250 recapture income to be recognized in the year of disposition, even though the excess gain can still use the installment method. Form 6252 line 12 pulls that recapture from Form 4797 Part III into Part I. For partnership-interest sales, section 453(i)(2) also reaches the portion of section 751 ordinary income tied to sections 1245 and 1250.

- Dealer / inventory property — excluded by section 453(b)(2) and Publication 537.

- Publicly traded stock / marketable securities — excluded by section 453(k); report full gain at the trade date.

- Loss sales — cannot use the method; the loss is recognized in the year of sale.

- Depreciation recapture (1245/1250) — recognized in full in the year of sale under section 453(i), even though the rest of the gain defers.

- Related-party sales of depreciable property — section 453(g) generally treats all payments as received in the year of sale (subject to a no-tax-avoidance exception).

5. Form 6252 in practice

Parts I, II, and III — and the liability-over-basis deemed payment

Form 6252 is filed for the year of disposition and every later year until the final payment is received or the obligation is otherwise disposed of — even in a year with no payment. A separate form is used for each sale, and for a sale to a related party, Part III stays alive for the year of sale and the next two years unless the final payment has already been received.

Lines 1-4 identify the property, dates, related-party status, and whether the total selling price is determinable by year-end. These are not throwaway boxes for a foreign seller: a Yes on the related-party line can turn on section 453(e) acceleration and ongoing Part III reporting, and a No on line 4 should push you into the contingent-payment rules.

Part I builds gross profit and contract price. Line 5 is selling price (including mortgages and debts, excluding interest); line 6 is liabilities assumed; lines 8-10 are basis and adjusted basis; line 11 is selling expenses; line 12 is recapture from Form 4797 Part III; line 16 is gross profit; line 18 is contract price. Line 17 is the liability-in-excess-of-basis adjustment, which feeds line 20 as a deemed payment in the year of sale — one of the most common and expensive preparation errors in leveraged real-estate deals.

Part II recognizes gain year by year. Line 19 is the gross-profit percentage; line 20 captures the deemed payment from liabilities over basis (year of sale only); line 21 is actual payments received during the year, excluding interest but including money or property received and even amounts withheld to pay off mortgages, broker fees, or legal fees. The buyer's note itself is generally not a payment — unless it is payable on demand or readily tradable. Line 23 picks up prior-year payments and deemed payments, including related-party second-disposition amounts and pledge-rule amounts under section 453A(d).

Part III handles related-party sales: line 27 names the related buyer, line 28 asks whether that buyer made a second disposition in the year, and line 29 tests the statutory exceptions (more than two years later, stock resold to the issuer, involuntary conversion, disposition after death, or no-tax-avoidance). If no exception applies, the form accelerates the remaining gain using the original gross-profit percentage.

6. FIRPTA and withholding on real-estate installments

Why the buyer withholds on the whole price at the first payment

For a foreign seller of a U.S. real property interest, FIRPTA sits on top of section 453. Section 1445 and its regulations generally require the buyer to withhold 15% of amount realized — and amount realized includes cash paid or to be paid, the value of other property transferred, and liabilities assumed or left on the property (principal only for deferred cash; interest and OID are excluded). Section 897 separately treats the underlying gain as effectively connected income.

Here is the crucial installment point: absent a withholding certificate, the buyer generally must withhold the full FIRPTA amount at the time of the first installment payment. The current Form 8288 instructions say exactly that, and warn that if the first payment lacks enough cash or liquid assets, the parties should obtain a withholding certificate. “15% on each installment” is not the default federal rule — the default is full withholding on the entire amount realized, with the cash-flow problem pushed to Form 8288-B.

Form 8288-B is the relief valve. Its instructions say the IRS will consider a withholding certificate for a nondealer transferor using the installment method under section 453, and that any installment-based certificate will account for the section 453A(c) interest charge when applicable. The structure the IRS will consider: withhold 15% (or a lower IRS-approved amount) on the down payment — which expressly includes assumed liabilities — withhold on each later payment, pay the deferred-tax interest when applicable, remit via Forms 8288 and 8288-A, and continue under the reduced certificate even if the seller later pledges the obligation.

The operational forms matter. Form 8288 is the remittance return filed by the buyer or withholding agent; Form 8288-A is completed for each person subject to withholding, generally filed and paid by the 20th day after the transfer. The IRS stamps Copy B and sends it to the foreign seller, who attaches it to Form 1040-NR or 1120-F (or an early-refund request) to claim credit. A seller who needs an ITIN may submit Form 8288-B together with Form W-7.

7. Related-party, large-obligation, and interest rules

Sections 453(e)/(f)/(g), 453A, and 1274/483 imputed interest

Section 453(e) is the classic two-step anti-deferral rule. If a seller sells to a related person on the installment method and the related person disposes of the property before the seller has collected, the amount realized on that second disposition is treated as received by the seller at the time of the second disposition. For nonmarketable property the rule generally applies only if the second disposition happens within two years of the first, but the clock is suspended while the related person's risk of loss is substantially reduced (puts, short sales, and the like).

Section 453(f) supplies the definitions: “related person” draws on section 318 attribution and section 267(b); a buyer note is usually not a “payment”, but a note payable on demand or readily tradable is treated as payment immediately — a real risk where a foreign seller takes affiliate paper or tries to monetize the note quickly. Section 453(g) is harsher: depreciable property sold on the installment method to a controlled related entity generally falls out of section 453 entirely, with all payments deemed received in the year of sale and no early basis step-up for the buyer.

Section 453A applies to nondealer obligations when the sales price exceeds $150,000 and the aggregate face amount of applicable obligations outstanding at year-end exceeds $5 million. When it bites, the seller owes an interest charge on the deferred tax, using the section 6621 underpayment rate on the applicable percentage of deferred tax. The pledge rule in section 453A(d) — often missed in private-credit exits — treats net loan proceeds as a payment when the debt becomes secured by the installment obligation: borrowing against the note is usually the economic equivalent of collecting it.

Sections 1274 and 483 recharacterize part of stated principal as interest when the paper lacks adequate stated interest, using AFR-based present-value tests. The seller-side effect: reduce the stated price by the unstated-interest or OID component, report that piece as interest income, and use the reduced principal for the installment math. One foreign-person nuance deserves emphasis: section 483 caps the discount rate at 6% for certain intrafamily land sales, but section 483(e)(4) removes that 6% cap when any party to the sale is a nonresident alien individual. Foreign sellers who copy domestic family-transfer templates routinely understate interest income here.

8. Note cancellation (453B) and the section 1031 interaction

Section 453B accelerates gain or loss when an installment obligation is satisfied at other than face value, distributed, sold, or otherwise disposed of. The seller's basis in the obligation is its face amount minus the income that would be returned if the note were paid in full. If the obligation is canceled or becomes unenforceable, section 453B(f) treats that as a non-sale disposition — and if obligor and obligee are related, the note's value cannot be treated as less than face. For foreign family or affiliate structures, forgiving the note is usually a taxable acceleration event, not a free cleanup step.

The section 1031 interaction is narrow but important. Under section 453(f)(6) the installment computation is adjusted for like-kind exchanges, and the deferred-exchange regulations ignore a properly structured qualified intermediary as the seller's agent for section 453 payment purposes. But if the taxpayer ultimately receives the buyer's installment note out of the exchange, that note is boot for section 1031 and a purchaser obligation for section 453. In plain English: a qualified intermediary preserves exchange treatment during the exchange window, but a buyer note received out of the exchange becomes taxable property rather than like-kind replacement real estate.

9. Partnership interests and California sourcing

A foreign seller may assume “this is not real estate, so only section 453 matters” — and be wrong. Section 864(c)(8) can make part of the gain on a partnership-interest sale effectively connected; section 1446(f) can require the transferee to withhold 10% of amount realized unless an exception applies; and section 897(g) independently pulls in the U.S.-real-property component. Section 864(c)(8)(C) prevents double counting by reducing the 864(c)(8) amount by the portion already taxed under section 897. If the partnership holds depreciated U.S. assets, the 1245/1250 recapture overlay must be modeled too. These deals combine pass-through tax, withholding, and asset-level look-through — among the least forgiving installment transactions for foreign owners.

California is unusually assertive on installment sourcing. FTB Publication 1100 sources real-property gain by the location of the property and intangible-property installment gain generally to the seller's state of residence at the time of sale — so a nonresident keeps owing California tax on later payments from California real estate, and a former California resident can keep owing California tax on later installment gain from stock sold while resident. California also runs its own withholding regime: the FTB 3805E instructions require buyers to withhold on the principal portion of each installment unless the seller elects out by reporting the full gain in the year of sale and receives an FTB release letter.

California adds an apportionment twist for multistate businesses: Legal Ruling 413 says the year-of-sale payroll, property, and sales factors — not the later year-of-payment factors — control the apportionment of installment gain. That matters when a foreign seller disposes of a California-connected business and then collects after the in-state footprint has disappeared; California holds on to the original sourcing footprint.

Asset class vs withholding track, at a glance

| Asset sold | Installment method? | Withholding overlay | Relief / key trap |

|---|---|---|---|

| US real estate (direct) | Yes (section 453), recapture in year of sale | FIRPTA 15% of amount realized (sections 897/1445) | Full withholding at first payment unless Form 8288-B certificate |

| US business (asset sale) | Mixed — allocate; inventory and recapture fall out | FIRPTA on any USRPI piece; otherwise none | Section 864(c)(6) keeps ECI gain taxable in later years |

| Partnership interest | Yes for the non-recapture gain; 751 hot assets up front | Section 1446(f) 10% of amount realized | 864(c)(8) ECI + 897(g) USRPI look-through |

| Publicly traded stock | No — section 453(k) bars deferral | Generally none (non-USRPHC) | Full gain reported at the trade date |

| Large note (over $5M outstanding) | Yes, but section 453A applies | As above for the asset class | Section 453A interest charge + pledge rule on borrowing |

Related on ForeignLLCTax

Primary sources

- IRS — About Form 6252 (Installment Sale Income)

- IRS — About Form 6252

- IRS — Publication 537 (Installment Sales)

- IRS — About Form 8288 (FIRPTA withholding return)

- IRS — About Form 8288-B (withholding certificate)

- IRS — FIRPTA withholding (section 1445)

- IRS — Partnership withholding (section 1446(f))

- 26 U.S.C. § 453 — Installment method (Cornell LII)

- 26 U.S.C. § 453A — interest charge & pledge rule (Cornell LII)

- 26 U.S.C. § 864(c)(8) — gain on partnership interests (Cornell LII)