Installment Sales Introduction: Form 6252 Basics

Key Takeaways

- Installment sales spread tax over the period payments are received (Form 6252)

- Prevents paying tax on gains before the cash is actually received

- Gross profit percentage determines the taxable portion of each payment

- Interest received on installment payments is reported separately as ordinary income

- Critical for business owners selling assets, real estate, or business interests over time

What Are Installment Sales?

An installment sale occurs when you sell property and receive at least one payment after the tax year of the sale. Form 6252 allows you to spread your tax liability over the period you actually receive payments, rather than paying all the tax in the year of sale. This can be a significant cash flow advantage for business owners and entrepreneurs.

Why Installment Sales Matter for Cash Flow

One of the most important lessons in running a business is maintaining healthy cash flow. You do not want to owe tax on income you have not yet received. Without the installment method, if you sell an asset for $1 million with payments spread over 5 years, you might owe tax on the entire $1 million gain in year one — even though you only received $200,000.

With Form 6252, you report gain proportionally as payments are received. Your gain is spread over the payment period, matching your tax liability with your actual cash inflow.

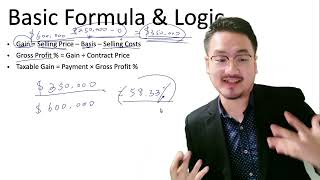

How the Calculation Works

Form 6252 calculates three key numbers: the gross profit percentage (the ratio of your total gain to the total contract price), the payment received in each year, and the taxable portion of each payment (payment multiplied by the gross profit percentage). Interest received is reported separately as ordinary income.

For example, if your gross profit percentage is 40% and you receive a $50,000 payment, you would report $20,000 as gain from the installment sale (50,000 × 40%). The remaining $30,000 represents return of your cost basis and is not taxed.

Frequently Asked Questions

Can all types of property be sold on the installment method?

Most property qualifies, but there are exceptions. Inventory sales, dealer property, and publicly traded stocks and securities generally cannot use the installment method. Depreciation recapture must be reported in the year of sale regardless of when payments are received.

Can I elect out of the installment method?

Yes. If you prefer to report all gain in the year of sale (perhaps to use capital losses or because you expect higher tax rates in the future), you can elect out by reporting the full gain on your return for the year of sale.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Installment Sales (Form 6252)

5:44

5:44Installment Sale Calculation: Step-by-Step Form 6252 Guide

Form 6252 Business Sale Allocation Guide

Form 6252 Business Sale Allocation Guide (2025-2026)

Form 6252 Related-Party Second Sale Guide

Form 6252 Related-Party Second Sale Guide (2025-2026)

Installment Sale Interest and Ineligible Property Guide

Installment Sale Interest and Ineligible Property Guide (2025-2026)

4:55

4:55Form 8938 Introduction: FATCA Foreign Financial Assets Reporting

5:06

5:06