Foreign Tax Credit: Introduction to Avoiding Double Taxation

Key Takeaways

- FTC prevents double taxation by crediting foreign income taxes against your U.S. tax liability

- Credit is dollar-for-dollar — more valuable than a deduction for foreign taxes

- Reported on Form 1116 with separate calculations for each income category

- Excess credits carry forward 10 years and back 1 year

- The FTC limitation formula ensures credits only offset U.S. tax on foreign-source income

What Is the Foreign Tax Credit?

The Foreign Tax Credit (FTC) is the IRS's mechanism for preventing double taxation on income earned overseas. If you earn income in a foreign country and pay income tax to that country's government, the FTC provides a dollar-for-dollar credit against your U.S. tax liability for those foreign taxes paid.

The credit is reported on Form 1116 and is calculated for each category of income (general, passive, etc.) separately. The rules have remained largely unchanged for decades, making this a relatively stable area of tax law.

How the FTC Works

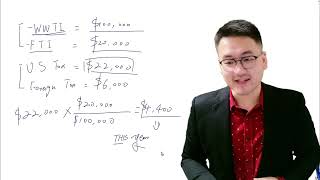

The FTC is calculated using a limitation formula that ensures you only receive a credit up to the amount of U.S. tax attributable to your foreign-source income. You cannot use foreign taxes paid to offset U.S. tax on U.S.-source income.

If you paid more in foreign taxes than the FTC limitation allows, the excess carries forward for up to 10 years (and can carry back 1 year). If you paid less in foreign taxes than the limitation, you can credit the full amount and still owe some U.S. tax on the foreign income.

FTC vs. Foreign Tax Deduction

Instead of claiming a credit, you can choose to deduct foreign taxes paid as an itemized deduction. However, a credit is almost always more beneficial because it reduces your tax dollar-for-dollar, while a deduction only reduces your taxable income. In most cases, the FTC provides greater tax savings.

Frequently Asked Questions

Should I take the foreign tax credit or deduction?

In almost all cases, the credit is more beneficial because it directly reduces your tax bill dollar-for-dollar. A deduction only reduces taxable income, providing less savings. The only scenario where a deduction might be preferred is if your foreign tax credit is limited and you cannot carry forward the excess.

Do I need to file Form 1116 for the foreign tax credit?

Generally yes. However, there is a simplified election available if your qualified foreign taxes are $300 or less ($600 if married filing jointly) and all foreign income is passive. In that case, you can claim the credit directly on Form 1040 without filing Form 1116.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Tax Credits (FTC, GBC)

3:55

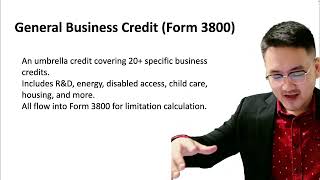

3:55General Business Credit Introduction and Overview

4:28

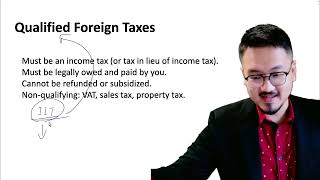

4:28Which Foreign Taxes Qualify for the Tax Credit?

5:15

5:15FTC Allowed Formula: How to Calculate Your Foreign Tax Credit

4:42

4:42Form 3800: Filing the General Business Credit

5:33

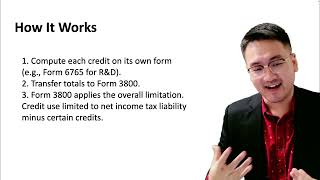

5:33How the General Business Credit Works: Form 3800 Mechanics

6:08

6:08