How the General Business Credit Works: Form 3800 Mechanics

Key Takeaways

- Calculate each credit separately, then combine on Form 3800

- GBC limitation = net tax minus greater of TMT or 25% of net tax above $25,000

- Allowable credit is the lesser of total credits or the limitation

- Excess carries back 1 year or forward 20 years

- Oldest credits are applied first (FIFO order)

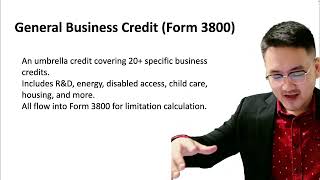

GBC Calculation Process

To calculate your General Business Credit, start by computing each individual credit on its respective form (e.g., Form 6765 for R&D, Form 3468 for energy). Bring each credit amount to Form 3800 and add them together to get your total current-year GBC.

Next, determine your GBC limitation: net income tax minus the greater of your tentative minimum tax or 25% of net regular tax above $25,000. The allowable GBC for the year is the lesser of your total credits or the limitation amount.

Carryback and Carryforward

If your total credits exceed the limitation, the excess is not wasted. You can carry the excess back 1 year (amending the prior year's return) or carry it forward up to 20 years. This flexibility ensures that business credits provide long-term value even in years when your tax liability is insufficient to absorb them all.

Credits are applied in chronological order — oldest carryforwards are used first, then current-year credits, then carrybacks.

Frequently Asked Questions

What is tentative minimum tax (TMT)?

TMT is the tax calculated under the AMT system before subtracting the AMT foreign tax credit. It serves as a floor for the GBC limitation to prevent business credits from reducing tax below the AMT level.

Can the R&D credit be applied against payroll tax?

Yes. Qualified small businesses (under $5 million in gross receipts, with less than 5 years of gross receipts) can elect to apply up to $500,000 of the R&D credit against payroll taxes instead of income taxes.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Tax Credits (FTC, GBC)

4:42

4:42Form 3800: Filing the General Business Credit

6:08

6:08General Business Credit Calculation Example on Form 3800

3:55

3:55General Business Credit Introduction and Overview

3:42

3:42Foreign Tax Credit: Introduction to Avoiding Double Taxation

4:28

4:28Which Foreign Taxes Qualify for the Tax Credit?

5:15

5:15