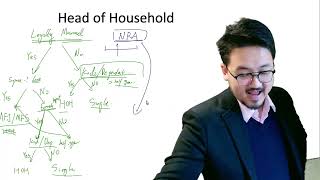

Head of Household Qualifying Person: Special Cases for Kids and Parents

Key Takeaways

- Follow the decision tree step by step — each test must be passed

- Single children living with you 6+ months are the simplest qualifying persons

- Married children add complexity — joint return filing rules apply

- Qualifying relatives must meet relationship, support, income, and household tests

- Evaluate each potential qualifying person separately

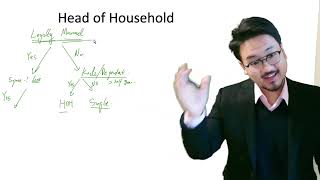

Decision Tree for Qualifying Person Status

Determining whether someone is a qualifying person for HOH requires following a logical decision tree. For children: First, does the child live with you for more than half the year? If yes, proceed to the next tests. If the child is single, they automatically qualify. If married, additional tests apply regarding whether the child files a joint return.

Married Children and Special Cases

A child who is married introduces complexity. If the married child files a joint return with their spouse, they generally cannot be your qualifying person for HOH unless the return was filed only to claim a refund and neither spouse would owe tax filing separately.

For qualifying relatives, the chain of dependency must be established: the person must meet the relationship test, the support test (you provide more than half), the gross income test, and the member of household or relationship test.

Root Dependent Concept

Think of this as a 'root dependent' decision tree — each test must be passed before proceeding to the next. If any test fails, that person cannot be your qualifying person, and you cannot claim HOH based on them. However, other people in your household may qualify, so evaluate each potential qualifying person separately.

Frequently Asked Questions

Can a foster child be a qualifying person?

Yes. A foster child placed with you by an authorized placement agency or court order can be a qualifying child for HOH purposes if they meet the residency and other tests.

What if two people can claim the same qualifying person?

Tiebreaker rules apply. Generally, the parent with the longest residency period with the child takes priority. If both are parents with equal time, the parent with the higher AGI prevails.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Filing Status Guide

6:12

6:12Head of Household: Qualifying Person Rules for Kids and Parents

4:33

4:33Head of Household Qualifying Person: Advanced Rules for Kids and Parents

4:28

4:28Head of Household: Qualifying Person Time Requirements Explained

5:31

5:31Head of Household for Non-Resident Aliens: Fast Decision Guide (Part 2)

8:40

8:40Head of Household Filing Status: Decision Tree Guide (Part 1)

5:21

5:21