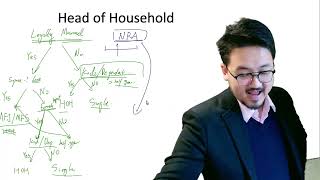

Head of Household: Qualifying Person Time Requirements Explained

Key Takeaways

- Qualifying person must live in your home for more than half the year (183+ days)

- The home must be the qualifying person's principal place of abode

- Temporary absences (school, military, medical, vacation) count as time at home

- Parents are a special exception — they don't need to live with you

- If you pay for a parent's separate home, they can still qualify you for HOH

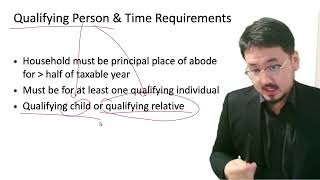

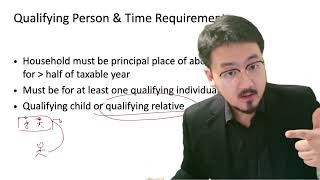

Qualifying Person Time Requirements

To claim Head of Household, you must maintain a household that is the principal place of abode for a qualifying person for more than half the tax year. 'Principal place of abode' means the primary place where the qualifying person lives — not a vacation home or secondary residence.

The 'more than half the year' requirement means more than 183 days for a regular calendar year. Temporary absences for school, military service, medical care, or vacation still count as time living in the household.

Who Is a Qualifying Person?

There are two main categories of qualifying persons for HOH purposes. Qualifying children must live with you for more than half the year and meet age, relationship, and support tests. Qualifying relatives must meet IRS support and relationship rules to be claimed as your dependent.

A special exception exists for parents: they do not need to live in your home to be a qualifying person. If you pay more than half the cost of maintaining their separate home (such as a nursing home), your parent can be a qualifying person for HOH status.

Frequently Asked Questions

What counts as a temporary absence?

School attendance, military service, medical treatment, vacation, and temporary work assignments are generally considered temporary absences. The key is the person intends to return to the home.

Can I claim HOH with a parent in a nursing home?

Yes. If you pay more than half the cost of maintaining your parent's home (including a nursing home), your parent can be a qualifying person for HOH even though they don't live with you.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Filing Status Guide

6:12

6:12Head of Household: Qualifying Person Rules for Kids and Parents

4:33

4:33Head of Household Qualifying Person: Advanced Rules for Kids and Parents

3:55

3:55Head of Household Qualifying Person: Special Cases for Kids and Parents

5:31

5:31Head of Household for Non-Resident Aliens: Fast Decision Guide (Part 2)

5:21

5:21Form 1040 Filing Status: Qualifying Surviving Spouse Explained

6:05

6:05