Pro Forma 1120 + Form 5472: Why the IRS Requires This Filing (Information, Not Tax)

Key Takeaways

- Form 1120 in this filing is a pro forma cover sheet — it carries Form 5472 to the right IRS processing unit

- The IRS isn't taxing these LLCs — they're tracking cross-border money flow through them

- Form 5472 is an information return (like 1099/W-2), not a tax return

- Failure-to-file penalty is $25,000 per missed form — because withheld information, not lost tax, is the harm

- The 1120 + 5472 structure exists because IRC §6038A treats the disregarded entity as a corporation for reporting only

Why the IRS Asks for Form 1120 When There's No Tax to Pay

Form 1120 is the U.S. corporate income tax return. So why does the IRS require foreign-owned single-member LLCs — which generally have no U.S. corporate income tax liability — to file a Form 1120 anyway?

The answer is in the word "pro forma." In this filing, the Form 1120 isn't a real corporate tax return. It's a cover sheet. The actual purpose is to carry Form 5472 (the real reportable form) into the IRS's processing system, and Form 1120 is the standardized envelope the IRS uses for that delivery.

What the Pro Forma 1120 Actually Contains

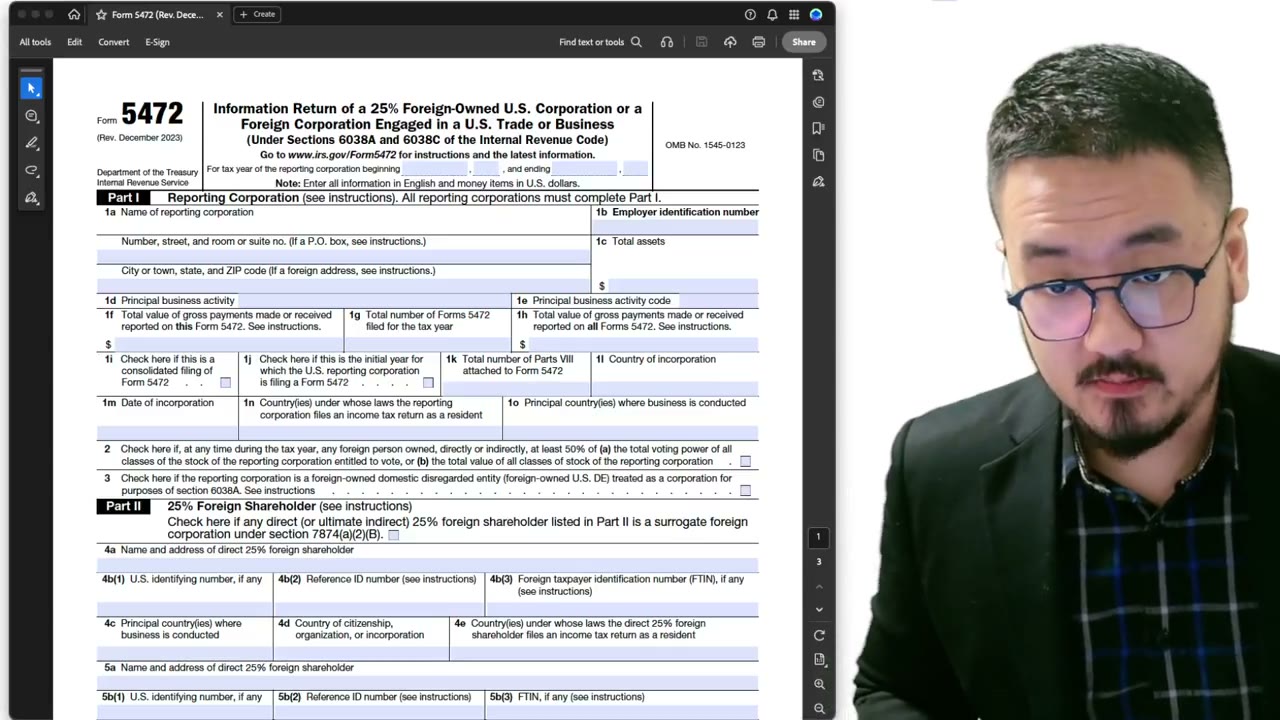

The fields the IRS asks you to fill on the pro forma Form 1120 are basic identity: entity name, EIN, address, and tax year. There's no income reported, no deductions claimed, no tax computed. The substantive income/deduction sections (Schedules C, J, K, L, M-1, M-2) are intentionally left blank — they don't apply to a disregarded entity.

This is why it's called a pro forma return. The form is filled in name only — it exists to identify the entity and signal "this is a foreign-owned U.S. disregarded entity" so the IRS routes the package to the right processing unit (the Ogden 5472 unit, not the standard 1120 unit).

The Real Purpose: Transparency, Not Taxation

The reason the IRS requires this filing isn't to collect tax. It's to maintain visibility into foreign-owned U.S. entities. Without Form 5472, foreigners could create U.S. LLCs and move money in and out invisibly — the U.S. tax authority would have no record of cross-border financial activity through these entities.

Form 5472 closes that gap by requiring annual reporting of any transaction between the U.S. entity and its foreign owner (or any other foreign related party). The IRS isn't taxing those transactions — they're tracking them, in case the cross-border flow needs scrutiny later (transfer pricing, money laundering, sanctions enforcement, etc.).

It's an Information Return, Not a Tax Return

The technical classification is information return. Like Form 1099 (which reports payments to contractors) or Form W-2 (which reports wages to employees), Form 5472 reports information to the IRS — it doesn't compute or collect tax.

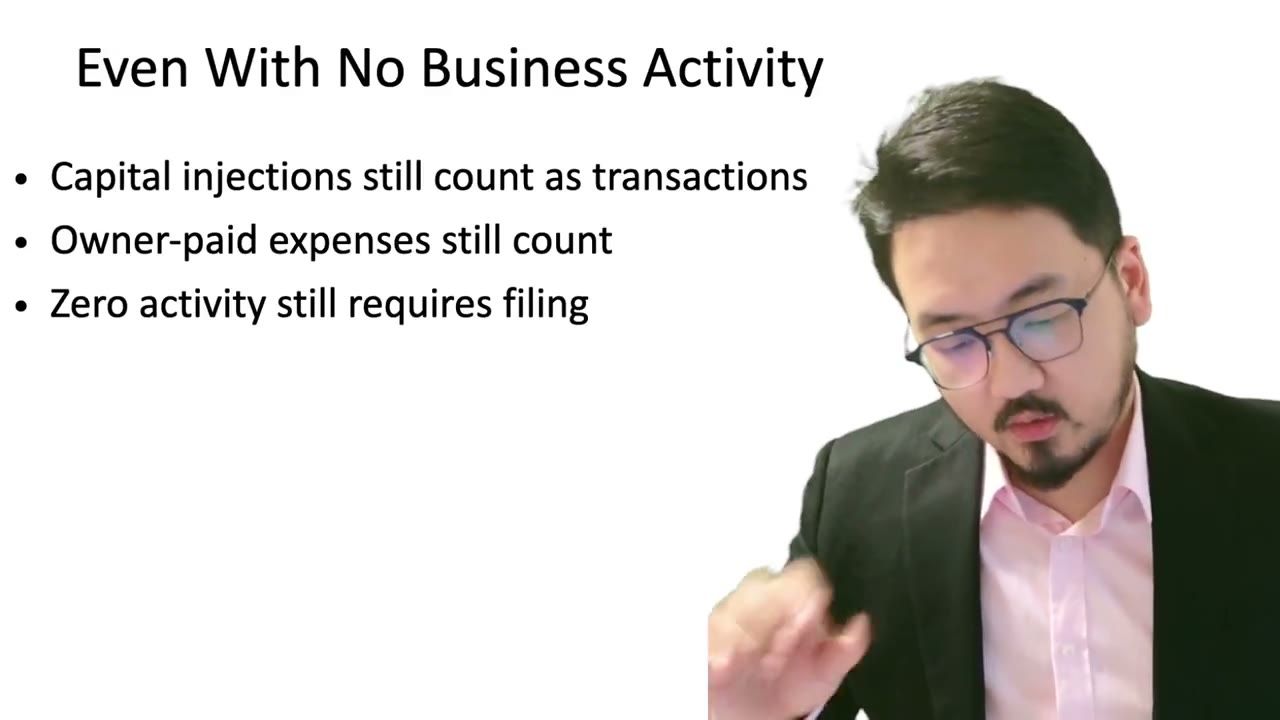

This matters because the penalties for information returns are different from tax returns. There's no "tax due" you can underpay. But the failure-to-file penalty for Form 5472 is steep — $25,000 per missed form, not because tax was lost, but because the information was withheld. That penalty exists to ensure the cross-border transparency the IRS needs.

Why Pro Forma 1120 Has to Be Attached

Why doesn't the IRS just accept Form 5472 by itself? Two reasons:

1. The IRS's processing infrastructure routes documents based on the cover form. A package without a 1120 cover would land in the wrong unit and get lost.

2. Form 5472 is technically defined as an attachment to a corporate tax return. The statute (IRC §6038A) treats the foreign-owned disregarded entity as a corporation for the limited purpose of reporting these transactions. The 1120 cover makes that statutory treatment work mechanically — the entity files "as if" it were a corporation, even though for tax purposes it isn't.

So the pro forma 1120 is the structural device that lets Form 5472 reach the IRS through the corporate-return pathway. Without it, the filing wouldn't fit the IRS's classification system.

What Foreign Owners Should Take Away

The pro forma 1120 + Form 5472 combination feels like overkill — two forms for what's essentially one report — but the structure is fixed and not negotiable. Treat the 1120 as a routing slip: fill in only the basic identity fields, leave everything substantive blank, and write "Foreign-owned U.S. DE" at the top of the form so the processing center routes it correctly.

The real attention goes into Form 5472 itself — that's where you report the reportable transactions, identify the foreign owner, and explain anything unusual. The 1120 is just paperwork around the 5472.

Frequently Asked Questions

If the 1120 is just a cover sheet, do I really need to file it?

Yes. The 5472 by itself doesn't fit the IRS's processing flow — without the 1120 cover, the package gets misrouted or rejected. The two forms together are the official, accepted filing format.

What if I skip the 1120 and only file the 5472?

The IRS will likely return the filing as incomplete, treating it as if you hadn't filed at all. That can trigger the $25,000 penalty for failure to file Form 5472. Always include both.

Do I owe any tax on the income reported on Form 5472?

Not directly — Form 5472 is informational only. Whether you owe U.S. tax depends on the underlying activity (e.g., effectively connected income, ECI). Form 5472 just documents what happened; the tax analysis is separate.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

1:30

1:30Why You Can't E-File Form 5472 + Pro Forma Form 1120 (IRS Reasons)

Form 5472 Explained — What It Is, Who Must File, and How It Works

Form 5472 Explained: What It Is, Who Must File, and How It Works (2025-2026)

1:55

1:55Pro Forma 1120 + Form 5472: Why Dormant LLCs Still Owe the $25,000 Filing

8:25

8:25Form 5472 Part I: Why the Reporting Corporation Files Income Tax as a U.S. Resident

1:04

1:04Why the IRS Requires Form 5472 for Foreign-Owned LLCs: Pro Forma 1120 Explained

2:00

2:00