Qualifying Surviving Spouse: Rent from Family Members Rules (Part 6)

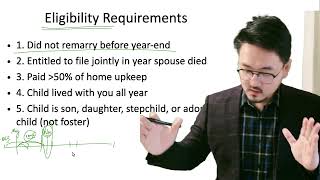

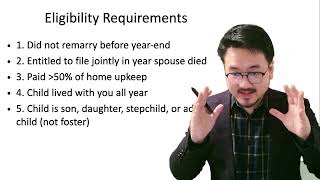

Key Takeaways

- Rent paid TO you counts as your income — you then pay bills from your funds

- Direct bill payments BY a relative count as the relative's household contribution

- The structure of family financial support affects QSS qualification

- Rent payments generally help maintain the surviving spouse's 50%+ threshold

- Direct bill payments by others can push you below the threshold

Rent from Family Members Living in Your Home

When a relative moves into the surviving spouse's home and pays rent, the tax treatment depends on how the payment is structured. If the relative pays rent directly to the surviving spouse, the IRS generally treats this as rental income to the surviving spouse — but the surviving spouse then uses those funds to pay household expenses, counting as the surviving spouse's own payment.

However, if the relative directly pays bills (mortgage, utilities) on behalf of the surviving spouse, those payments may be treated as the relative's contribution to household costs, potentially reducing the surviving spouse's share below 50%.

Structuring Family Support Correctly

The distinction between rent payments and direct bill payments matters significantly for the QSS household cost calculation. Rent paid to you is your income; you then pay the bills, and those bill payments count as yours. A relative paying your mortgage directly is the relative paying your household costs.

For example, if total household costs are $40,000 and a relative pays $800/month ($9,600/year) in rent to the surviving spouse, the surviving spouse still pays 100% of the household costs using their own funds (which include the rent received). But if the relative pays $9,600 directly toward the mortgage, the surviving spouse's share may be reduced.

Frequently Asked Questions

Do I need to report rent from a family member as income?

If you charge a relative fair market rent, you should report it as rental income on Schedule E. If you charge below-market rent to a family member, special rules may apply, and the IRS may not treat the arrangement as a rental activity.

What if the relative lives rent-free?

A relative living rent-free does not affect the household cost calculation unless they are directly paying household expenses. If they contribute nothing financially, the surviving spouse's share of household costs is unaffected.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Filing Status Guide

6:13

6:13Qualifying Surviving Spouse: Child's Survivor Benefits Rules (Part 5)

6:05

6:05Qualifying Surviving Spouse Eligibility: Did Not Remarry Requirement (Part 1)

5:33

5:33Qualifying Surviving Spouse: Entitled to File Requirement (Part 2)

12:42

12:42Qualifying Surviving Spouse: Paid More Than 50% Cost of Home (Part 3)

3:58

3:58Qualifying Surviving Spouse: Cost of Home Calculation Example (Part 4)

5:21

5:21