Qualifying Surviving Spouse Eligibility: Did Not Remarry Requirement (Part 1)

Key Takeaways

- Must not remarry before the end of the tax year to claim QSS

- QSS is available for two years following the year of spouse's death

- Remarrying ends QSS eligibility but opens MFJ with new spouse

- Must continue to meet all other QSS requirements each year

- This is a financial decision — weigh the tax implications carefully

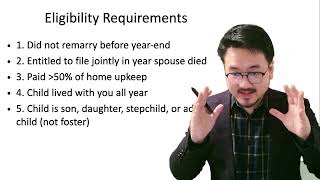

QSS Requirement: Did Not Remarry

The first eligibility requirement for Qualifying Surviving Spouse status is that you must not have remarried before the end of the tax year. If you remained single throughout the year while raising your dependent child, you can claim QSS for that year.

For example, if your spouse passed away in May 2023 and you stayed single through all of 2024, you can file as QSS for 2024. However, if you remarried in November 2024, you lose QSS eligibility for that year and would instead file jointly with your new spouse or choose another applicable status.

Financial Decision Making

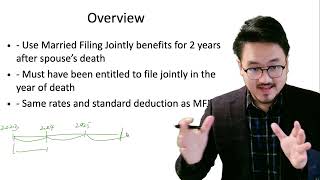

The decision to remarry has tax implications beyond the personal. Remarrying ends QSS eligibility but opens up MFJ filing with the new spouse. In many cases, this is still beneficial — but the two-year QSS window is specifically designed to ease the financial transition after a spouse's death, and the tax rates mirror the favorable MFJ brackets.

Frequently Asked Questions

What if I get engaged but don't marry during the tax year?

Engagement does not affect your filing status. Only a legal marriage ends QSS eligibility. If you are engaged but not married by December 31, you can still file as QSS if you meet all other requirements.

Can I claim QSS for three years?

No. QSS is available for only two tax years after the year your spouse died. In the year of death itself, you can file a joint return with your deceased spouse.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Filing Status Guide

5:33

5:33Qualifying Surviving Spouse: Entitled to File Requirement (Part 2)

12:42

12:42Qualifying Surviving Spouse: Paid More Than 50% Cost of Home (Part 3)

3:58

3:58Qualifying Surviving Spouse: Cost of Home Calculation Example (Part 4)

6:13

6:13Qualifying Surviving Spouse: Child's Survivor Benefits Rules (Part 5)

13:17

13:17Qualifying Surviving Spouse: Rent from Family Members Rules (Part 6)

5:21

5:21