C/O (Care Of) Address on Form 1120 — The IRS-Approved Workaround

Key Takeaways

- C/O is the IRS-approved way to route mail through a third party while satisfying the Form 1120 address rule

- Format: 'C/O [Third Party Name], [Their Street]' on the street address line

- Acceptable recipients: CPA, attorney, bookkeeping firm, U.S. mailbox service (with a real street address)

- The C/O recipient does NOT need to be a registered agent — that's actually disqualifying

- Use the same C/O notation on both Form 1120 and Form 5472 Part I, Line 1a

What 'C/O' Means on an IRS Form

"C/O" stands for "Care Of" — a centuries-old postal convention meaning "please give this to [the named third party] on behalf of [the addressee]." On Form 1120 and Form 5472, C/O is the IRS-approved way to route your tax mail through a third party while keeping your principal place of business as the actual address.

The Form 1120 instructions explicitly authorize this format: "If the corporation receives mail in care of a third party (such as an accountant or attorney), enter on the street address line 'C/O' followed by the third party's name and street address or P.O. box."

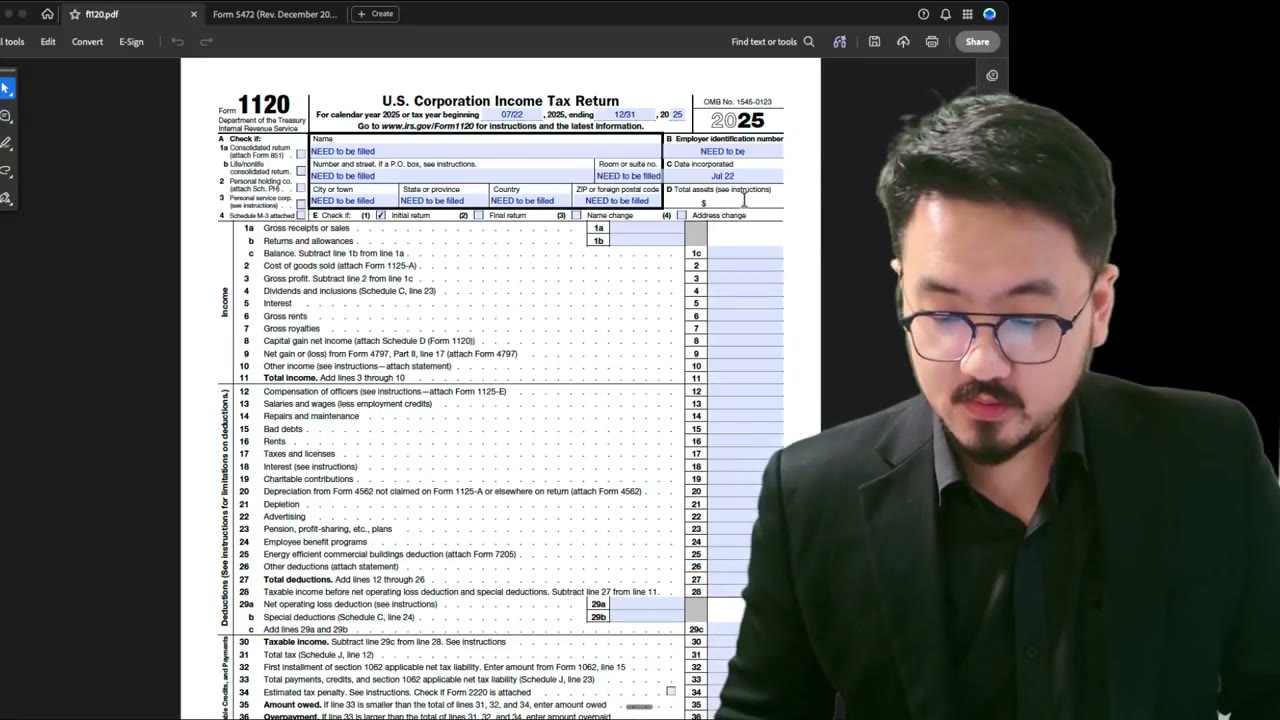

Exact Formatting on Form 1120 and Form 5472

On the principal address line of Form 1120 (and Form 5472 Part I, Line 1a), format like this:

Street Address: C/O [Third Party Name], [Their Street] City / State / ZIP: [Their location]

Example:

Street Address: C/O Smith CPA LLP, 1234 Main St City / State / ZIP: Wilmington, DE 19801

The LLC's actual operations might be in Berlin or Mumbai — but the IRS treats the C/O address as the official correspondence destination. The principal place of business remains conceptually wherever you actually operate; the C/O notation just routes mail.

Who Can Act as the C/O Recipient

The IRS instructions give two examples — "accountant or attorney" — but the actual scope is broader. Any third party who agrees to receive your mail and has a stable U.S. street address can serve as the C/O recipient.

Valid C/O recipients (in order of how clean they look on an IRS form):

1. Your CPA or enrolled agent — most defensible 2. Your attorney — equally defensible 3. A bookkeeping or tax-prep firm with a real office 4. A U.S. mailbox service with a street address (NOT a P.O. Box) — works but looks less professional 5. A U.S. friend or family member willing to forward mail — works in a pinch but raises questions in audit

Who can't act as C/O recipient: - The registered agent for your state of incorporation (the rule specifically excludes this) - A P.O. Box without a street address backing - A fictitious address or commercial mail-drop with no real presence

Why This Beats Using the Registered Agent Address

Three reasons to use C/O over the bare registered agent address:

1. Full IRS compliance. The Form 1120 instructions explicitly permit C/O; they explicitly prohibit the registered agent address. There's no ambiguity.

2. Better audit profile. If an IRS examiner pulls your file and sees a C/O notation, the optics are "taxpayer uses a professional service provider for mail handling" — a normal pattern. A bare registered agent address on the same line signals "this filer didn't read the instructions or is hoping no one notices."

3. Easier to explain on §6038A or transfer-pricing reviews. The C/O notation cleanly separates the operational address (where the business actually happens) from the correspondence address (where mail goes). The registered agent address conflates the two, making the entire address question harder to defend.

Frequently Asked Questions

Do I need a written agreement with the C/O recipient?

Not for IRS purposes. The IRS doesn't ask for or audit your agreement with the C/O recipient. But you should have a practical understanding with them — they need to forward, scan, or hold mail for you. Many CPA firms offer mail-forwarding as part of their standard service.

Can I use a service like iPostal1 or Earth Class Mail as the C/O recipient?

Technically yes — they have real U.S. street addresses. But these services aren't widely known to the IRS, and an examiner unfamiliar with them might question the legitimacy. For higher-stakes filings, prefer a CPA or attorney whose firm name is recognizable.

Does the C/O format work for state filings too?

Usually yes, but check your state. Most states accept C/O addresses for their annual report filings. Some require the registered agent address to also be listed — in which case both addresses go in different fields on the state form. The federal Form 1120 / 5472 has only one address field, so the C/O goes there.

Can I change the C/O recipient mid-year?

Yes. If you switch CPAs or change service providers, simply use the new C/O on the next year's filing. The IRS doesn't track address changes between years for foreign-owned DEs — they just use whatever's on the most recent return.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

1:30

1:30Why Foreign LLC Owners Use Registered Agent Address (Risk Tradeoffs)

2:25

2:25Can You Use a P.O. Box on Form 1120? IRS Address Rules for LLCs

2:00

2:00Can You Use Your Registered Agent's Address on Form 1120? IRS Rules

2:00

2:00Foreign LLC No U.S. Office: Foreign Address vs Service Address (Part 2)

3:35

3:35Form 1120 Item D: Total Assets and Why You Must Fill It Despite Pro Forma Status

Form 1120 Personal Service Corporation Tax Year Guide