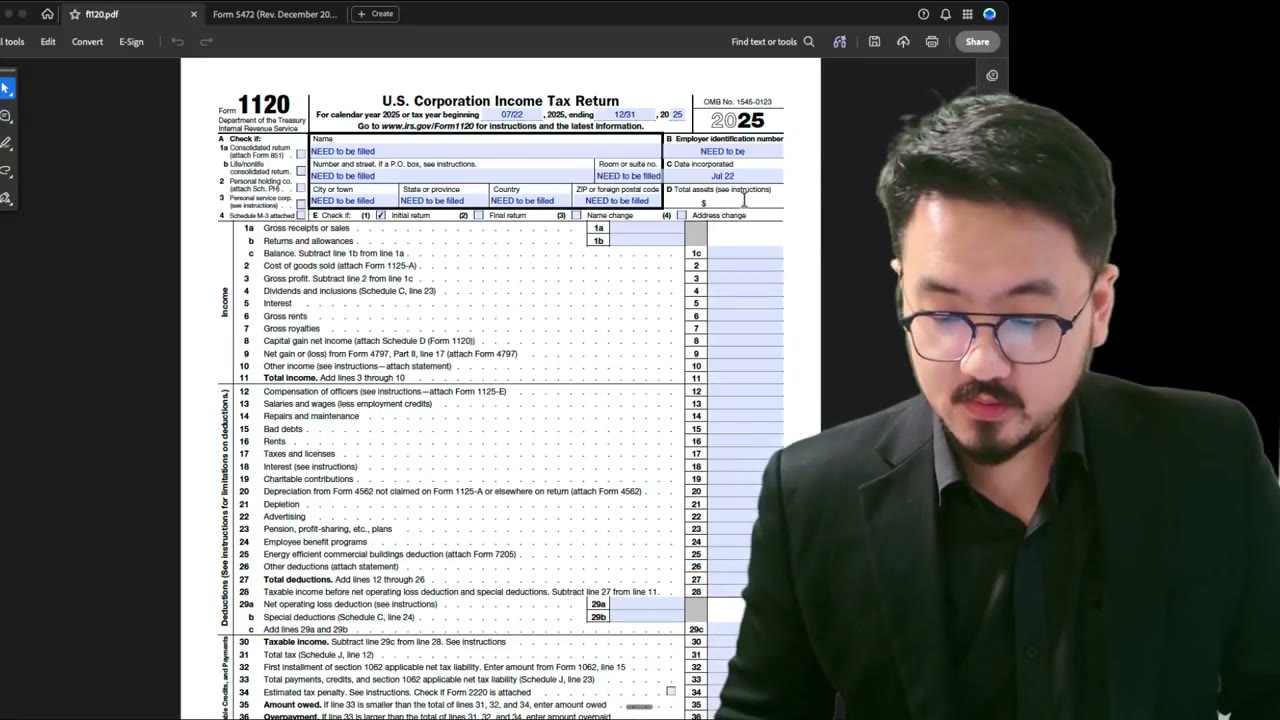

Why Foreign LLC Owners Use Registered Agent Address (Risk Tradeoffs)

Key Takeaways

- Using the registered agent address as the principal address is a common practice despite being non-compliant

- The IRS rarely catches it automatically — typically only on examination or §6038A review

- Risk depends on transaction volume, operational profile, and any treaty positions you're claiming

- The C/O workaround gives you reliable mail handling with full IRS compliance

- Service providers for C/O don't need to be registered agents — accountants, mailbox services, or friends all qualify

The Reality vs. the Rule

If you ask a dozen foreign-owned LLC owners how they fill out Form 1120, you'll find a sizable share using their registered agent's address — despite the explicit IRS prohibition. The reason is practical, not legal: registered agents are set up to receive U.S. mail, the IRS sends notices by U.S. mail, and the address solves a problem the IRS rule doesn't acknowledge.

Most service providers (Northwest, Incfile, ZenBusiness, the formation agent inside Stripe Atlas or doola) offer mail-forwarding as part of their service. Some forward by scan-and-email; others physically forward. Either way, a notice that arrives at the registered agent's address actually reaches the foreign owner — which is more than you can say for a notice mailed to an unreliable foreign address.

What Actually Triggers an IRS Letter About the Address

In practice, the IRS doesn't have an automated check that compares the principal address against the registered agent address on file with the state. The form goes through scanning and data entry; the address is recorded as-is. Years can pass without anyone at the IRS noticing.

The address issue typically surfaces only when something else triggers an examination: a §6038A review of related-party transactions, a refund claim that requires verification, a transfer-pricing inquiry, or a multi-year audit. At that point, the examiner pulls the registered agent records from the state and compares — and a mismatch becomes part of the deficiency analysis.

When to Risk It and When Not To

Risk tolerance for the registered agent shortcut depends on your transaction volume and audit profile:

Low risk: Single-member LLC with minimal transactions (mostly capital contributions and distributions to/from the foreign owner). The §6038A penalty exposure is per form per year — annoying but not company-killing if your fact pattern supports reasonable-cause relief.

Medium risk: LLC with significant operational activity, employees, or substantial inventory. Examination is more likely, and the registered agent address can compound into a broader "the LLC has no real U.S. presence" finding.

High risk: LLC engaged in U.S. trade or business with a treaty position (e.g., claiming protection from U.S. taxation under a tax treaty). Here the address is part of the treaty fact pattern, and using a non-operating address can undermine your treaty claim entirely.

A Safer Compromise: The C/O Workaround

The middle path — and the one we recommend — is the IRS-approved Care Of (C/O) address. Form 1120 instructions explicitly permit using "C/O [Third Party Name], [Third Party Address]" on the street address line.

This gives you:

- Reliable mail handling (you list a service provider's address) - IRS compliance (the C/O notation is explicitly allowed) - A clean audit trail (the principal place of business is still implicitly your operational address, just routed through a third party)

Most foreign owners who want both compliance and reliable mail handling use this. The provider can be an accountant, attorney, U.S.-based mailbox service, or even a friend — anyone who agrees to receive your mail. The provider does NOT have to be a registered agent.

Frequently Asked Questions

Will the IRS catch me if I use the registered agent address?

Probably not on the initial filing. The IRS scans Form 5472 and Form 1120 data into its systems without automatically cross-checking against state registered-agent records. The issue surfaces only when something else triggers an examination — and even then, examiners often focus on transaction substance rather than address technicalities. Risk is non-zero but low for routine filers.

If many people do it, why is it still wrong?

The IRS instructions are clear. Common practice doesn't change the rule. The reason 'many people do it' persists is that enforcement has been historically lax — but the rule remains, and the IRS could enforce it more strictly at any time. The C/O workaround gives the same practical outcome with full compliance.

What if my registered agent IS my accountant?

Then you should still use the C/O format. List 'C/O [Their Firm Name], [Their Street Address]' on the address line. The C/O prefix is what makes it compliant; without it, the IRS instructions still treat the address as a 'registered agent' address (even if the agent happens to be your accountant).

Does this rule apply to faxed returns or only mailed returns?

It applies to both. The address rule is about what's printed on the form itself, not about how the form is delivered. A faxed return with the registered agent address on Form 5472 Part I, Line 1a has the same compliance issue as a mailed one.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:00

2:00Can You Use Your Registered Agent's Address on Form 1120? IRS Rules

1:45

1:45C/O (Care Of) Address on Form 1120 — The IRS-Approved Workaround

3:35

3:35Form 1120 Item D: Total Assets and Why You Must Fill It Despite Pro Forma Status

1:23

1:23Can the IRS Reissue a CP 575 Letter? What to Do If You Lost It

2:25

2:25Can You Use a P.O. Box on Form 1120? IRS Address Rules for LLCs

2:15

2:15