Foreign-Owned LLC IRS Mail Checklist: 5 Steps Before You Send Form 5472

Form 5472 reporting flow

How a foreign-owned single-member LLC reports its reportable transactions to the IRS.

Identify reportable transactions

Money in/out between the LLC and its foreign owner or related parties.

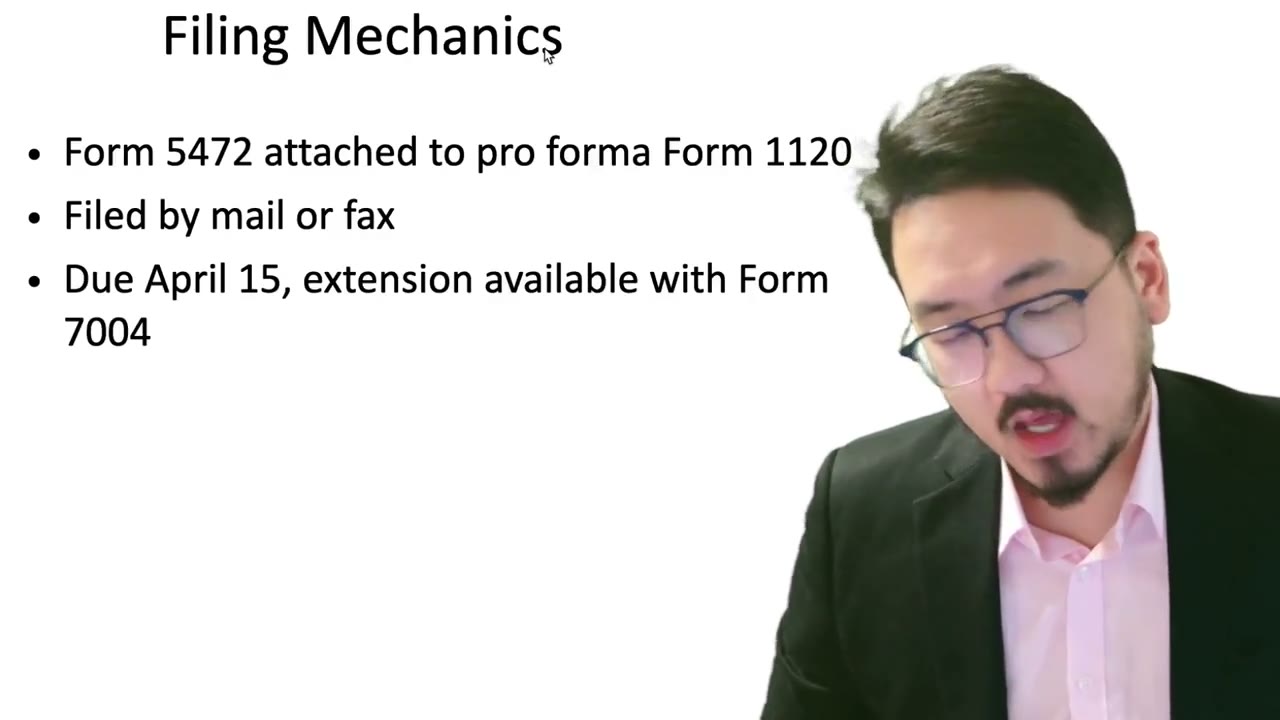

Prepare pro forma 1120 + 5472

Form 5472 attaches to a pro forma Form 1120 cover page.

File by the deadline

Mail or fax the package by the corporate return due date.

Keep records

Retain transaction records supporting every reported amount.

Key Takeaways

- Write "Foreign-owned U.S. DE" across the top of Form 1120 — required for IRS PIN Unit routing

- Use the dedicated Ogden PIN Unit address with M/S 6112 and 'Attn: PIN Unit' — NOT the standard Form 1120 address

- Sign with wet ink (pen on paper) for mailed returns — electronic signatures only work for fax under IRC §6061

- Ship via an IRS-approved Private Delivery Service tier per Notice 2016-30 — Ground services do NOT qualify for §7502

- Save shipping label, acceptance receipt, tracking number, and signed delivery confirmation as §7502 proof for 6+ years

- Pro forma Form 1120 has no tax due — never include a payment with the envelope

- If you missed the deadline, CCA 202617012 (April 2026) provides reasonable-cause relief for small foreign-owned LLCs

Why Mailing Form 5472 Is Different From Mailing Any Other Tax Form

A foreign-owned single-member LLC's annual U.S. filing is a single information return — Form 5472 — attached behind a pro forma (placeholder) Form 1120 that exists only as a cover sheet. The IRS treats this exact combination as a special-case workflow with its own mailing address, its own internal routing code, its own signature rules, and its own dedicated processing team inside the Ogden Submission Processing Center.

If you mail it the way you'd mail an ordinary corporate Form 1120, almost everything goes wrong silently. The package ends up in the wrong scanning queue. A clerk sees an income tax return with all the income lines blank and flags it for examination. Three weeks later you get a CP-notice asking for the missing income figures, the missing Schedule L, the missing Schedule M-1 — none of which apply to your filing — and your timely-filed claim under IRC §7502 starts looking shaky.

This checklist covers the five things every foreign-owned LLC owner must do correctly before sealing the envelope. Each step has a video walkthrough embedded below. They're ordered from "absolutely required to avoid CP-notices" to "required to defend your filing date if the IRS challenges it."

None of these steps individually triggers the $25,000 §6038A penalty. But each missing piece compounds. A filing that lacks the header marking AND uses the wrong address AND lacks a wet-ink signature AND ships via an unapproved courier is, functionally, an unfiled return — and an unfiled Form 5472 is exactly what the $25,000 penalty was designed to punish.

Step 1: Write "Foreign-Owned U.S. DE" Across the Top of Form 1120

Open the current IRS instructions for Form 5472 and you will find a small but easy-to-miss requirement, in the section titled "Filing requirements for foreign-owned U.S. disregarded entities." The IRS tells filers to write the phrase "Foreign-owned U.S. DE" (DE = disregarded entity) across the top of the pro forma Form 1120 — by hand or typed — before mailing or faxing.

This marking is the routing signal. Without it, the Form 1120 on top of your package looks like any other corporate return — and gets queued for the regular 1120 processing pipeline, which expects income, deductions, balance-sheet entries, and tax due. When the IRS pipeline encounters a 1120 with all those lines empty, the return gets flagged for examination or correspondence. You'll receive a CP-notice asking for missing data that, for a disregarded entity, doesn't exist.

Mechanically: write or type "Foreign-owned U.S. DE" in the white margin above the form's pre-printed header (above the OMB number and the tax-year box). Center it. Use capital letters. Use solid black or dark blue ink, or a black font if you're typing — light pencil or grey will not survive fax compression or document scanning. The phrase should be unmistakable on a one-second glance.

The marking goes only on the pro forma Form 1120 — the cover sheet. Form 5472 itself does not need this header because its own Part I, Line 1 fields explicitly identify the filing as a foreign-owned disregarded entity return.

If you forgot this on a return you've already mailed: don't panic. Wait for the CP-notice (typically arrives 4-12 weeks after the IRS receives the package). Respond promptly with a corrected cover page showing the header. Your original §7502 timely-filing date still controls — only processing is delayed.

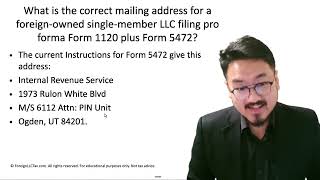

Step 2: Use the Dedicated Ogden PIN Unit Address (Not the Standard Form 1120 Address)

The address you find in the standard Form 1120 instructions is NOT the address for a foreign-owned DE filing. Standard Form 1120 returns route to one of several IRS service centers based on entity size and state. Foreign-owned DE filings route to a dedicated team called the PIN Unit at the Ogden Submission Processing Center.

The correct address:

Internal Revenue Service 1973 Rulon White Blvd, M/S 6112 Attn: PIN Unit Ogden, UT 84201 United States

Three things have to appear on the envelope or shipping label, exactly as shown:

1. "M/S 6112" — this is the IRS internal mail stop code. It tells the Ogden mailroom which floor and which team to route the envelope to. Some couriers' auto-formatting will try to expand it to "Mail Stop 6112" — keep the abbreviated form, which is what the IRS scanners are calibrated to read.

2. "Attn: PIN Unit" — the human-readable team name. PIN stands for Production Implementation Network, the internal IRS function that processes information returns from foreign-owned DEs. Without this attention line, your envelope sits in the Ogden general queue for days before being manually re-routed.

3. The full city/state/ZIP: Ogden, UT 84201. Don't drop digits. Don't add a ZIP+4 unless your courier requires one — and if they do, use 84201-0023 (the IRS's general Ogden routing code) or leave it at 84201.

When booking a courier (DHL Express, FedEx, UPS), enter "Internal Revenue Service" as the receiver Company Name. Leave the Contact Name field blank if optional, or enter "PIN Unit" if required. Use 1-800-829-4933 (the IRS Business and Specialty Tax Line) for any required receiver phone field — couriers need a phone for international customs forms, and that number is officially associated with the agency even though no one answers it for delivery inquiries.

If you've already mailed to the wrong address, the IRS will eventually forward your package — but this can add 4-8 weeks to processing and may push you past your filing deadline if you were cutting it close.

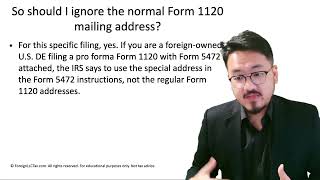

Step 2b: Why the Standard Form 1120 Address Is Wrong (Even Though the Instructions Mention It)

First-time filers often spot the Form 1120 instructions, find the table of mailing addresses keyed by entity location, pick the address that matches their state, and ship there. This is wrong for foreign-owned DE filings — and the reason isn't obvious.

The standard Form 1120 instructions assume you're filing a real corporate income tax return. Those instructions list addresses for the Cincinnati, Kansas City, Memphis, and Austin service centers. None of those centers has a team set up to process Form 5472 attached to a pro forma Form 1120 for a foreign-owned disregarded entity. They process actual corporate income tax returns.

The Ogden Submission Processing Center, by contrast, is where the IRS centralizes international information returns — Form 5472, Form 5471, Form 8938, Form 1042, the §965 transition tax forms, FBAR coordination with FinCEN. The PIN Unit inside Ogden is the team that handles your specific combination. If your envelope arrives anywhere else, it eventually gets forwarded to Ogden — but the delay can be weeks.

The Form 5472 instructions (not the Form 1120 instructions) contain the correct address. Always follow the Form 5472 instructions for this filing, not the Form 1120 instructions. The pro forma 1120 is just a cover sheet; the substantive return is the Form 5472, and the Form 5472 instructions are the authoritative source for where to send the package.

Step 3: Sign Form 1120 With a Wet Ink Signature

If you mail the return, the IRS requires a "wet ink" signature on the actual paper inside the envelope. That phrase has a specific meaning in IRS practice — it means a signature made by physically applying a pen to the paper that arrives at Ogden. It does NOT mean a typed name in a script font, a scanned image of your signature inserted into the PDF, a DocuSign or Adobe Sign electronic signature, or a stylus signature embedded in a PDF that you then print and mail.

The statutory basis is IRC §6061, which requires returns to be signed under penalty of perjury. The IRS treats an original wet-ink signature as the canonical evidence of perjury exposure — meaning the signer affirms the return is true under threat of criminal prosecution. A scanned or pasted signature image fails this evidentiary standard for mailed returns. (Faxed returns are different — see below.)

Mechanically:

1. Print Form 1120 (the pro forma cover sheet) on standard 8.5x11 paper. 2. Locate the "Sign Here" block on page 1 — bottom of the form. 3. Sign with a pen in dark blue or black ink. Avoid pencil (erasable), red ink (visually conflicts with IRS form markings), or light gel pens that may not scan cleanly. 4. Fill in the "Print Name" line — your typed-or-handwritten full legal name. 5. Fill in the "Title" line — "OWNER" for a single-member LLC owner. (For a multi-owner LLC, use the title you've actually been given, e.g., "MANAGING MEMBER.") 6. Fill in the date — the date you signed, in MM/DD/YYYY format.

If you can't easily access a printer (a common problem for foreign owners), switch to fax submission instead. The IRS accepts electronic signatures embedded in the PDF for fax — because the fax transmission itself is treated as the electronic delivery, and the on-screen signature you draw in the PDF is sufficient under IRS Internal Revenue Manual procedure for the fax channel. This is the single biggest reason most foreign owners file by fax rather than mail.

If an authorized representative is signing on your behalf (a CPA, enrolled agent, or attorney), they must have a current Form 2848 (Power of Attorney) on file with the IRS. A generic power of attorney from your home country, or even a U.S. general POA, is NOT sufficient — Form 2848 is the only POA the IRS accepts for signing tax returns on someone else's behalf.

Step 4: Ship via an IRS-Approved Private Delivery Service

USPS Certified Mail or Registered Mail is the gold standard for U.S.-based filers. The postmark date locks in your filing date under IRC §7502, the "timely mailing is timely filing" rule, regardless of when the IRS actually opens the envelope.

Foreign owners almost always can't use USPS directly. USPS does not pick up internationally — you can't drop a package in a USPS box from your country and have it arrive at Ogden. Some workarounds (mailing it to a U.S. friend who then drops it at USPS) exist, but they introduce a hold time that erodes your §7502 protection.

The IRS solves this with §7502(f), which authorizes Treasury to designate "Private Delivery Services" whose acceptance date is treated the same as a USPS postmark. The current designated list, published in IRS Notice 2016-30, includes three carriers:

DHL Express — but only these specific tiers qualify: Express 9:00, Express 10:30, Express 12:00, Express Worldwide, Express Envelope, Import Express 10:30, and Import Express Worldwide.

FedEx — First Overnight, Priority Overnight, Standard Overnight, 2 Day, International Next Flight Out, International Priority, International First, and International Economy.

UPS — Next Day Air Early AM, Next Day Air, Next Day Air Saver, 2nd Day Air, 2nd Day Air A.M., Worldwide Express Plus, and Worldwide Express.

This is the part that catches the most filers: not every service from these three brands qualifies. FedEx Ground is NOT on the list. UPS Ground is NOT on the list. DHL Express Economy is NOT on the list. If you book one of these unapproved tiers, your filing isn't "late" in a courier sense — it'll still arrive at Ogden — but it loses §7502 timely-mailing protection. The IRS will use the date they actually receive your package as your filing date, not the date the courier accepted it.

For most foreign owners shipping a small documents envelope to Ogden, the most affordable approved tier is DHL Express Worldwide or FedEx International Economy/Priority — typically $50-100 from Europe or Asia, $80-200 from Latin America or Africa.

Step 4b: Use USPS Domestically Only (and What to Do If You're Outside the U.S.)

Even though USPS isn't an option from abroad, it's worth understanding the inside-the-U.S. choice — because if you have a U.S. friend, a U.S. business partner, or a U.S. mail-forwarding service that can ship for you, USPS Certified Mail or Registered Mail is generally cheaper than the equivalent PDS tier.

USPS Certified Mail: $4-5 with delivery confirmation. The mailing receipt shows the postmark date, which locks in your §7502 filing date. Tracking is online but minimal — you see when it's accepted and delivered, no scans in between.

USPS Registered Mail: $14-20 with stricter chain-of-custody handling. Every USPS employee who handles the package signs for it internally. This is overkill for most filings, but worth it if you're sending a return so close to deadline that even a 24-hour delay matters, or if you're filing high-stakes amended returns where defensive recordkeeping matters.

For foreign owners using a U.S. intermediary, be careful about timing. The IRS treats the date the intermediary's USPS receipt is dated as your §7502 date — not the date you handed the package to your friend. If your intermediary holds the package for a week before mailing, you've burned a week of your timely-filing buffer. If you must use an intermediary, ship the package to them by an IRS-approved PDS tier (so the intermediary handoff is itself a covered event) and instruct them to USPS-mail it the same day they receive it, with you as the sender of record on the USPS receipt.

Step 5: What Goes in the Envelope (The Pre-Mail Checklist)

Before you seal the envelope, run through this checklist. Missing any one item is a common cause of CP-notices or processing delays:

1. Form 1120 (pro forma) — page 1 only is required, with "Foreign-owned U.S. DE" written across the top, the entity name, EIN, address, and signature block filled in. Pages 2-6 can be omitted or included blank.

2. Form 5472 — all required parts complete. For foreign-owned single-member LLCs that's typically Part I (Reporting Corporation), Part II (25% Foreign Shareholder), Part III (Related Party), and Part IV/V/VI as applicable based on your transactions.

3. Supporting statements — if you have transactions that don't fit cleanly into Part IV's pre-printed categories, attach Part V or a federal supporting statement explaining each one. The IRS prefers explicit disclosure over forced fitting into wrong categories.

4. A copy of your prior-year Form 5472 — optional but helpful if this isn't your first year. The Ogden PIN Unit examiners use it to verify continuity of reporting.

5. Form 2848 (if signed by a representative) — must be on file with the IRS already, but including a copy in the envelope speeds processing.

Don't include:

- A check or money order. Pro forma Form 1120 shows zero tax due, so there's no payment. - Your formation documents (Articles of Organization). The IRS doesn't ask for these and including them muddies the package. - A cover letter unless you have a specific reason (e.g., reasonable-cause statement for a late-filed return).

Fold the package once horizontally if it fits a #10 business envelope, or send unfolded in a 9x12 documents envelope. The 9x12 is preferable — pro forma 1120 + Form 5472 + statements is typically 5-15 pages, and folded paper can jam IRS document scanners.

Step 6: Save Four Pieces of Proof (For §7502 and Future Audits)

Once shipped, save four items in your tax records:

1. The shipping label or booking confirmation — must show the specific PDS service tier name (e.g., "DHL Express Worldwide" or "FedEx International Priority"). Generic confirmations that don't show the tier are insufficient if the IRS challenges your filing date.

2. The acceptance receipt — the timestamped slip showing the date and time the courier physically accepted your package. For DHL Express, this is the screen you see right after the courier scans your shipping label; save the email or PDF.

3. The tracking number — letterhead and tracking pages are sufficient. Save a screenshot showing the delivery scan to the IRS Ogden address.

4. The delivery confirmation — most couriers offer a signature-on-delivery upgrade for $5-10. For an IRS filing, it's worth it. The signature proves the IRS received the package (rather than it being left on a loading dock or marked as "delivered" to the wrong building).

Under §7502, the date the approved PDS accepts your package is your statutory filing date — not the date the IRS opens the envelope or processes the return. These four documents are the evidence supporting that filing date. If the IRS ever sends you a notice claiming your return was filed late, this is what you'll attach to your protest.

Keep the proof for at least 6 years from the filing date. IRC §6501(e) gives the IRS a 6-year statute of limitations for assessments where the taxpayer omitted substantial gross income. For Form 5472 specifically, which is an information return rather than an income tax return, the statute mechanics differ — but practitioners generally recommend 6-7 years of retention to be safe.

If you store records digitally, scan each piece to PDF, name the file with the filing tax year, and keep them in the same folder as your tax return copies. Cloud backup is fine; the IRS accepts digital copies for §7502 evidence.

Bonus: The Full DHL Express Booking Walkthrough (Members-Only)

If you're new to international shipping, DHL Express's online booking form is the part of the mailing process that surprises most foreign owners. The form has 11 distinct screens covering country of origin, receiver info, sender info, shipment type, package dimensions, payment, service tier selection, optional signature service, courier pickup vs drop-off, and the final label printing.

A few specific traps:

— On the receiver-info screen, DHL's auto-format sometimes expands "M/S 6112" to "Mail Stop 6112" — which causes routing problems at Ogden's mailroom. Always verify the second address line shows "M/S 6112" before confirming.

— On the shipment-type screen, picking "Package" instead of "Documents" triggers customs declarations that don't apply to a tax filing, adds $20-40 to the price, and can cause customs delays.

— On the service-tier screen, the cheapest visible option is usually DHL Express Economy or DHL eCommerce — neither of which qualifies for §7502 protection. The right pick is DHL Express Worldwide or Express Envelope.

— On the optional-services screen, signature-on-delivery is the one paid extra worth taking. The other upsells (insurance, indemnity) are not needed for an IRS filing.

We maintain a 13-video click-by-click walkthrough of the DHL Express booking flow, included with the Form 5472 video pack or membership at /unlock-videos. The first video — the country-availability check — is free. The remaining screens cover the booking form with the exact entries for an IRS Ogden shipment.

The full Mail-to-IRS guide combining all 24 walkthrough videos lives at /guides/mail-form-5472-to-irs.

What If You Missed the Deadline Entirely?

If you missed your Form 5472 deadline (typically April 15 for calendar-year filers, or June 15 if you qualify for the automatic foreign-owner extension, or October 15 with a Form 7004 extension), the right move is to file as soon as possible with a reasonable-cause statement attached.

The §6038A penalty for late or missing Form 5472 is up to $25,000 per form per year. That's the headline number — but it isn't automatic. The IRS must propose the penalty in a notice, and you can challenge it by showing reasonable cause under the standard set out in Treasury Regulation §1.6038A-4.

Reasonable cause is fact-specific. The IRS looks at whether you exercised ordinary business care and prudence — for foreign owners, that includes whether you knew about the requirement, whether you had advisors competent in U.S. cross-border tax, whether the LLC actually had transactions (the rule applies even with zero transactions, but the penalty calculus differs), and whether you came forward voluntarily or were caught.

In April 2026, the IRS Office of Chief Counsel issued CCA 202617012, which gives examiners more liberal reasonable-cause discretion for small foreign-owned corporations. If your LLC qualifies (broadly: not a Fortune 1000 subsidiary, no prior penalty history, transactions of modest scale), the CCA provides a path to penalty abatement that wasn't formally available before.

If you're in this situation, see our full guide at /guides/form-5472-common-mistakes for a worked example of a reasonable-cause statement and the documentation that supports it.

Frequently Asked Questions

What happens if I forget one of these five steps?

Each missed step has its own consequence: a missing header causes IRS routing delays and CP-notices; the wrong address causes the package to be internally forwarded (4-8 weeks lost); a missing wet ink signature can invalidate the filing under §6061; an unapproved courier loses §7502 timely-filing protection; missing proof leaves you defenseless if the filing date is challenged. None individually triggers the $25,000 §6038A penalty automatically, but each can compound into a much larger problem and a longer IRS exam.

Is faxing easier than mailing for foreign owners?

Yes, usually. Fax accepts electronic signatures (no wet ink requirement), doesn't require a courier or international shipping, provides instant transmission proof via the confirmation sheet, and reaches the same Ogden PIN Unit team. The main downside is the IRS fax line can be busy near deadlines. See our /guides/how-to-submit-form-5472 guide for the current fax number and fax-service recommendations.

Can I use Stripe Atlas's mail-handling service to ship for me?

Be careful. The IRS treats the §7502 acceptance date as the date the COURIER accepts the package — not the date you handed it to a third party. If a mail-handling service holds your envelope before shipping (even by 1-2 days), that hold time counts against your filing date. If you use a mail-handling intermediary, verify they ship same-day via an IRS-approved PDS tier, with you as the sender of record on the courier's receipt.

What if I missed the deadline entirely?

File as soon as possible with a reasonable cause statement attached. The §6038A penalty is up to $25,000 per form per year, but the IRS may abate it if you can show reasonable cause under Treas. Reg. §1.6038A-4. CCA 202617012 (April 2026) gives small foreign-owned corporations more liberal abatement consideration. See our /guides/form-5472-common-mistakes article for a worked reasonable-cause statement example.

How long should I keep these mailing records?

The IRS has a 6-year assessment statute under §6501(e) for substantial omissions and an indefinite statute for unfiled returns. Keep the mailing proof at least 6 years from the date the return was filed. For Form 5472 specifically, many advisors recommend keeping it 7+ years given the stakes — both for §7502 defense and for general substantiation if the IRS examines a related year.

What about the OBBBA 2026 1% remittance tax — does it affect my mailing?

No. The enacted 1% tax concerns certain cash-funded consumer remittance transfers after December 31, 2025; it does not change Form 5472 filing requirements or the mailing process. The same Ogden PIN Unit address, signature rules, and §7502 private-delivery-service list apply. See /guides/remittance-excise-tax for the transfer scope.

Can I email or upload my Form 5472 to the IRS?

No. The IRS does not accept email, secure-portal upload, or any other electronic submission for Form 5472 + pro forma 1120. The only two valid submission methods are fax and mail. (E-filing through Modernized e-File doesn't accept this combination — see /learn/why-you-can-t-e-file-form-5472-pro-forma-form-1120-irs-limitations-explained for the technical reason.)

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

2:00

2:00IRS Ogden PIN Unit Mailing Address for Form 5472 + Pro Forma 1120

1:30

1:30Why Foreign-Owned LLCs Ignore the Standard Form 1120 Mailing Address

2:00

2:00Wet Ink Signature Required for Mailed IRS Returns (Form 1120 + 5472)

5:30

5:30Pro Forma 1120 + Form 5472: Mail vs Fax (and Why the Mailing Address Is Special)

3:25

3:25Pro Forma 1120: Wet Signature, Owner Title, and Why Schedules C/J/K/L Stay Blank

1:30

1:30