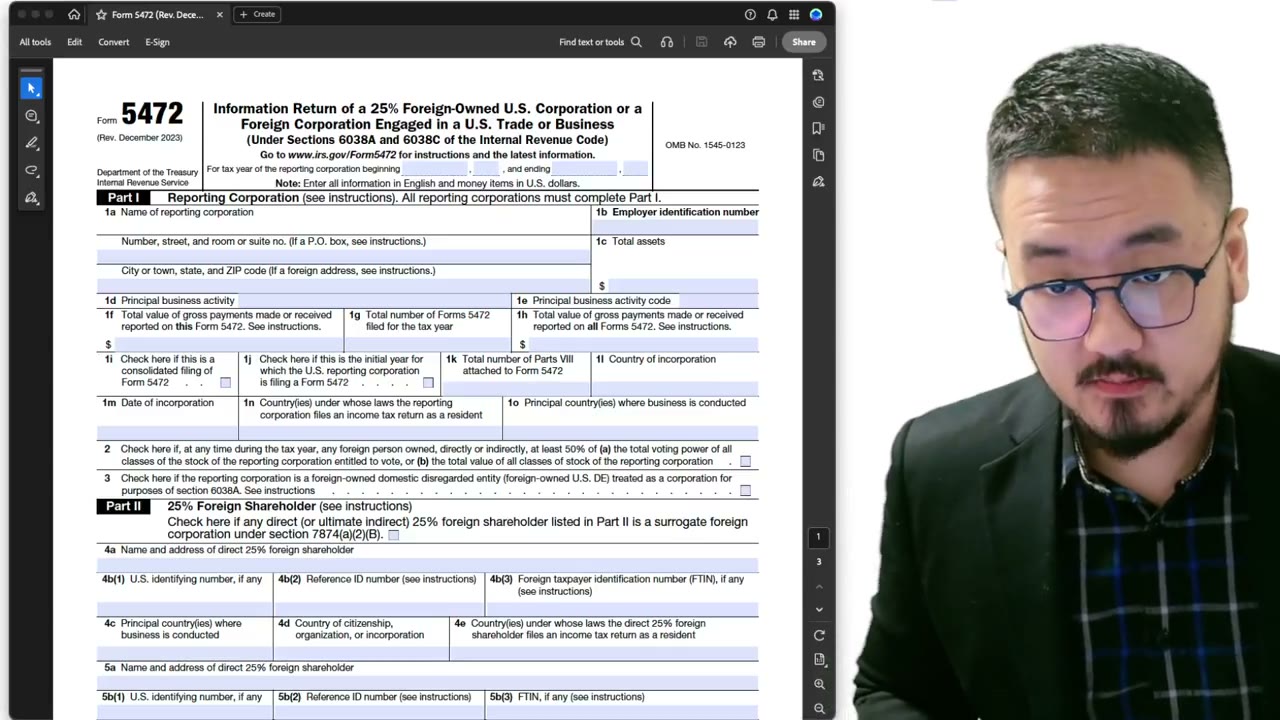

Form 5472 Part III: Why "Principal Country" Is the Related Party's Country, Not the LLC's

Key Takeaways

- Part III uses the same name, address, and identification numbers as Part II for single-member LLCs

- Reference ID number must be consistent between Part II and Part III — the IRS threads them

- Principal country of business in Part III is the RELATED PARTY's operating country, not the LLC's

- Country where related party files income tax as a resident = foreign country (your home country)

- Avoid putting USA in Part III country fields by default — for foreign-owned LLCs, the related party is foreign

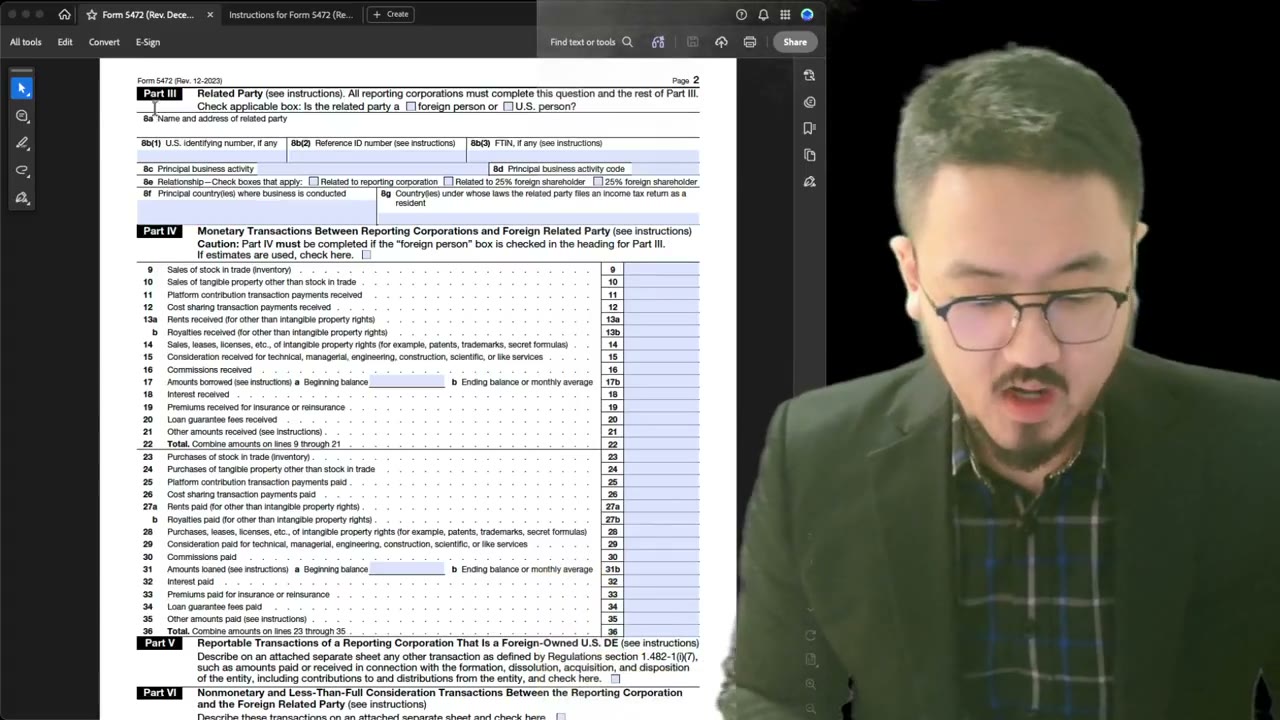

Part III, Continued: Copy Information from Part II

When you're filling Part III for a single-member LLC where you're both the 25% shareholder AND the related party, the easiest approach: copy the name and address from Part II directly into Part III. Same name, same address, same U.S. ID (if any), same reference ID, same foreign TIN.

The IRS expects this consistency. Mismatches between Part II and Part III for the same person look like data-entry errors and trigger correspondence asking for clarification.

Reference ID Number — Use the Same One

If you assigned yourself a reference ID number in Part II (e.g., "WANG-LLC-25"), use the exact same number in Part III. This is the IRS's threading mechanism — they use the reference ID to confirm Part II's shareholder and Part III's related party are the same person, not two distinct foreigners.

If you used a numbering system in Part II (1, 2, 3 for multiple shareholders), keep that numbering consistent in Part III. The first shareholder in Part II becomes the first related party in Part III, and the IDs match across both.

Principal Business Activity — Same as LLC's Business

For a single-member LLC, the related party's (your) principal business activity is typically the same as the LLC's. You are a sole foreign owner whose primary business is running this LLC. Use the same NAICS-style code you used on Form 1120 (and on the LLC's own activity field).

For more complex structures (holding companies, multi-tier ownership), the related party's business activity may differ. Look it up in the Form 1120 instructions activity code table and pick what actually describes that entity's primary work.

Principal Country Where Business Is Conducted: NOT the LLC's Country

This is a frequently confused field. Part III is about the RELATED PARTY (you) and where YOUR business operates — not where the LLC operates.

If you're a Singapore resident running a Delaware LLC from Singapore: the LLC's principal country of business may be Singapore (Part I, item 1o) AND your personal principal country of business is also Singapore. They happen to match here. But if you lived in China and ran a Delaware LLC remotely while traveling, the LLC's principal country might be China (where you make decisions) and your personal country might also be China — again matching.

The key is: don't put USA here just because the LLC is U.S.-formed. Put the country where you, the related party, actually conduct your business activity.

Country Where the Related Party Files Income Tax as a Resident

Field 1i in Part III asks where the related party (you) files income tax as a resident. For a foreign individual owner, this is your personal tax residency — wherever you file your personal income tax return. China, Singapore, Japan, UK, etc.

IMPORTANT: Don't write USA here unless you're actually a U.S. tax resident (which would be unusual for a foreign owner, but possible if you have a green card or pass the substantial presence test). The default for most foreign-owned LLC owners is your home country.

The Common Mistake: Filling USA Everywhere

I've seen YouTube tutorials and online articles where the filer puts "USA" in every country field on Part III, presumably reasoning "the form is U.S., so USA goes in all the country fields." Wrong. The fields are asking about the related party, which for foreign-owned LLCs is a foreign person living in a foreign country.

For Part III, the country fields should usually reflect the related party's foreign residency. The only field where USA naturally appears in Part III is if the related party happens to be U.S.-based (uncommon — Form 5472 is about foreign related parties).

Don't Forget the Relationship Check Boxes (Multi-Check)

At the bottom of Part III is the relationship check box section: related to the reporting corporation, related to 25% foreign shareholder, 25% foreign shareholder. As covered before — these are multi-check, not single-select. Check every applicable box.

For a single-member foreign owner: definitely check "25% foreign shareholder" (you own 100%). If the legal characterization also makes you "related to the reporting corporation," check that too. The IRS prefers over-disclosure to under-disclosure on relationship characterization.

Wrapping Up Part III, Moving to Part IV

Once Part III is complete (with full info on every related party, the consistency with Part II preserved, the country fields correctly reflecting foreign residencies, and all applicable relationship boxes checked), you're done with the identification section. The next part — Part IV — is where the actual transaction amounts go.

Part IV is the most computational part of the form. It's also where the failure-to-disclose penalties most often bite, because Part IV is what the IRS uses to understand whether the cross-border money flow needs scrutiny.

Frequently Asked Questions

What if I'm a U.S. green-card holder running a U.S. LLC — is the related party still 'foreign'?

If you're a U.S. resident for tax purposes (substantial presence or green card), you're not a foreign related party — and the foreign-owned-LLC framework may not apply. Consult a CPA, because your filing requirements differ from a true foreign owner.

Can the LLC be its own related party?

No. The LLC is the reporting corporation. Related parties are external persons or entities (typically the owner and the owner's affiliates) — not the corporation itself.

What if the related party doesn't have a principal business activity (they're retired, etc.)?

Use the activity code that best describes their economic role. For a retired individual whose primary economic activity is investment management, use a financial-services-related code. For someone whose only economic activity is owning this LLC, mirror the LLC's activity code.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

8:25

8:25Form 5472 Part I: Why the Reporting Corporation Files Income Tax as a U.S. Resident

3:35

3:35Form 5472 Part III: Why You Must Fill Even If You Already Did Part II

Form 5472 Part VI — Do You Need a Statement About the Owner-Manager Relationship?

Form 5472 Part VI Attachment: Owner-Manager Nonmonetary Transaction Disclosure

Form 5472 Part 1d — Principal Business Activity Code for Foreign-Owned LLCs

Form 5472 Business Activity Code: Which Code to Use for Your Foreign-Owned LLC (2025-2026)

Form 5472 Field-by-Field Guide for Foreign-Owned LLCs

Form 5472 Field-by-Field Guide for Foreign-Owned LLCs (2025-2026)

Separate Form 5472 for Each Related Party Guide