Form 5472 Part III: Why You Must Fill Even If You Already Did Part II

Key Takeaways

- Part III is mandatory even if the related party is the same person as the Part II shareholder — DO NOT skip

- For single-member LLCs: copy-paste Part II answers into Part III; the same person fills both contexts

- Use attachments for more than 8 related parties, formatted to mirror the Part III block

- Principal country of business for the related party = where THEY operate, not where the LLC operates

- Multi-check the relationship boxes — they're NOT mutually exclusive; check every one that applies

Part III Is Mandatory Even If You Already Filled Part II

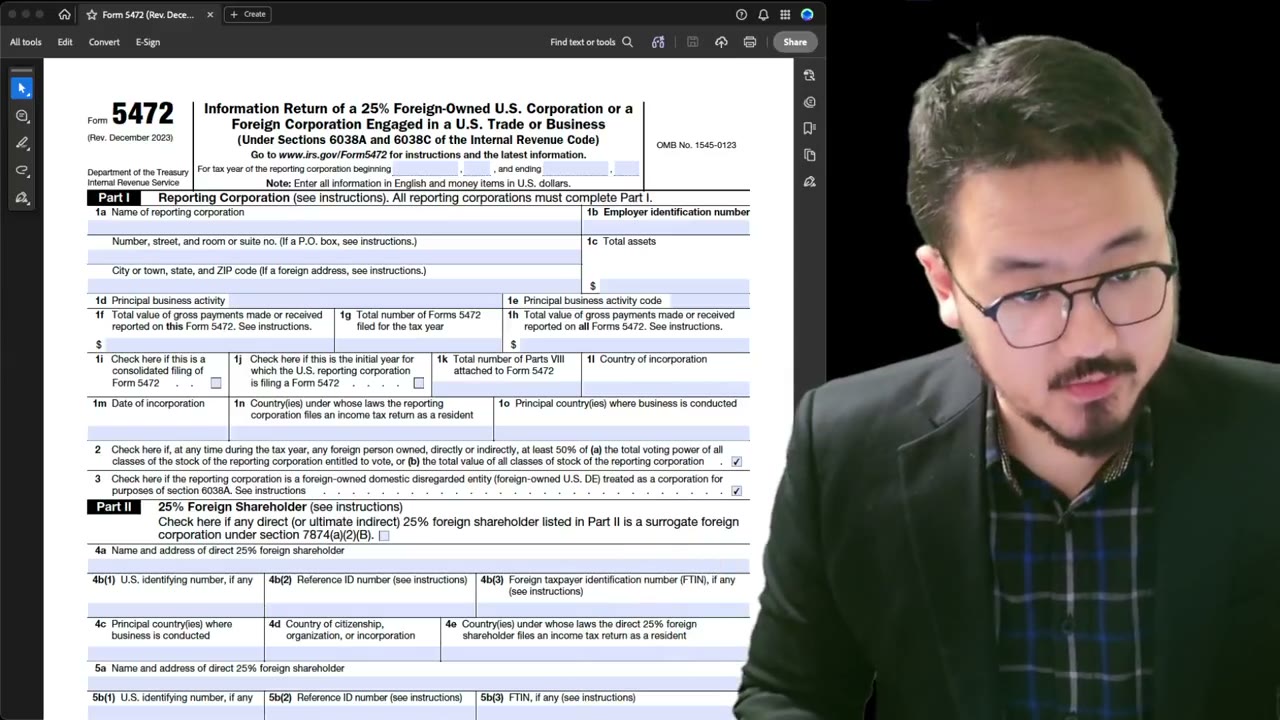

Form 5472 Part III asks for related-party information. The single most common mistake on this form: filers fill Part II (25% foreign shareholder), see Part III asking about "related party," assume it's a different scenario, and skip Part III entirely.

Wrong. Even when the 25% foreign shareholder from Part II IS the same person as the related party in Part III (which is typical for single-member LLCs — you are both), you still must complete Part III. Skipping it because "I already mentioned this in Part II" is the most common cause of penalty-triggering omissions on Form 5472.

Why the Form Asks Twice

Part II is about ownership structure: "who holds 25% or more of this corporation?" Part III is about transaction parties: "who are the related parties whose transactions with the corporation we're reporting?" The same person can answer both questions, but the IRS wants them captured in both contexts.

In a single-member LLC, the owner is both the 25%+ shareholder (Part II) and the related party with transactions (Part III). Fill the same info in both — don't skip Part III thinking the duplication is wasted effort.

What to Fill in Part III

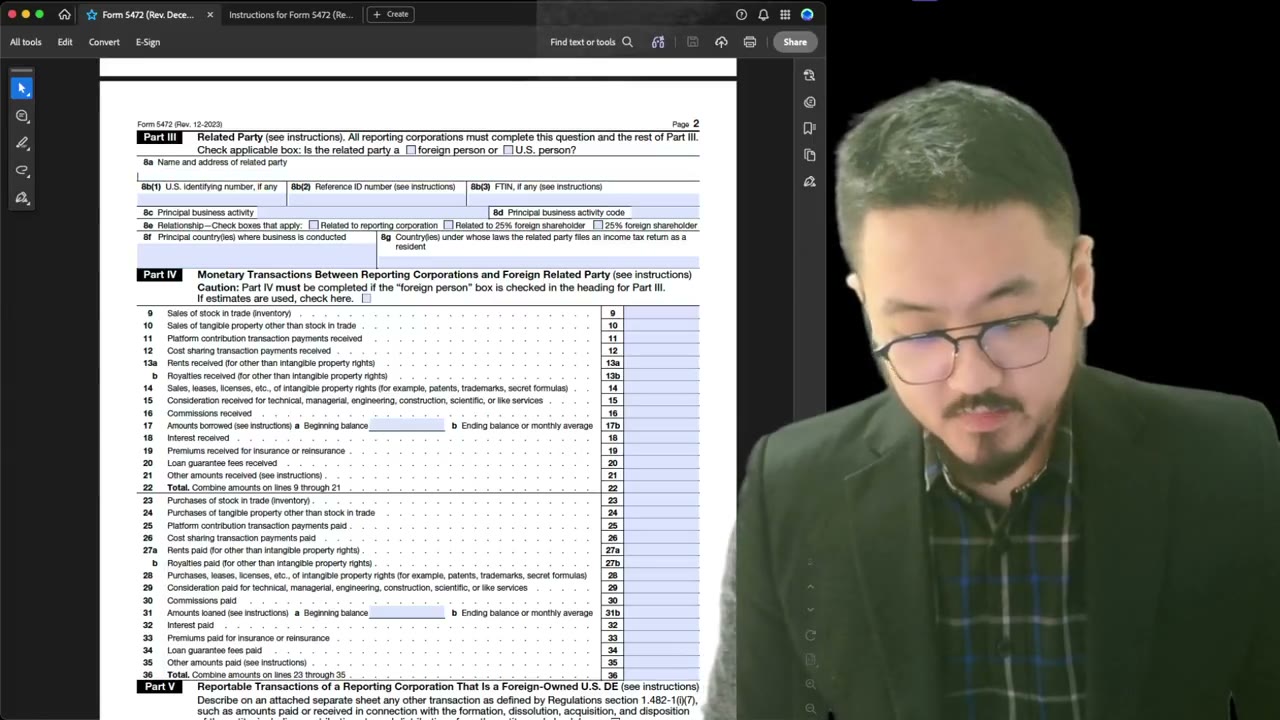

Part III asks for the same fields as Part II: name, address, U.S. identification number, reference ID number, foreign TIN, principal business activity (with code), principal country where the related party conducts business, country of citizenship, and country where the related party files income tax as a resident.

For a single-member LLC where you are the sole shareholder AND sole related party: copy-paste your Part II answers into Part III. The information should match exactly. Don't introduce variations "to look different" — the IRS expects consistency.

Multiple Related Parties Use Attachments

Part III provides space for up to eight related parties. If you have more than eight (rare for single-member LLCs, common for complex multi-party structures), use attachments. Format the attachment to mirror the Part III block structure — name, address, identification numbers, country fields — and reference the attachment with a note like "See Attachment for additional related parties."

Principal Business Activity for the Related Party

For a personal/individual related party (you as the owner of a single-member LLC), the principal business activity is what you do personally as a business — typically the same as the LLC's business since you're the sole driver of it.

For a corporate related party (e.g., your home-country company that has a stake in the LLC), it's that corporation's primary business activity, which may differ from the LLC's. Be specific and use the IRS-published activity codes from the Form 1120 instructions.

Principal Country Where Business Is Conducted (Related Party's Side)

This field is where the RELATED PARTY conducts its business — not the LLC's operating country. For an individual owner who lives and works in Singapore, the related party's principal country of business is Singapore, not the U.S.

For a corporate related party in Japan, it's Japan. Don't write "USA" here just because the LLC is American — that confuses the related-party characterization. The IRS uses this to understand cross-border transaction context.

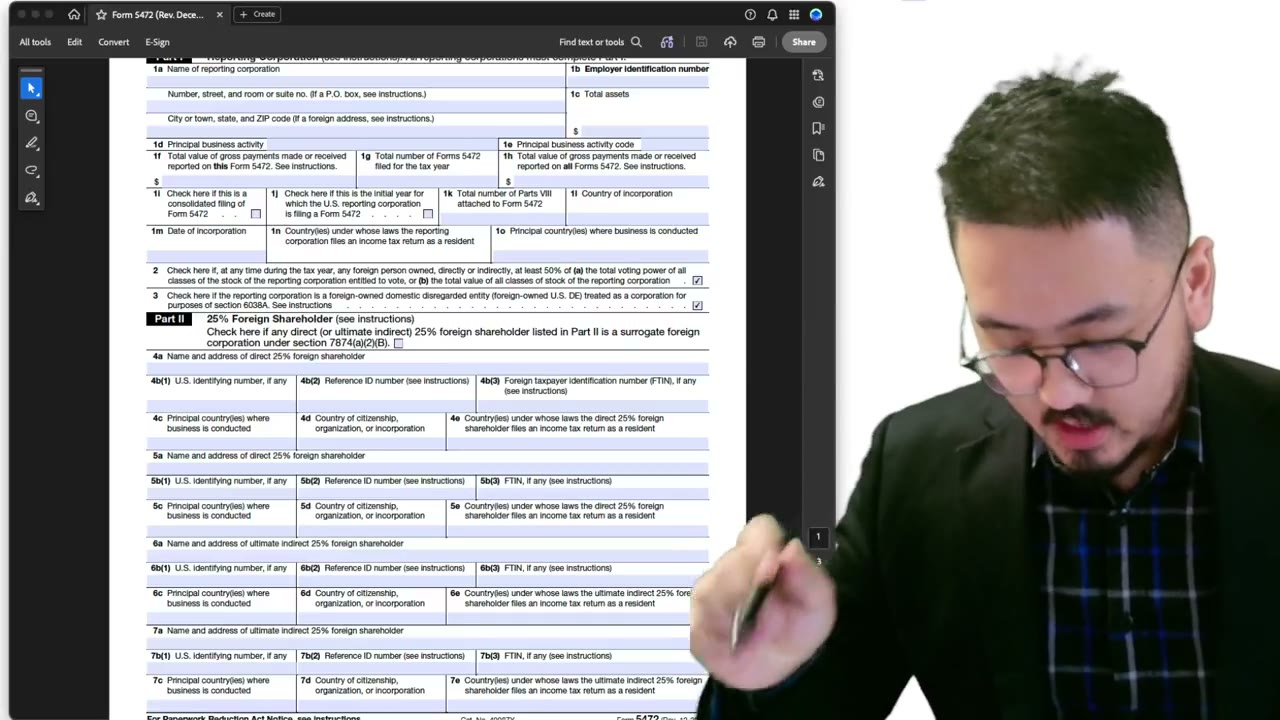

Check Boxes Apply — Multiple Are Allowed

Part III has check boxes for: "related to the reporting corporation," "related to 25% foreign shareholder," and "25% foreign shareholder." These are NOT mutually exclusive — you can (and often should) check multiple.

For a single-member LLC where you are the owner: check "25% foreign shareholder" (because you own 100%, which is more than 25%). If your relationship also qualifies under other definitions (you're related to the corporation as a sole shareholder, related to yourself as the 25%+ shareholder), check those too. Online articles and YouTube videos often only check one — that's incomplete. Multi-check whatever applies.

Frequently Asked Questions

Is filling Part II and Part III with the same info really required?

Yes. The IRS sees the duplication as confirmation, not redundancy. Skipping Part III because Part II already says it triggers an incomplete-form flag, which can lead to a $25,000 penalty for failure to file Form 5472 completely.

What goes in 'related to 25% foreign shareholder' vs '25% foreign shareholder'?

"25% foreign shareholder" means you ARE the shareholder. "Related to 25% foreign shareholder" means you have a familial, business, or control relationship with the shareholder but aren't the shareholder yourself. For single-member self-ownership, only "25% foreign shareholder" applies. For a spouse or business partner of the shareholder, the "related to" box would also apply.

Can the related party be the LLC itself?

No — the LLC is the reporting corporation, not a related party. Related parties are people or entities the LLC transacts with. The LLC reports its own information separately in Form 5472's identity section.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

2:10

2:10Form 5472: Why the §1.6038A-2 Attachment Is Mandatory (Don't Skip)

Form 5472 Explained — What It Is, Who Must File, and How It Works

Form 5472 Explained: What It Is, Who Must File, and How It Works (2025-2026)

5:45

5:45Form 5472 Part III: Why "Principal Country" Is the Related Party's Country, Not the LLC's

1:55

1:55Pro Forma 1120 + Form 5472: Why Dormant LLCs Still Owe the $25,000 Filing

1:49

1:49When Must Your LLC File Form 5472? Avoid the $25,000 IRS Penalty

3:20

3:20