Form 8379 Community Property Allocation Guide (2025-2026)

How to approach this

A source-based path from understanding the rule to filing and recordkeeping.

Determine the requirement

Confirm whether and how the rule applies to you.

Identify the forms

Map the requirement to the specific IRS forms involved.

Prepare and file

Complete the forms accurately and submit on time.

Retain records

Keep documentation supporting every figure you report.

Key Takeaways

- Community-property rules can materially change the injured-spouse refund calculation.

- The IRS uses each state's marital-property rules rather than a single national shortcut.

- Earned income credit is allocated based on each spouse's earned income.

- A detailed separate-return style allocation worksheet strengthens the filing.

Community property changes the refund-allocation math before the IRS even reaches the debt

The Instructions for Form 8379 list nine community-property states and say special rules apply to the injured-spouse refund calculation if the couple lived in one of those states and intended to establish a permanent home there. The instructions also say the IRS will apply each state's rules to determine how much of the joint overpayment, if any, is refundable to the injured spouse.

So the allocation exercise is not purely federal arithmetic. State marital-property rules can reshape the refund before the offset rules finish their work.

Overpayments are often treated as joint property, but not every component is handled the same way

The same instructions say that in community-property states, overpayments are generally considered joint property and are generally applied to legally owed past-due obligations of either spouse, but there are exceptions. They also say earned income credit is allocated to each spouse based on each spouse's earned income.

This is why a couple cannot simply divide the refund down the middle and assume the IRS will do the same thing.

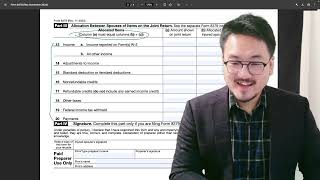

The best file reconstructs the return as if the spouses had filed separately

The Instructions for Form 8379 say each spouse must allocate wages, self-employment income and expenses, withholding, and many credits as if a separate return had been filed. Other items that do not clearly belong to either spouse may be divided equally. That means bookkeeping detail matters far more than people expect from a 'refund form.'

If the household moved between community-property and non-community-property states during the year, the timeline needs to be especially clear.

Frequently Asked Questions

Which states trigger community-property rules for Form 8379?

The Instructions for Form 8379 list Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

Is a joint overpayment always split 50-50 in a community-property state?

Not always. The instructions say overpayments are generally joint property but also note exceptions and state-specific rules.

How is earned income credit handled on Form 8379 in a community-property state?

The instructions say earned income credit is allocated to each spouse based on each spouse's earned income.

IRS Form 8379 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 8379 Injured Spouse

Form 8379 Injured Spouse Offset Guide

Form 8379 Injured Spouse Offset Guide (2025-2026)

6:45

6:45Form 8379: How to Allocate Items Between Spouses on Joint Return

4:18

4:18Form 8379: Injured Spouse Allocation Introduction

5:33

5:33Form 8379: Who Qualifies as the Injured Spouse?

J-2 Spouse Payroll and FICA Guide

J-2 Spouse Payroll and FICA Guide (2025-2026)

FIRPTA Residence Exception Guide