Form 8379 Injured Spouse Offset Guide (2025-2026)

How to approach this

A source-based path from understanding the rule to filing and recordkeeping.

Determine the requirement

Confirm whether and how the rule applies to you.

Identify the forms

Map the requirement to the specific IRS forms involved.

Prepare and file

Complete the forms accurately and submit on time.

Retain records

Keep documentation supporting every figure you report.

Key Takeaways

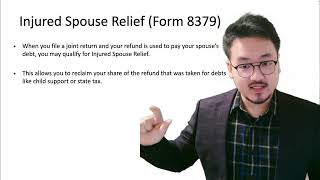

- Form 8379 allocates a joint overpayment after an offset tied to the other spouse's debt.

- It is different from Form 8857 and should not be used for innocent-spouse liability relief.

- Offsets can arise from tax, child-support, unemployment, and federal nontax debts such as student loans.

- The form can be filed with the return, with an amended return, or separately afterward.

Form 8379 is a refund-allocation tool, not a liability-forgiveness request

The Instructions for Form 8379 say the form is filed by one spouse on a joint return when all or part of that spouse's share of the overpayment was, or is expected to be, applied against the other spouse's legally enforceable past-due obligation. The instructions also tell taxpayers not to use Form 8379 when claiming innocent spouse relief and instead to file Form 8857 for that purpose.

That line matters because taxpayers often use the phrase 'innocent spouse' loosely when the actual issue is that Treasury intercepted the refund.

The list of offsettable debts is broader than many couples expect

The instructions say offsets can apply to a spouse's past-due federal tax, state income tax, state unemployment compensation debts, child support, or federal nontax debt such as a student loan. So the refund problem can start even when the IRS itself is not the main creditor.

A taxpayer who receives a Bureau of the Fiscal Service notice should therefore stop asking only 'what does the IRS think?' and instead identify which debt program triggered the offset.

The filing options are flexible, but the supporting documents matter

The instructions say Form 8379 can be filed with the joint return, with an amended joint return claiming an additional refund, or later by itself after the original joint return has been filed. If filed separately, the spouse should attach copies of Forms W-2, W-2G, and any Forms 1099 showing withholding. The instructions also give a limitations period: generally three years from the due date of the original return, including extensions, or two years from the date the tax was paid, whichever is later.

That means late cleanup is possible, but only if the refund-allocation file is built carefully.

Frequently Asked Questions

What is Form 8379 for?

It is used by an injured spouse on a joint return to recover that spouse's share of a joint overpayment that was applied to the other spouse's past-due obligation.

Can a student loan trigger an offset that makes Form 8379 relevant?

Yes. The Instructions for Form 8379 list federal nontax debts such as student loans among the debts that can trigger an offset.

Can I file Form 8379 after the original joint return was already processed?

Yes. The instructions say the form can be filed afterward by itself if the original joint return has already been filed.

IRS Form 8379 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 8379 Injured Spouse

Form 8379 Community Property Allocation Guide

Form 8379 Community Property Allocation Guide (2025-2026)

6:45

6:45Form 8379: How to Allocate Items Between Spouses on Joint Return

5:33

5:33Form 8379: Who Qualifies as the Injured Spouse?

4:18

4:18Form 8379: Injured Spouse Allocation Introduction

J-2 Spouse Payroll and FICA Guide

J-2 Spouse Payroll and FICA Guide (2025-2026)

Form 709-NA Noncitizen Spouse Gift Guide