Form 8832 Entity Classification Election: Step-by-Step Instructions (Part 2)

Key Takeaways

- Specify whether your entity is newly formed or changing an existing classification

- Foreign owners can elect disregarded entity (default) or C-Corporation — not S-Corp

- The election must be filed within 75 days before to 12 months after the effective date

- The form must be signed by an authorized person (typically the LLC owner)

Part I: Election Information

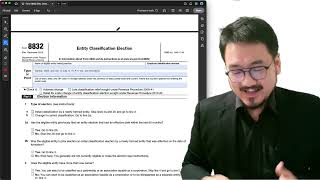

The first part of Form 8832 asks for your entity's basic information and the classification you want to elect. You need to specify whether you are a newly formed entity or an existing entity changing its classification.

For newly formed entities, you can choose your classification effective from the formation date. For existing entities, you specify the date you want the new classification to take effect.

Choosing Your Classification

The form provides several classification options. For a single-member LLC with a foreign owner, the relevant choices are typically: disregarded entity (the default, no filing needed) or association taxable as a corporation. If you want to be taxed as a corporation, you would check the appropriate box and specify the effective date.

Remember that S-Corporation status is not available to foreign owners, so this election would make you a C-Corporation.

Filing and Signature Requirements

Form 8832 must be signed by an authorized representative of the entity — typically the owner for a single-member LLC. The form should be filed with the IRS no later than 75 days before or 12 months after the desired effective date of the election.

Frequently Asked Questions

When should I file Form 8832?

File no later than 75 days before or 12 months after the date you want the new classification to take effect. If you miss this window, you may need to use Part II (Late Election Relief).

What if I file Form 8832 late?

Part II of Form 8832 provides Late Election Relief. You must provide a reasonable cause explanation for why the election was not filed on time. The IRS may accept the late filing if you meet certain conditions.

IRS Form 8832 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 8832 Entity Classification

5:23

5:23Form 8832 Entity Classification Election: Key Rules You Must Know (Part 3)

5:56

5:56Form 8832 Entity Classification Election: How It Works (Part 1)

Form 8832 Entity Classification Guide

Form 8832 Entity Classification Guide for Foreign-Owned LLCs

Form 8832 Effective Date Window Guide

Form 8832 Effective Date Window Guide for Foreign-Owned LLCs (2025-2026)

Late Form 8832 Relief Guide

Late Form 8832 Relief Guide for Foreign-Owned LLCs (2025-2026)

Form 8832 60-Month Rule Guide