Head of Household With a Nonresident Spouse Guide (2025-2026)

Nonresident return flow (Form 1040-NR)

How a nonresident individual reports U.S.-source income to the IRS.

Classify the income

Effectively connected (ECI) vs. fixed/determinable (FDAP).

Gather U.S.-source documents

1042-S, K-1, or other statements of U.S. income.

Prepare Form 1040-NR

ECI on the main form; FDAP on Schedule NEC.

File and reconcile withholding

Credit amounts already withheld at source.

Key Takeaways

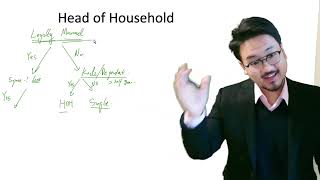

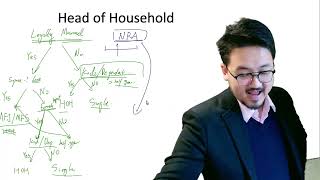

- A taxpayer with a nonresident spouse may be considered unmarried for head-of-household purposes if no resident election is made.

- The nonresident spouse cannot serve as the qualifying person for head-of-household status.

- A separate qualifying person and the other head-of-household tests still have to be met.

- Community-property and related-benefit rules can complicate the final answer.

A nonresident spouse can leave the head-of-household lane open, but only if no resident election is made

Publication 501 says a taxpayer is considered unmarried for head-of-household purposes if the spouse was a nonresident alien at any time during the year and the taxpayer does not choose to treat that spouse as a resident alien. That is one of the most misunderstood filing-status rules in international households because people assume any legal marriage blocks head-of-household treatment automatically.

The rule is narrower than that. The marriage still exists, but for head-of-household testing the IRS can treat the taxpayer as unmarried if the election to treat the spouse as resident is not used.

The spouse cannot be the qualifying person

Publication 501 also says the nonresident spouse is not a qualifying person for head-of-household purposes. The taxpayer still needs another qualifying person and still has to satisfy the normal head-of-household tests, including home-cost and residency requirements where applicable.

That matters in founder families where the spouse lives abroad but the child or another qualifying relative does not meet the dependency or residency rules. The nonresident spouse alone never finishes the analysis.

The filing-status choice also affects other items in the return

Publication 501 warns that different tests can apply for different tax benefits and notes that special community-property rules may matter in some situations. So the right process is not to start with the label 'head of household' and work backward. It is to test whether the resident-spouse election is being made, whether there is a real qualifying person, and whether the household-cost facts support the position.

When those elements are documented together, the filing status becomes much easier to defend.

Frequently Asked Questions

Can my nonresident spouse be my qualifying person for head of household?

No. Publication 501 says the nonresident spouse is not a qualifying person for head-of-household purposes.

What happens if I elect to treat my nonresident spouse as a resident?

That usually closes the head-of-household route because Publication 501's considered-unmarried rule for a nonresident spouse applies only if you do not make the resident election.

Can I still file head of household if my child lives with me and my spouse lives abroad?

Potentially yes, but only if you do not elect resident treatment for the spouse and you otherwise meet the qualifying-person and home-cost rules in Publication 501.

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Filing Status Guide

Nonresident Spouse Joint Return Election Guide

Nonresident Spouse Joint Return Election Guide Under Section 6013(g) (2025-2026)

Standard Deduction After a Nonresident Spouse Election Guide

Standard Deduction After a Nonresident Spouse Election Guide (2025-2026)

Dual-Status Spouse Resident Election Guide

Dual-Status Spouse Resident Election Guide Under Section 6013(h) (2025-2026)

Applied For EIN on Returns and Deposits Guide

Applied For EIN on Returns and Deposits Guide (2025-2026)

8:40

8:40Head of Household Filing Status: Decision Tree Guide (Part 1)

5:31

5:31