Standard Deduction vs Itemized Deduction: Quick Comparison

Key Takeaways

- Standard deduction is a flat amount that varies by filing status and adjusts for inflation annually

- Itemizing means listing specific qualifying expenses that may exceed the standard deduction

- You must choose one or the other — cannot claim both standard and itemized deductions

- Common itemized deductions: medical expenses, state/local taxes, mortgage interest, charitable donations

- Since TCJA, fewer taxpayers benefit from itemizing due to the higher standard deduction

Standard Deduction: The Simple Choice

The standard deduction is a flat dollar amount that reduces your taxable income. It is essentially an automatic deduction available to all taxpayers. The amount varies by filing status and is adjusted annually for inflation. For most taxpayers, the standard deduction is the simpler and often more beneficial choice.

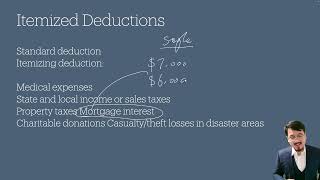

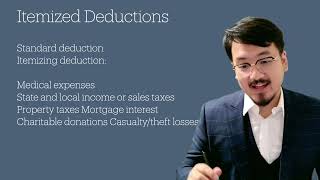

Itemized Deductions: When Your Expenses Add Up

Itemizing means listing out specific qualifying expenses that exceed the standard deduction amount. Common itemized deductions include medical expenses (above a percentage of AGI), state and local income or sales taxes, property taxes, mortgage interest, and charitable donations. Casualty and theft losses in federally declared disaster areas may also qualify.

You must choose between the standard deduction and itemizing — you cannot claim both. The rational approach is to calculate your total itemized deductions and compare them to the standard deduction, then choose whichever is larger.

Making the Right Choice

For a single filer, if your itemized deductions (mortgage interest, property taxes, state taxes, charitable donations, etc.) total more than the standard deduction amount, itemizing saves you more money. If your itemized deductions total less, take the standard deduction.

Since the Tax Cuts and Jobs Act significantly increased the standard deduction, fewer taxpayers benefit from itemizing. However, homeowners with large mortgages, taxpayers in high-tax states, and those making substantial charitable contributions often still benefit from itemizing.

Frequently Asked Questions

Can I switch between standard and itemized deduction each year?

Yes. You can choose whichever method benefits you more each tax year. There is no requirement to be consistent from year to year.

Is there a limit on state and local tax deductions?

Yes. The SALT (State and Local Tax) deduction is currently capped at $10,000 per return. This includes state income taxes (or sales taxes) and property taxes combined.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Tax Basics & Filing Requirements

7:17

7:17Standard vs Itemized Deduction: Important Catches Part 1

5:43

5:43Standard vs Itemized Deduction: Important Catches Part 2

5:28

5:28Business vs Personal Expenses: Tax Deduction Grey Areas Explained

8:07

8:07Essential IRS Forms and Due Dates Quick Reference Guide

3:15

3:15How to Find and Download IRS Forms, Publications, and Instructions

1:39

1:39