US LLC Tax Guide for Japan Residents

Everything Japan residents need to know about US LLC tax obligations, treaty benefits, ITIN requirements, and compliance deadlines.

Quick Summary

Tax Treaty

Yes — treaty in effect

ITIN

Usually required

E-2 Visa

Eligible

US Tax Obligations for Foreign-Owned LLCs

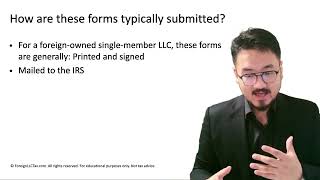

Every foreign-owned single-member LLC that is treated as a disregarded entity must file the following with the IRS, regardless of whether the LLC earned any income:

Form 5472 + Pro Forma Form 1120

Reports transactions between the LLC and its foreign owner (e.g., capital contributions, distributions, loans). Must be filed even if no reportable transactions occurred during the year. Penalty for failure to file: $25,000 per form.

Deadline: April 15 (or extended to October 15)

The Form 5472 is due on the 15th day of the 4th month after the tax year ends (April 15 for calendar year filers). An automatic 6-month extension is available by filing Form 7004.

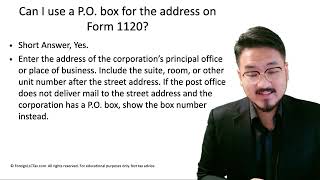

EIN (Employer Identification Number)

Your LLC must have an EIN before filing. Apply using Form SS-4 online, by fax, or by mail. Foreign owners without an SSN can apply by fax or use our EIN application tool.

Tax Treaty Benefits

The US-Japan tax treaty is a modern, comprehensive agreement that provides strong protections against double taxation. It offers some of the lowest withholding rates of any US tax treaty, with 0% on royalties and favorable rates on dividends and interest.

Treaty Withholding Rates

0–10%

Dividends

0–10%

Interest

0%

Royalties

Treaty rates apply to specific types of income. A single-member LLC that is disregarded for US tax purposes generally does not itself earn dividends, interest, or royalties in the traditional sense. However, these rates become relevant if the LLC elects corporate treatment or if you have other US-source income. Use our Treaty Lookup Tool to explore the full treaty provisions.

ITIN Requirements

Usually needed. Japanese residents typically do not have a US SSN and must apply for an ITIN.

How to Apply for an ITIN

- 1Complete IRS Form W-7 with your tax return

- 2Provide original identification documents (passport) or certified copies

- 3Submit by mail to the IRS ITIN Operation, or through a Certifying Acceptance Agent (CAA)

- 4Processing typically takes 7–11 weeks

Local Tax Reporting in Japan

The NTA (National Tax Agency) requires worldwide income reporting. US LLC income must be reported through Kakutei Shinkoku (確定申告) — the annual tax return. A foreign tax credit is available to offset US taxes paid.

Important: Tax laws change frequently. The information above is for general guidance only. Always consult a qualified tax professional in Japan who is familiar with US LLC structures to ensure accurate reporting and compliance.

Special Considerations for Japan Residents

Japanese citizens are eligible for the E-2 Treaty Investor visa. Japan is a very active market for US LLC formation, particularly for e-commerce and digital service businesses. Language barriers may require bilingual tax professionals. Japanese tax advisors (Zeirishi) experienced with US structures are recommended.

E-2 Treaty Investor Visa: As a Japan national, you are eligible for the E-2 visa, which allows you to live and work in the US to direct and develop your US business. This requires a substantial investment in the US enterprise.

Common Formation States

Japan residents most commonly form their US LLC in the following states:

Delaware

Most established business law in the US. Court of Chancery specializes in business disputes. No state income tax on out-of-state revenue. Privacy protections for owners.

Wyoming

No state income tax. Lowest annual fees. Strong asset protection. No franchise tax. Lifetime proxy allowed.

Ready to Get Started?

Whether you need to form a new LLC, get an EIN, or file your annual Form 5472, we have the tools to help Japan residents stay compliant.