Transfer Pricing for Foreign-Owned LLCs

How the IRS reviews transactions between you and your LLC — and how to document them properly on Form 5472.

Key Facts

What Is Transfer Pricing?

Transfer pricing refers to the pricing of transactions between related parties. For foreign-owned LLCs, this means any financial transaction between the LLC and its foreign owner (or other related entities).

The IRS requires that these transactions be conducted at "arm's length" — meaning the terms should reflect what unrelated parties would agree to in a comparable transaction. This prevents related parties from manipulating prices to shift profits out of the U.S. or otherwise avoid U.S. tax obligations.

For most foreign-owned single-member LLCs (which are treated as disregarded entities for tax purposes), transfer pricing primarily concerns the accurate reporting of transactions on Form 5472, Part V.

Why Transfer Pricing Matters for Foreign-Owned LLCs

The IRS specifically scrutinizes transactions between foreign owners and their U.S. LLCs because these transactions occur between related parties who can set whatever terms they choose. Unlike arm's length transactions between strangers, there is no market mechanism to ensure fair pricing.

- Form 5472 is the IRS's primary tool for monitoring these transactions

- Even disregarded entities (single-member LLCs) must report all related-party transactions

- The $25,000 penalty for non-compliance underscores how seriously the IRS takes this

- Inadequate documentation can trigger audits and additional penalties

Key point: Even if your LLC has zero income and zero U.S. tax liability, you must still report all transactions with the foreign owner on Form 5472. The IRS wants to see the complete picture.

Common Related-Party Transactions

For most foreign-owned single-member LLCs, these are the typical transactions that occur between the owner and the LLC:

Capital Contributions

The owner transfers money into the LLC's bank account to fund the business. This is the most common transaction for new LLCs.

Example: Owner wires $5,000 to the LLC's Mercury bank account to cover startup costs.

Owner Pays for LLC Formation

The owner pays a formation service (like doola or Firstbase) to set up the LLC. This is a related-party transaction even though the payment went to a third party.

Example: Owner pays $500 to Firstbase for LLC formation on behalf of the LLC.

Owner Covers Operating Expenses

The owner pays for software subscriptions, hosting, or other business expenses from their personal account.

Example: Owner pays $200/month for web hosting using their personal credit card.

LLC Reimburses Owner

The LLC sends money to the owner as reimbursement for expenses paid on the LLC's behalf.

Example: LLC reimburses owner $1,200 for hosting costs paid during the year.

Distributions to Owner

The LLC distributes profits to the foreign owner.

Example: LLC distributes $10,000 in profits to the owner's foreign bank account.

Loans Between Owner and LLC

The owner lends money to the LLC (or vice versa). Loan terms should be documented and at arm's length interest rates.

Example: Owner lends $20,000 to the LLC with a 5% annual interest rate, documented in a promissory note.

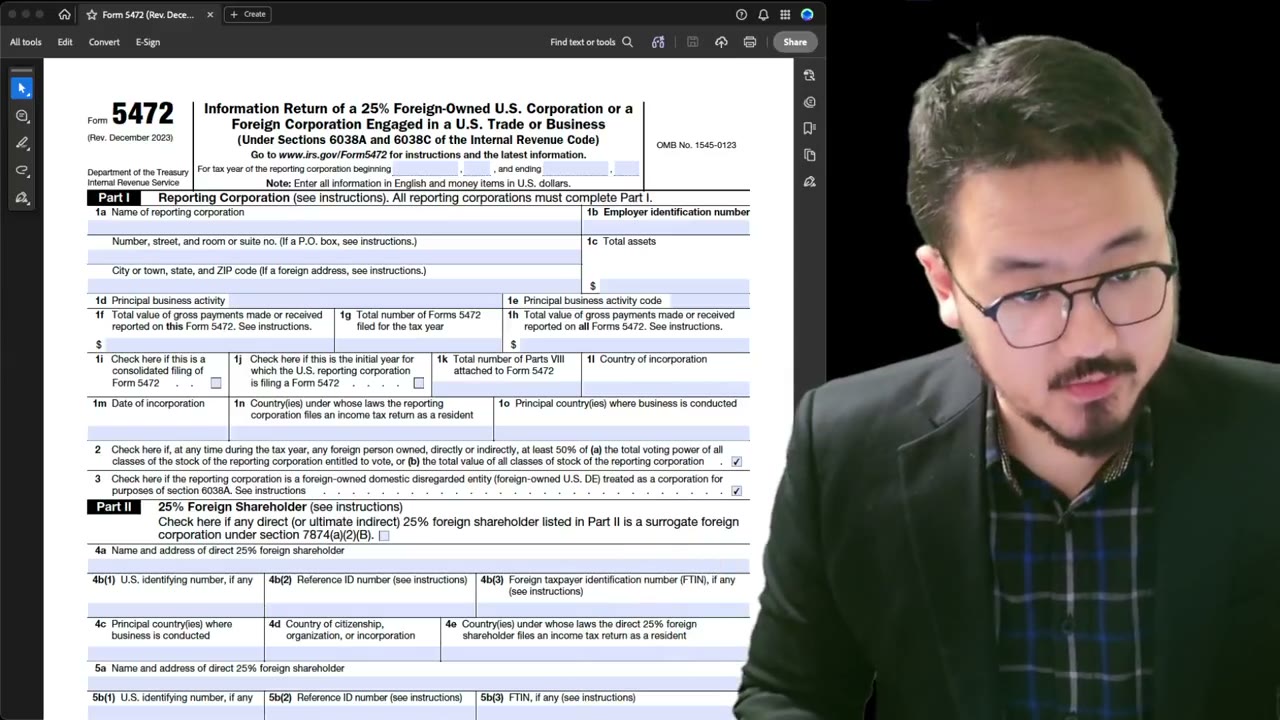

How Form 5472 Part V Captures Transactions

Part V of Form 5472 is titled "Reportable Transactions of a Reporting Corporation with a Foreign or Domestic Related Party." It lists specific transaction categories with dollar amounts:

- Lines 1-7: Sales, purchases, and compensation-related transactions

- Lines 8-12: Commissions, rents, royalties, and interest paid/received

- Lines 13-15: Insurance premiums, service fees, and other amounts

- Lines 16-22: Capital contributions, loans, accounts payable/receivable, and other balances

For most single-member LLCs, the relevant lines are:

- Line 13(b): Other amounts paid to the related party (reimbursements, distributions)

- Line 15(b): Other amounts received from the related party (capital contributions, expense payments)

- Lines 16-22: Loan balances and accounts payable/receivable

Our filer handles this automatically: When you use our Form 5472 filer, Part V is populated based on the transaction information you enter. No need to figure out which lines to use.

The Arm's Length Principle

The arm's length principle (IRC Section 482) requires that transactions between related parties be priced as if they occurred between unrelated parties in comparable circumstances.

For most foreign-owned single-member LLCs, applying the arm's length principle is straightforward:

- Capital contributions: These are at face value — there's no pricing issue.

- Expense reimbursements: Reimburse at actual cost — keep receipts.

- Loans: Charge a market-rate interest. The IRS publishes Applicable Federal Rates (AFR) monthly.

- Services: If the owner provides services to the LLC, the compensation should reflect market rates.

- IP licensing: If the LLC uses the owner's intellectual property, any royalties should be at market rates.

For most small LLCs:The transactions are simple (contributions and reimbursements) and the arm's length standard is easily met. Complex transfer pricing studies are typically only needed for larger businesses with significant intercompany transactions.

Documentation Requirements

The IRS requires that you maintain records sufficient to establish the correctness of each reported transaction. Good documentation protects you in an audit and strengthens reasonable cause arguments if penalties are assessed.

Bank Statements

Monthly statements showing all transfers between the owner and LLC.

Wire Transfer Records

Confirmation documents for each international transfer.

Invoices and Receipts

For any expenses the owner pays on behalf of the LLC.

Loan Agreements

Written promissory notes for any loans between the owner and LLC.

Operating Agreement

Your LLC's operating agreement defining contribution and distribution terms.

Transaction Log

A simple spreadsheet tracking each transaction with date, amount, description, and category.

Examples of Proper Documentation

Example 1: Capital Contribution

Owner wires $10,000 from their personal bank to the LLC's U.S. bank account.

Example 2: Owner Pays for Software

Owner pays $1,200 for annual software subscription used by the LLC.

Example 3: Owner Loan to LLC

Owner lends $50,000 to the LLC at 5% annual interest.

Penalties for Non-Compliance

Transfer pricing non-compliance for foreign-owned LLCs primarily manifests as Form 5472 penalties:

- $25,000 per form for failure to file, late filing, or filing with incomplete/inaccurate information

- Additional $25,000 for each 30-day period of continued non-compliance after IRS notice

- Record-keeping penalties for failure to maintain adequate documentation

- IRC Section 482 adjustments — the IRS can reallocate income between the owner and LLC if pricing is not at arm's length

Accurate, well-documented reporting on Form 5472 is your best protection against transfer pricing penalties.

Not sure which method fits your deal?

The free method helper asks what your related-party transaction is — goods, a management fee, a royalty, or a loan — and points to the right §482 method, the safe harbor, and the documentation you need.

Open the Transfer-Pricing Method Helper →Picking a §482 Method at Small Scale

Every specified method under Treas. Reg. §1.482 starts from the same gate: the best-method rule. The method you use is whichever one gives the most reliable measure of an arm's-length result given your actual facts and the data you can get. For penalty defense, your choice is only "reasonable" if you concluded the selected method was the most reliable as applied and made a genuine effort to weigh the alternatives. That does not mean running every method to completion — a proportionate file just has to show why one method fit the facts and the others did not.

At one-person-LLC scale, four patterns cover almost everything:

Routine US distributor → CPM (operating-margin)

The comparable profits method (Treas. Reg. §1.482-5) is the workhorse when there are no clean internal comparables. It tests the least-complex party — here, a US LLC that warehouses, processes orders, handles customer service, and sells — on its operating profit relative to sales, with the foreign owner treated as the residual claimant. A thin, benchmarked operating margin is far more defensible than an improvised markup. It weakens fast if the US LLC owns valuable local intangibles or bears the entrepreneurial risk.

Limited-risk reseller → resale-price method

A tangible-goods method (§1.482-3) that tests the controlled purchase price by the gross margin a comparable independent reseller earns. It fits a US LLC that imports finished inventory from a foreign affiliate and resells it with limited functions, limited risk, and no US-created intangibles — and the goods are not physically altered before resale. It is not for pure services, royalties, or loans.

Contract manufacturer → cost-plus

Also a tangible-goods method (§1.482-3): an arm's-length price is production cost plus a comparable gross markup. Natural when the US LLC is a routine producer or contract manufacturer for a foreign affiliate and usable comparable markups exist. Cost-plus logic is a poor primary tool for valuable-IP royalties, which the intangible rules route elsewhere.

Both sides add nonroutine value → profit split

The profit split (§1.482-6) divides combined operating profit from the smallest identifiable activity. In its residual form, routine contributions get a market return first, then the leftover is split by the relative value of each side's nonroutine contributions. For solo LLCs this is the exception — reserve it for when the foreign owner contributes real brand or technology AND the US LLC makes its own demonstrable nonroutine contribution (meaningful US marketing intangibles, technology enhancement, shared strategic control).

Substance beats paper. Under §1.482-1, the IRS can look at actual conduct, disregard contract terms the parties do not follow, and impute terms where no written agreement exists. For a small LLC, owner emails, invoices, project logs, and the real flow of risks and benefits can carry as much weight as the intercompany agreement itself.

The Services Cost Method: Charge Admin at Cost

The Services Cost Method (SCM) under Treas. Reg. §1.482-9 is the single most useful simplification for routine support charges. When it applies, eligible services are priced at total services cost with no markup, SCM is treated as the best method, and the IRS is limited to adjusting the charge to the correctly computed total cost. For a foreign owner billing the US LLC for bookkeeping, payroll, or IT help-desk support, SCM often removes any need for a full markup study.

SCM eligibility has four moving parts, and all must hold:

- Covered service: either a specified covered service (Rev. Proc. 2007-13 lists payroll, AP/AR support, general admin, bookkeeping, accounting, tax-compliance support, recruiting, training, and IT support, among others) or a low-margin service whose median comparable markup on total cost is no more than 7%.

- Not an excluded activity: the exclusions are broader than founders expect — manufacturing, production, extraction, construction, reselling/distribution, R&D, engineering/scientific work, financial transactions (including guarantees), and insurance/reinsurance are all out.

- Passes the business-judgment rule: you must reasonably conclude the service does not contribute significantly to the group's key competitive advantages, core capabilities, or fundamental risks of success or failure.

- Adequate books and records: the cost build-up and allocations have to be documented.

The "management" trap.Routine office administration, bookkeeping, payroll support, tax compliance, and recruiting can ride SCM at cost. Strategic management, product strategy, key pricing decisions, brand stewardship, and IP-development oversight cannot — those are tied to competitive advantage and need another method. Do not bundle the two under one "management fee."

Some "management" is not chargeable at all.Under §1.482-9(l), a service must confer a benefit on the recipient. Duplicative activities generally do not. Activities whose only effect is to protect the renderer's own capital investment, or to meet legal or regulatory requirements specific to the renderer, are shareholder activities— not chargeable to the US LLC under any method. A foreign owner's investor-level oversight or parent-level governance cost should never land in a management charge. Genuine day-to-day operational support that actually benefits the LLC may be charged.

If SCM does not apply, the services rules step you up: a direct comparable fee (§1.482-9(c)), then cost-of-services-plus, then CPM for services, with profit split reserved for genuinely integrated high-value arrangements.

Owner Loans and Royalties

Related-party loans

For owner advances, Treas. Reg. §1.482-2 asks what unrelated parties would charge on a comparable loan — looking at principal, term, security, the borrower's credit, and the prevailing rate at the lender's location. The practical anchor for small LLCs is the AFR safe-haven: a dollar loan rate is treated as arm's length if it sits at 100%–130% of the applicable federal rate (short-, mid-, or long-term AFR matched to the loan term; short-term AFR for demand loans). Charge too little and the floor applies; charge too much and the ceiling applies unless you prove a better market rate.

Thin capitalization is the bigger risk than the rate. §1.482-2 only reaches bona fide debt. A running owner balance with no note, no fixed maturity, no payment history, and no realistic expectation of repayment can be recharacterized as a capital contribution or a distribution even if the stated rate is inside the AFR band. If the instrument is not respected as debt, there may be no deductible interest at all. Keep a real note, maturity, principal schedule, and evidence of actual accruals and payments.

Even where debt is genuine and priced, IRC §163(j) can cap the interest deduction (generally business interest income plus 30% of adjusted taxable income), though the §448(c) small-business gross-receipts exemption keeps many one-person LLCs out of the limit entirely. The order of questions is: is the advance real debt, then price the interest under §482, then test deductibility under §163(j).

Royalties and IP

The intangible rules (Treas. Reg. §1.482-4) are a separate, more demanding branch. The specified royalty methods are the comparable uncontrolled transaction (CUT) method, CPM, profit split, and unspecified methods — note that resale-price and cost-plus are not on the list. A CUT is strongest when the same or comparable IP is licensed externally; small LLCs often overlook an internal CUT, such as the foreign owner licensing the same trademark or software to another market.

Commensurate-with-income / periodic adjustments. IRC §482 requires that income from a transfer or license of intangibles be commensurate with the income the intangible actually produces. The regulations enforce this through periodic adjustments: the IRS can revisit the consideration in a later year to keep it commensurate — even if the original transfer year is closed. A royalty that looked fine when a brand was small can become indefensible once the US market takes off and the file never documented the projections and pricing logic.

The US brand build-out trap.When a US LLC funds and executes meaningful US marketing that enhances a foreign-owned trademark without contemporaneous compensation or a realistic expectation of future benefit, §1.482-4's examples let the IRS look past a simple owner-imposed royalty and ask who actually created the local value. A foreign-owned online store building US-market premium with its own spend cannot assume a flat royalty tells the whole story.

Penalties and the Documentation Defense

Separate from the $25,000 Form 5472 / §6038A penalties already covered, IRC §6662(e) and (h) impose accuracy-related penalties on the income-tax side: a 20% penalty for a substantial valuation misstatement, rising to 40% for a gross misstatement. There are two bases:

- Transactional: the claimed price is 200% or more, or 50% or less, of the correct §482 price (the 40% tier triggers at 400% / 25%).

- Net adjustment: the net §482 adjustment exceeds the lesser of $5M or 10% of gross receipts (the 40% tier at $20M or 20%).

The catch on the net-adjustment basis: §6662 says you get no reasonable-cause relief unless you meet the documentation requirements of Treas. Reg. §1.6662-6. That makes a contemporaneous file the heart of the defense, even at small scale. The principal documents must generally exist when the return is filed and be handed to the IRS within 30 days of request.

The 10 principal documents (§1.6662-6(d)(2)(iii)(B))

- Overview of the business and the economic and legal factors affecting pricing

- Organizational structure / org chart covering all related parties that matter under §482

- Any documentation the §482 regulations specifically require (e.g. an SCM intent statement)

- The selected method and why it was chosen, including whether its requirements were met

- The alternative methods considered and why they were rejected

- The controlled transactions and internal data analyzed, including terms of sale and cost build-ups

- The comparables used, how comparability was judged, and any adjustments

- The economic analysis and projections relied on

- Relevant data obtained after year-end but before filing

- A general index of the principal and background documents and the recordkeeping system

Proportionate is fine.For a one-person LLC this is not an economist's report — it is a low-cost annual file: a short method memo, a one-page related-party chart, written agreements (or a same-day memo of an oral arrangement), a transaction spreadsheet that ties each category to Form 5472 and the return, support for each amount, and a year-end true-up note. Add the SCM intent statement and cost allocations if you use SCM, a small CPM benchmark if you use CPM, or the note plus AFR support if you have a loan. That package satisfies the logic of §§482, 6662, and 1.6662-6 without paying for a full study every year. See the record-keeping for Form 5472 guide for the transaction-by-transaction mapping, then build the return in the step-by-step filer.

Primary sources

- IRC §482 — allocation among controlled parties; commensurate-with-income rule

- IRC §6662 — accuracy-related penalties (transactional and net-adjustment bases)

- IRC §163(j) — business-interest deduction limitation

- Treas. Reg. §§1.482-1, -2, -5, -9 — best-method rule, loans, CPM, and services/SCM

- Treas. Reg. §1.6662-6 — contemporaneous-documentation defense and the principal documents

- Rev. Proc. 2007-13 — specified covered services eligible for the SCM

Related Tools

File Form 5472

Our filer handles Part V transaction reporting automatically.

Transaction Categorizer

Categorize your related-party transactions for Form 5472.

Form 5472 Amendment Guide

Need to correct Part V transactions on a prior filing?

Penalty Calculator

Estimate potential penalties for non-compliance.

Let doola Handle Your Bookkeeping

Proper bookkeeping is the foundation of transfer pricing compliance. doola provides dedicated bookkeeping for foreign-owned LLCs — every transaction categorized and ready for Form 5472 reporting.

Explore doola BookkeepingFile Form 5472 with Part V Done Right

Our guided filer walks you through Part V transaction reporting step by step. Enter your transactions, review the generated form, sign, and submit it yourself.

Start Filing