Form 5472: Why the §1.6038A-2 Attachment Is Mandatory (Don't Skip)

Key Takeaways

- Form 5472 has a separate DE section after Part IV requiring you to check a box AND attach a supplementary description

- Many filers skip this section, thinking Part IV already covered everything — that's a $25,000-penalty mistake

- The regulation (Treasury §1.6038A-2) defines reportable transactions broadly — almost everything qualifies

- Attachment requires: amount, nature of transaction, related party identification, and sufficient factual detail

- Over-disclose rather than under-disclose — IRS reviewers don't know your business; spell out the context

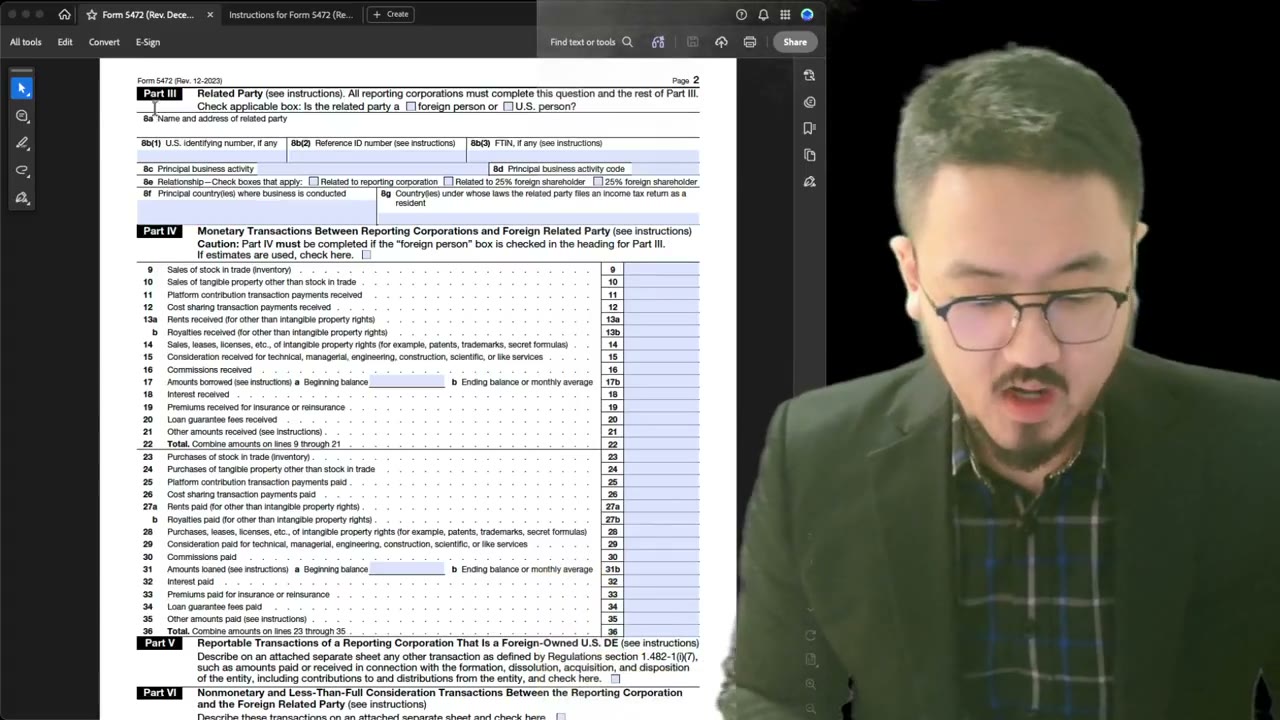

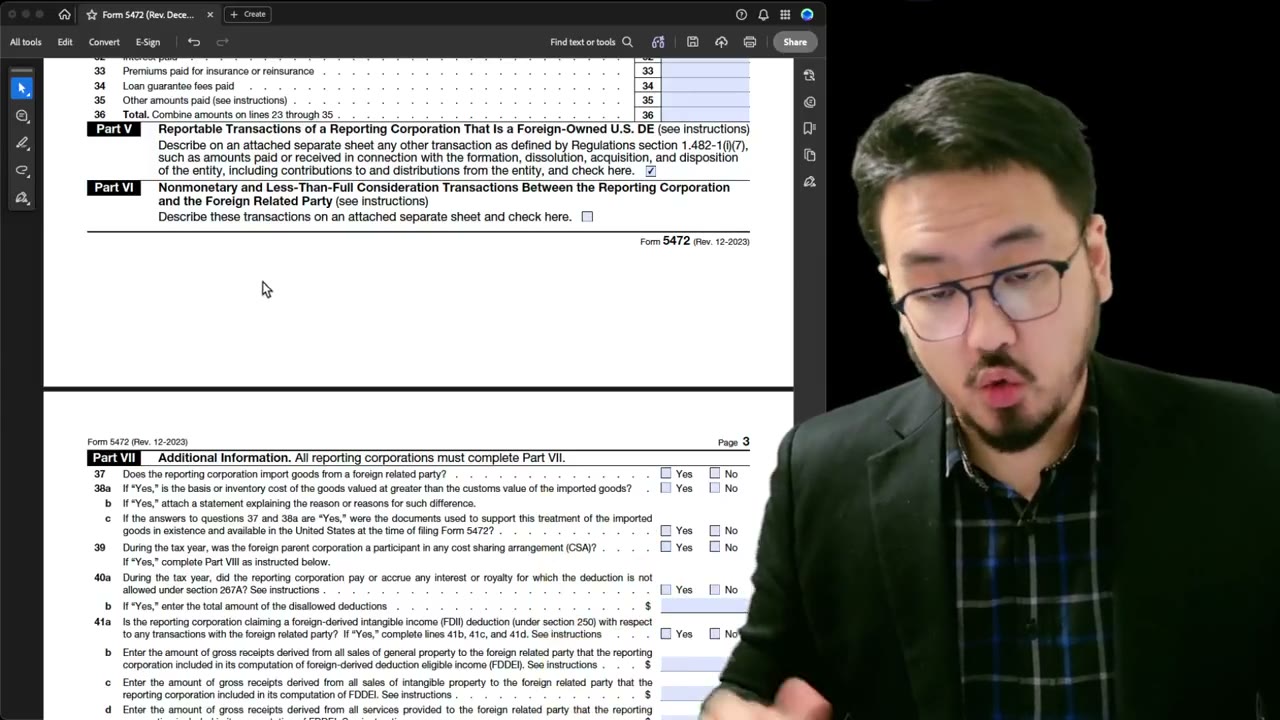

After Part IV: The "Reportable Transactions of a Foreign-Owned U.S. DE" Section

After Part IV (the monetary transactions), Form 5472 has a critically important section that many filers skip: the section asking about "reportable transactions of a reporting corporation that is a foreign-owned U.S. disregarded entity." The wording is awkward, but the function is enormous.

This section is specifically for foreign-owned single-member LLCs (DEs). You must check the box indicating you're filing as a foreign-owned U.S. DE, AND you must then attach a supplementary description of "other transactions" — transactions not captured in Part IV's monetary line items.

Why People Skip It (and Why That's a $25,000 Mistake)

Filers see the section, see that Part IV already captured the monetary transactions, and think "I already reported everything — this section must be for someone else." Wrong.

This section exists BECAUSE the IRS wants foreign-owned DEs to disclose all transactions, including ones that don't fit the structured Part IV line items. Capital contributions, loans, dissolutions, intercompany transfers, accommodations, in-kind transfers — anything not covered by Part IV's narrower categories needs to be described in the attached supplementary statement.

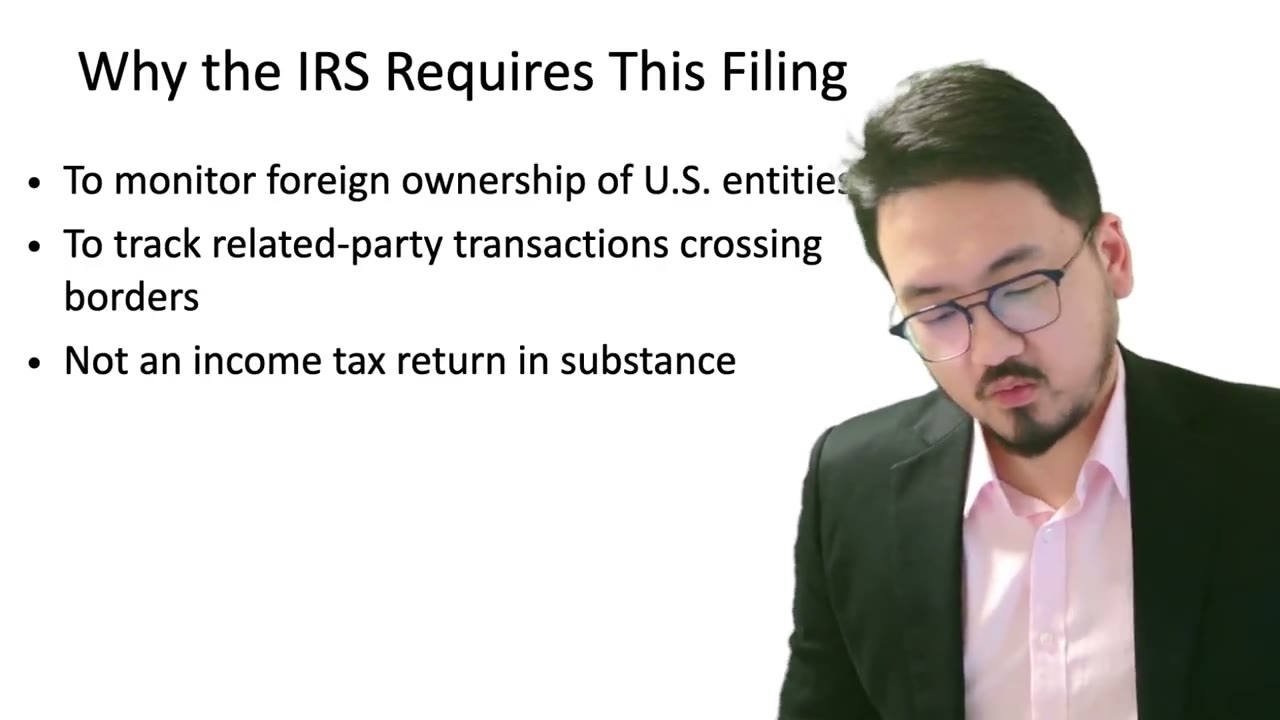

Section 1.6038A-2 — The Broad Definition

The regulation that drives this section (Treasury Regulation §1.6038A-2) defines "reportable transactions" extremely broadly. Any transaction between the reporting corporation and any foreign related party, of any kind, fits within scope.

This is why "my LLC has no transactions" rarely holds up — almost any cross-border money movement, in-kind transfer, accommodation, or service provision counts. The regulation is inclusive by design, precisely to avoid loopholes that would let filers avoid disclosure.

Check the Box, Then Attach a Description

Two steps:

1. Check the box indicating you're filing as a foreign-owned U.S. DE. This is a one-click action on the form.

2. Attach a separate document (no specific IRS template — you create it) describing the other transactions. This attachment is what fulfills the disclosure obligation.

What the Attachment Should Contain (Preview)

The attachment requires four core elements:

- **Amount paid or received** for each transaction - **Nature of the transaction** (capital contribution, dissolution payment, in-kind transfer, etc.) - **Identification of the related party** (yourself, by name) - **Sufficient factual detail** to make sense to an IRS reviewer

The video's recommended approach: think of the attachment as telling the story. Picture the IRS reviewer reading it cold — does it make clear what happened, who paid whom, when, and why? If yes, the disclosure is adequate. If not, add more context.

Don't Outsource Judgment Here If You're Doing It Yourself

If you're filing without a CPA, you're solely responsible for the attachment quality. A weak attachment can trigger "incomplete filing" notices that escalate to the $25,000 penalty.

The video suggests: even amateur filers should add more description than they think necessary. The IRS reviewer doesn't know your business; they need every relevant detail spelled out. Two paragraphs of context beats two sentences of summary every time.

If You're a Professional Filing for Clients

Professionals (CPAs, EAs, tax attorneys) preparing Form 5472 for clients should treat the attachment as core deliverable, not boilerplate. Each client's attachment should reflect their specific transaction set with specific dates, amounts, and descriptions. Templated attachments "customized" by name substitution often miss client-specific details that matter at the IRS level.

Frequently Asked Questions

Is the attachment a specific IRS form?

No — there's no standard template. You create a free-form document (plain text PDF) with the required elements. Title it clearly ("Attachment to Form 5472 — Other Reportable Transactions") so the IRS reviewer knows what it is.

What if I genuinely have NO other transactions beyond what's in Part IV?

Rare. But if true, the attachment can be a brief statement: "No additional reportable transactions occurred during the tax year beyond those reported in Part IV." Sign and date it. This is your declaration that the IRS has the complete picture.

Can the attachment be informal (no specific format)?

Yes — informal is fine. The IRS values clarity over format. A well-organized free-form document with clear headings, dates, amounts, and descriptions is sufficient.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

3:35

3:35Form 5472 Part III: Why You Must Fill Even If You Already Did Part II

Form 5472 Explained — What It Is, Who Must File, and How It Works

Form 5472 Explained: What It Is, Who Must File, and How It Works (2025-2026)

Form 5472 Part IV Monetary Transactions Guide

Form 5472 Part IV Monetary Transactions Guide for Foreign-Owned LLCs (2025-2026)

1:49

1:49When Must Your LLC File Form 5472? Avoid the $25,000 IRS Penalty

2:10

2:10Pro Forma 1120 + Form 5472: Why the IRS Requires This Filing (Information, Not Tax)

3:15

3:15