Foreign-Owned LLC No U.S. Office Address: Form 1120 & 5472 (Part 1)

Key Takeaways

- Three options for foreign-owned LLCs with no U.S. office: foreign address, U.S. C/O address, or U.S. service address

- The C/O address is the most common professional choice — reliable mail handling with full IRS compliance

- Registered agent addresses and P.O. Boxes are explicitly prohibited by Form 1120 instructions

- The address affects IRS correspondence, examiner impressions, state filings, and BOI reports — all should match

- First-time filers default to the wrong answer; Part 2 and Part 3 of this series walk through the decision systematically

The Question Every Foreign-Owned LLC Owner Faces

If you're a foreign founder who owns a U.S. LLC but has no real U.S. office — no employees, no warehouse, no co-working space, no rented apartment — what address goes on Form 1120 and Form 5472 Part I, Line 1a?

This is the single most-asked address question we see from foreign-owned LLC owners. It comes up because the IRS instructions implicitly assume a U.S. address exists, but reality says it often doesn't. Part 1 of our address-strategy series unpacks the question and lays out the three real options.

Why This Matters

The address you put on Form 1120 isn't cosmetic. It affects three downstream things:

1. Where the IRS sends notices, refund checks, and correspondence. A wrong address means missed notices, missed deadlines, and compounding penalties.

2. How an IRS examiner reads your overall fact pattern. The address is one of the first things on the form. A registered agent address (against instructions) looks like an early non-compliance signal. A foreign address signals "genuine foreign-owned, no U.S. presence" — which is exactly what most filers are. A clean C/O notation signals "professionally-prepared filing."

3. Your state filings, any BOI report that is actually required for your entity type, and any treaty positions. All of these reference the same address; consistency matters.

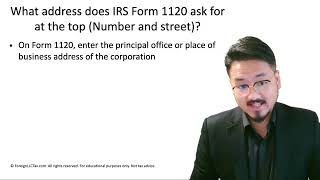

What the IRS Actually Expects

The Form 1120 instructions assume two things: (1) the entity has a principal place of business, and (2) that place is a physical street address (not a P.O. Box, not a virtual mailbox, not a registered agent).

For foreign-owned LLCs with no U.S. presence, the IRS hasn't issued explicit guidance on what to do. Practitioners read between the lines: the principal place of business is wherever the LLC is actually managed — which for a solo foreign founder is their home or office abroad.

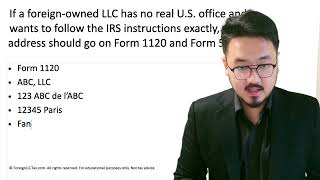

The Three Options

Foreign-owned LLCs with no U.S. office have three workable address options:

1. The foreign principal address. Use your actual home or operating address abroad. Compliant with instructions. Downside: U.S. mail to foreign addresses is unreliable.

2. A U.S. C/O address. Use 'C/O [CPA / Attorney / Mailbox Service], [their U.S. Street Address]'. Reliable mail. Compliant with Form 1120 instructions. Most common choice for serious filers.

3. A U.S. service address with no C/O. Use a U.S. mailbox service or virtual office as the bare address. Technically compliant if the service provides a real street address — but looks suspicious to examiners. Avoid unless you have no other option.

Part 2 walks through when to pick the foreign address vs. a U.S. service address. Part 3 covers the practical recommendation for solo founders.

Why Most First-Time Filers Get This Wrong

First-time filers usually default to one of two wrong answers: (a) the registered agent address (explicitly prohibited), or (b) a P.O. Box (also prohibited unless the post office doesn't deliver to your street address).

The right path requires reading the Form 1120 instructions carefully, understanding the C/O permission, and making a deliberate choice based on your operating reality. None of this is intuitive, which is why most filers end up either using the wrong address or paying a CPA to figure it out. This series walks through the decision systematically.

Frequently Asked Questions

Do I have to have a U.S. address at all?

No. The IRS accepts foreign addresses on Form 1120 and Form 5472 — Part I, Line 1c of Form 5472 specifically has fields for foreign address, foreign postal code, and country. The catch is mail reliability — IRS notices to foreign addresses can be slow or lost.

If I have a Stripe Atlas / doola / Firstbase formation, what address did they give me?

Most formation services use their registered agent's address by default, which is the one address the IRS Form 1120 instructions specifically prohibit. Check the address your formation service set up — if it's the registered agent, you should change it to either your foreign address or a C/O address before filing.

Can I use my home address abroad?

Yes. It's compliant with Form 1120 instructions (the principal place of business is where you actually operate). The Form 5472 Part I, Line 1c has dedicated fields for foreign address. The main downside is mail reliability.

Do I have to keep the same address every year?

No. You can change addresses year-over-year as your situation changes. The IRS uses the address on the most recent return as the canonical one. If you change addresses mid-year, also file Form 8822-B (Change of Address — Business) so notices route correctly.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:00

2:00Foreign LLC No U.S. Office: Foreign Address vs Service Address (Part 2)

1:23

1:23Can the IRS Reissue a CP 575 Letter? What to Do If You Lost It

2:00

2:00Foreign LLC No U.S. Office: Practical Address Recommendations (Part 3)

3:16

3:16Spacing and Punctuation on IRS Forms: Do Periods Commas and Spaces Matter? (Form 1120 and 5472)

4:33

4:33What Address Goes on Form 1120? Principal Office vs Mailing Address Explained

2:00

2:00