Foreign LLC No U.S. Office: Practical Address Recommendations (Part 3)

Key Takeaways

- Default for solo foreign founders: U.S. C/O address through CPA or professional mailbox service

- Mailbox services should be CMRA-registered (real street addresses, not bare P.O. Boxes)

- Use the same address across Form 1120, 5472, SS-4, state filings, BOI, and banking KYC

- File Form 8822-B within 60 days of any address change to keep records aligned

- Document the reasoning for your address choice in tax records for future audit defense

The Default We Recommend for Solo Foreign Founders

If you're a solo foreign founder with a single-member LLC, no employees, no U.S. office, and standard transactions (capital contributions, distributions, occasional service payments), our default recommendation is:

Use a U.S. C/O address through your CPA or a professional mailbox service.

This hits the best balance: full Form 1120 compliance, reliable mail delivery, a stable correspondence address that doesn't change when you move countries, and a clean audit profile. Cost: $20-50/month for a CPA's mail-forwarding service, or $10-25/month for a virtual office / mailbox service.

When You Should Pay for a Proper U.S. Mailbox Service

If you don't have a U.S. CPA (or your CPA charges per-piece for mail forwarding, which can run $5-15 per item), a dedicated mailbox service is the right choice. Look for these features:

- Real street address (not just a P.O. Box). Search for 'commercial mail receiving agency' (CMRA) — they're required by USPS to provide street-format addresses. - Mail scanning. The service scans the envelope (and optionally contents) to a PDF you can view online. Saves on physical forwarding. - Free or low-cost forwarding. Some services bundle 5-10 items/month; others charge per piece. - USPS Form 1583 handling. The service should already be set up to handle this — it's a USPS-required authorization to receive mail on your behalf.

Recommended price range: $10-25/month for basic, $40-80/month for premium scanning.

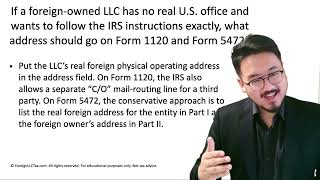

How the Address Ripples Through Other Filings

Whatever address you choose, use it consistently across:

- Form 1120 (pro forma cover sheet for Form 5472) - Form 5472 Part I, Line 1a (reporting corporation address) - Form SS-4 (if you're applying for an EIN) - State annual report (Delaware, Wyoming, etc.) - Any BOI report that is actually required for your entity type - Any state sales tax registration - Stripe / Mercury / Wise / Brex / other banking KYC

Inconsistency across these filings is a yellow flag for IRS examiners and for banks. If your principal address changes mid-year, file Form 8822-B (Change of Address — Business) within 60 days to keep everything aligned.

A 60-Second Decision Flowchart

Here's how to pick in under a minute:

Q1: Do you have a U.S. CPA you work with regularly? - Yes → Use 'C/O [CPA Firm], [Their Address]'. Done. - No → Q2

Q2: Is your home country's postal delivery reliable (Western Europe, developed Asia, Australia, NZ, Canada)? - Yes → Use your foreign home address. Done. - No → Q3

Q3: Do you have a U.S. mailbox service or virtual office? - Yes → Use 'C/O [Service Name], [Service Address]'. Done. - No → Sign up for one ($10-25/month). Then return to Q3.

Whatever you pick, document the reasoning in your tax records. If the IRS ever asks, you'll have a defensible explanation rather than scrambling to reconstruct it from memory.

Frequently Asked Questions

What's the cheapest compliant option?

A foreign home address (free) if you live in a stable country with reliable postal delivery. Second-cheapest: a $10-15/month CMRA-registered mailbox service used as C/O. Avoid 'free' virtual offices that aren't backed by real street addresses.

Should I keep the same address forever?

Ideally yes — consistency reduces friction in audits and reviews. If you must change (CPA switches, mailbox service shuts down, you move countries), file Form 8822-B within 60 days and update Form 5472 / Form 1120 for the next filing.

What if I'm not sure between options?

Default to the U.S. C/O address through a CPA. It's the safest, most defensible option, and the additional cost is modest ($240-600/year) compared to the potential cost of a missed IRS notice or audit complication.

Does any of this affect the OBBBA 2026 1% remittance tax?

No. The enacted 1% tax is limited to certain cash-funded consumer remittance transfers and is independent of your principal address. It does not alter Form 5472 + pro forma Form 1120 address rules; see /guides/remittance-excise-tax for the funding-method scope.

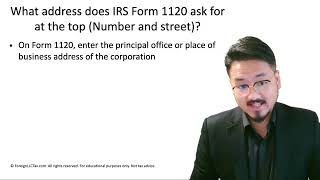

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:00

2:00Foreign LLC No U.S. Office: Foreign Address vs Service Address (Part 2)

2:15

2:15Foreign-Owned LLC No U.S. Office Address: Form 1120 & 5472 (Part 1)

4:33

4:33What Address Goes on Form 1120? Principal Office vs Mailing Address Explained

2:25

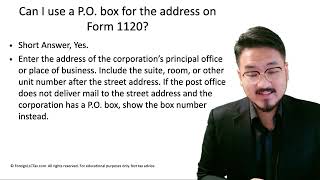

2:25Can You Use a P.O. Box on Form 1120? IRS Address Rules for LLCs

2:00

2:00Can You Use Your Registered Agent's Address on Form 1120? IRS Rules

Pro Forma Form 1120 for Foreign-Owned LLCs: What to Fill and What to Skip