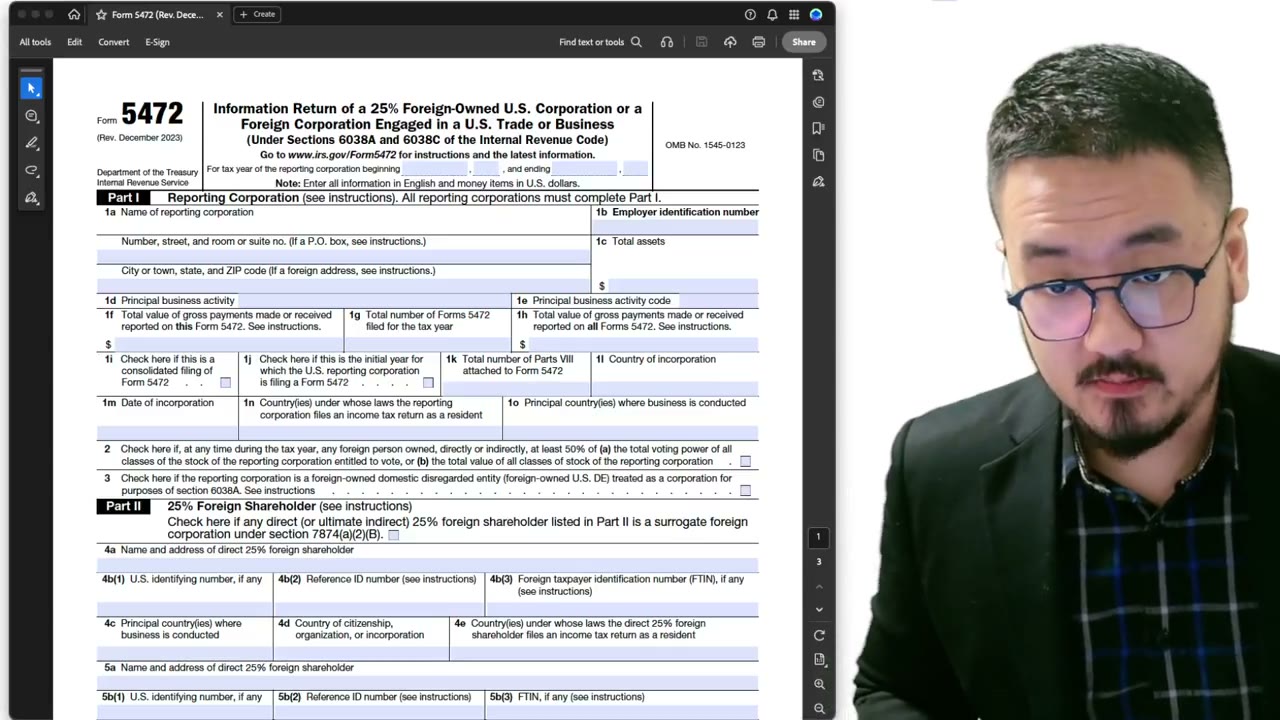

Form 5472 Part II: Name AND Address, Reference ID Numbers, Foreign TIN

Key Takeaways

- Part II requires BOTH name AND address for the 25% foreign shareholder — many filings skip the address

- U.S. identification number is usually "None" for foreigners unless they have an ITIN from prior U.S. filings

- ITIN expires after 3 years of non-use; Form 5472 doesn't count as "using" it — only actual tax returns do

- Reference ID number is yours to invent (e.g., LASTNAME-LLC-YEAR) — must be unique and consistent across all future filings

- Foreign TIN: your home country's tax number; cross-references with treaty-based information exchange

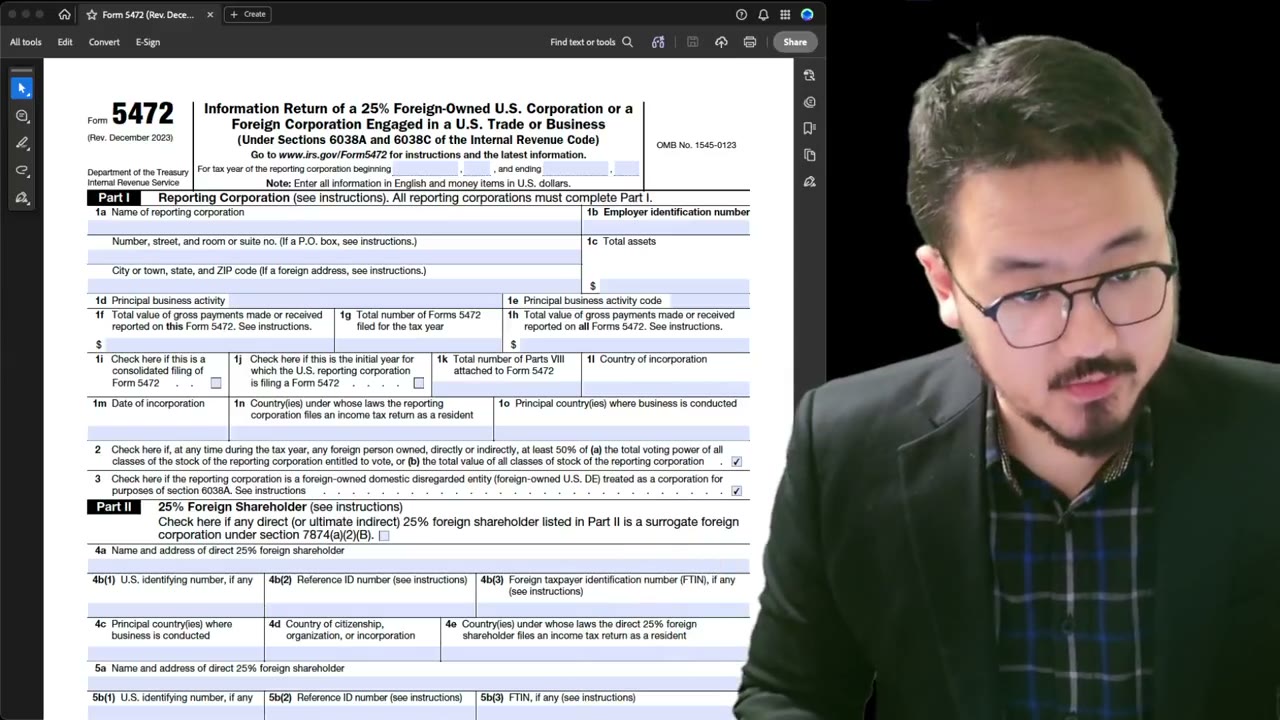

Part II: Identifying the 25% Foreign Shareholder

Form 5472 Part II asks you to identify the 25% foreign shareholder. For a single-member LLC owned 100% by a foreign person, that shareholder is you — the foreign owner. Check the box that says "any direct or ultimate indirect 25% foreign shareholder."

The optional "surrogate form" box only applies if you indirectly hold the LLC through some control mechanism without being the direct holder. For most single-member structures (you personally own the LLC, no intermediary), don't check the surrogate box.

Name AND Address — Don't Skip the Address

The form asks for the shareholder's name AND address. Both required. A surprising number of filings — even from professionals — only fill in the name, leaving the address blank. That's incorrect.

The address ties the shareholder to other identifying information (SSN, ITIN, foreign TIN, reference ID number) through the IRS's cross-reference system. If the address doesn't match what's on other returns (like a personal 1040-NR or another 5472), the inconsistency gets flagged. Fill both, and make them consistent with everything else you've ever filed.

U.S. Identification Number: SSN, ITIN, or None

Field 4b asks for the foreign shareholder's U.S. identification number. The options:

- **SSN** (Social Security Number) — only if the foreign person somehow has one (rare, usually from prior U.S. residency) - **ITIN** (Individual Taxpayer Identification Number) — assigned to foreigners who file U.S. tax returns. If you have one, use it. - **None** — for foreigners with no U.S. tax identification

Most foreign-owned LLC owners don't have an SSN or ITIN unless they've actively filed U.S. personal returns. If you have an ITIN from a prior filing, use it here.

ITIN Notes: Renewal and Activity

ITINs expire if not used on a tax return for 3 consecutive years. Filling in your ITIN here on Form 5472 doesn't count as "using" it for renewal purposes — you have to actually file a U.S. tax return (typically Form 1040-NR) to keep the ITIN active.

If your ITIN expired, the IRS will still accept it on Form 5472 (since it identifies the right person), but you'll need to renew before filing any future U.S. tax return that requires it. The renewal form is W-7 again.

Reference ID Number: Your Own Unique Identifier

If you don't have an SSN or ITIN, the form lets you create a reference ID number. This is a string you make up — must be unique, must be consistent across filings, must not contain special symbols, and shouldn't be too long.

A practical pattern: include your last name and the year, like "WANG2025" or "SMITH-LLC-01." The key is consistency: once you pick a reference ID, use the exact same one on every future Form 5472 filing. The IRS uses it to thread filings together across years. Changing it mid-filing-history creates apparent duplicates and triggers reviews.

Foreign Taxpayer Identification Number (FTIN)

Field 4d asks for the foreign taxpayer identification number — your home country's tax number. For most countries, this is your national ID number or tax registration number. Examples:

- China: 18-digit citizen ID number (with the embedded tax number for individuals) - Singapore: NRIC or FIN number - UK: National Insurance number or UTR - Canada: SIN (Social Insurance Number)

If your country has a separate tax-only number distinct from a national ID, use the tax number. Fill it accurately — the IRS uses this for cross-border information exchange under tax treaties.

Principal Country Where Business Is Conducted (Shareholder's Side)

This field is the SHAREHOLDER's principal country of business — not the LLC's. For an individual foreign owner who runs no separate business, this is typically the same as your residence country (where your day-to-day economic activity happens).

Country of Citizenship

Your country of citizenship — pretty self-explanatory. If you hold multiple citizenships, list the primary one used on your foreign TIN. Be consistent with how you've identified yourself on other U.S. filings or visa records.

Country Where the Shareholder Files Income Tax as a Resident

Here, finally, the wording "as a resident" does mean what it sounds like — your personal tax residency, where you file your personal income tax return. For most foreign owners, this is the country you live in (Singapore, China, Japan, Canada, UK, etc.).

Don't use abbreviations. Write the full country name. Consistency with field 4f (citizenship) is common but not required — you can be a citizen of one country and a tax resident of another (digital nomads, expats, etc.).

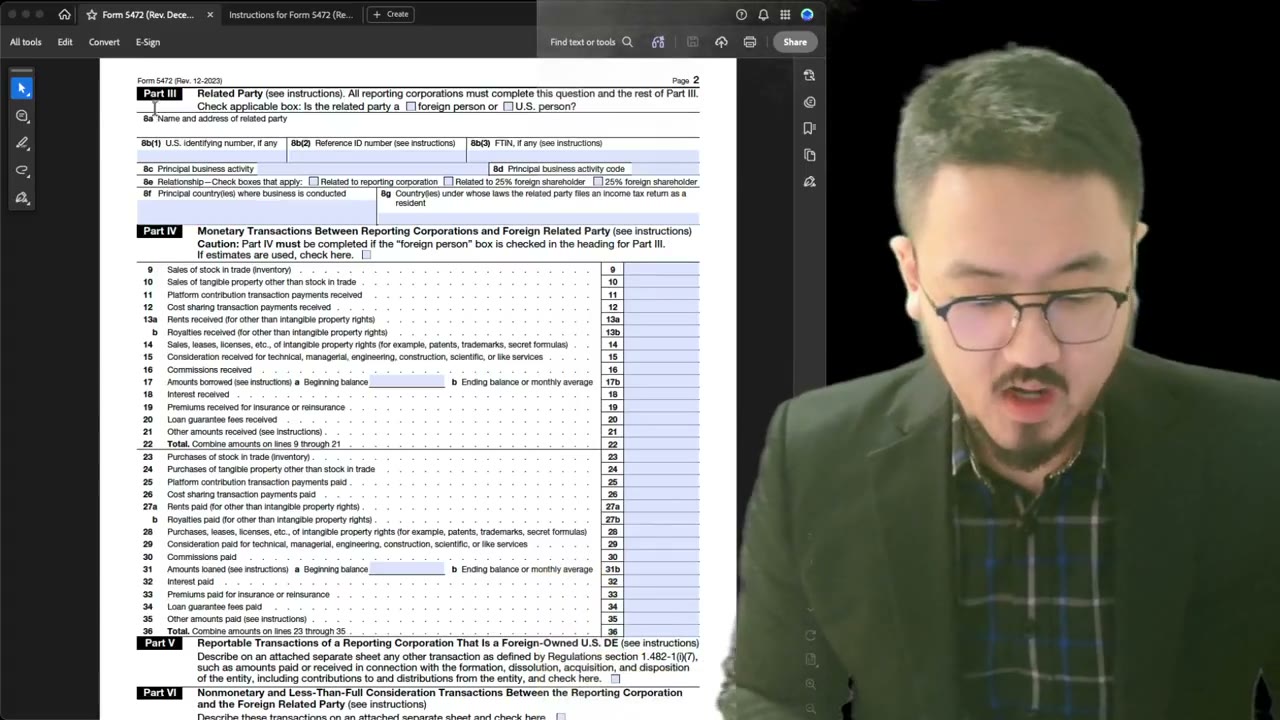

Multiple Shareholders? Repeat the Block

Fields 4a–4i, then 5a–5i, then 6a–6i, then 7a–7i — Form 5472 repeats the same shareholder-info block for up to four 25%+ shareholders. For a single-member LLC (one shareholder = you), only fill the first block. Leave the others blank or write "N/A."

For genuinely multi-shareholder structures, fill one block per 25%+ shareholder. If you have more than four, you can attach supplementary pages with the additional shareholders, formatted identically to the form's blocks.

Frequently Asked Questions

What if I change my reference ID number between filings?

Don't. The IRS uses it to link your filings across years. Changing it creates apparent duplicate filings (the IRS sees two streams that look like different people) and triggers reviews. Pick one and commit.

Can I leave the foreign TIN field blank if I don't want to disclose it?

Technically you can, but the IRS strongly prefers having a TIN for cross-border verification. Blank fields can flag the return for review. If your country doesn't issue a TIN-equivalent (rare), document why; otherwise provide it.

What if I'm a citizen of Country A but tax-resident in Country B?

List Country A in the citizenship field (4f) and Country B in the tax-residency field (4i). The IRS understands this — it's a common pattern for expats and dual-residents. Just make sure your foreign TIN is consistent with whichever country actually issues it.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

4:20

4:20Mailing Form 5472 to the IRS: How to Fill the Courier Sender Info Correctly

8:25

8:25Form 5472 Part I: Why the Reporting Corporation Files Income Tax as a U.S. Resident

3:35

3:35Form 5472 Part III: Why You Must Fill Even If You Already Did Part II

2:10

2:10Form 5472: Why the §1.6038A-2 Attachment Is Mandatory (Don't Skip)

Form 5472 Penalties, Deadlines, and Extensions — What You Need to Know

Form 5472 Penalties ($25,000), Deadlines, and Extension Rules (2025-2026)

Form 5472 Address Rules — Registered Agent vs C/O vs Foreign Address