Form 5472 Item 1n: Why "Files Income Tax As a Resident" Always Means USA

Key Takeaways

- Item 1n asks about the corporation's residency, not yours — for U.S.-formed LLCs, always "United States"

- Write "United States" in full, not "U.S." or "USA" — unambiguous wording is safer than abbreviations

- Item 1o (principal country where business is conducted) is different — that one IS about actual operations

- If Item 1o is the U.S., the IRS expects ECI; if it's foreign, ECI is generally not triggered

- Common mistake: writing your home country in 1n — that misclassifies the corporation's tax-residency

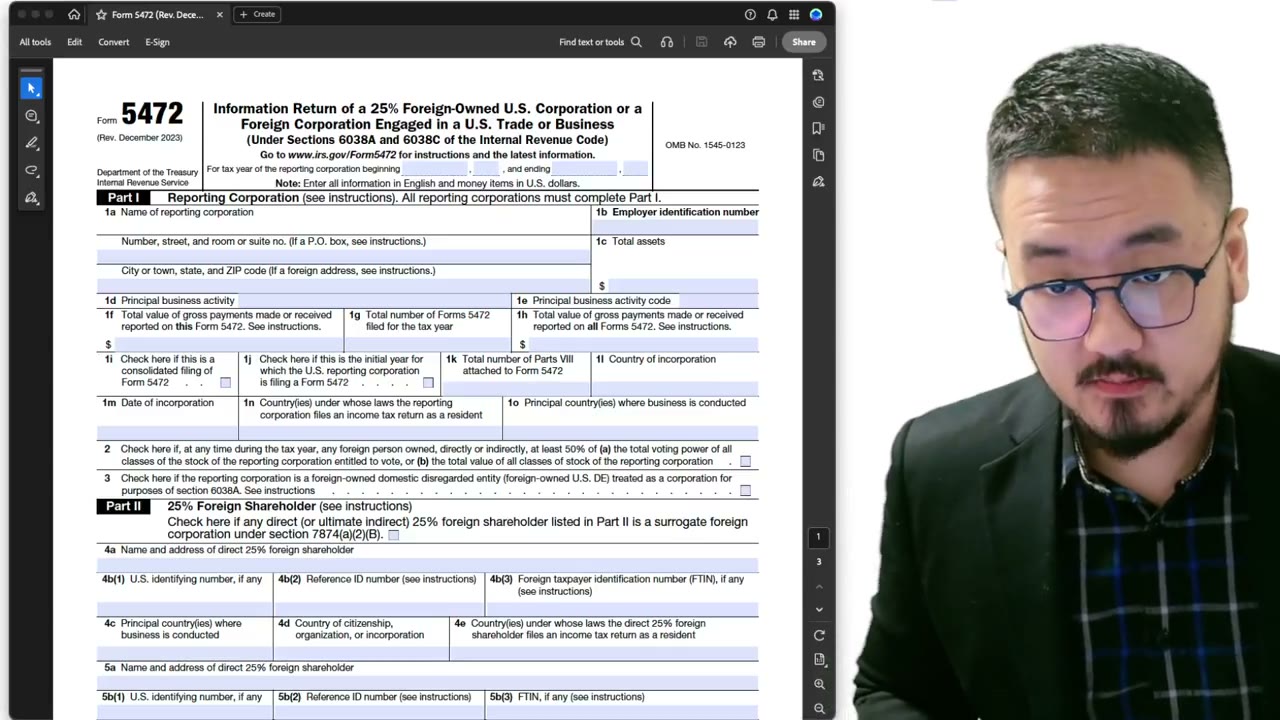

The Confusing Wording in Form 5472 Item 1n

Form 5472 Item 1n asks: "Country under whose laws the reporting corporation files an income tax return as a resident." This phrasing trips up almost every first-time filer.

"As a resident" sounds like it's asking about the owner's residency. It isn't. It's asking about the reporting corporation's residency for tax-filing purposes — and that's the U.S., not the owner's country. The wording is a bit awkward because it carries over from corporate-tax-return contexts where it makes more direct sense.

Why It's the U.S., Not Your Home Country

Your LLC is incorporated in a U.S. state. The pro forma Form 1120 you're attaching this to is a U.S. income tax return. Even though no actual U.S. tax is owed (because the LLC is disregarded for tax purposes), the corporation is filing as a U.S. resident under §6038A.

So when Item 1n asks where the corporation files "as a resident," the answer is the United States. Your personal residency (Singapore, China, Japan, wherever) doesn't change this. The corporation has a residence; the owner has a residence; they're separate and the form is asking about the corporation's.

Use "United States" — Not "U.S." or "USA"

Recommended phrasing: write out "United States" in full. Avoid abbreviations like "U.S." or "USA." The IRS forms processing software prefers consistent, unabbreviated country names — and abbreviations occasionally trip OCR systems.

"USA" is technically the United States of America and is interpreted correctly most of the time. But "United States" is unambiguous and matches the format the IRS uses internally. Pick safety over brevity here.

Principal Country Where Business Is Conducted (Different Field)

Item 1o (different field, often confused with 1n) asks for the principal country where business is conducted. THIS field is about actual operations, not legal residency.

If your LLC operates entirely from Singapore — your team is there, your clients are there, your revenue comes from there — then Item 1o is Singapore. The two fields legitimately have different answers: 1n = United States (legal residency), 1o = Singapore (where operations happen).

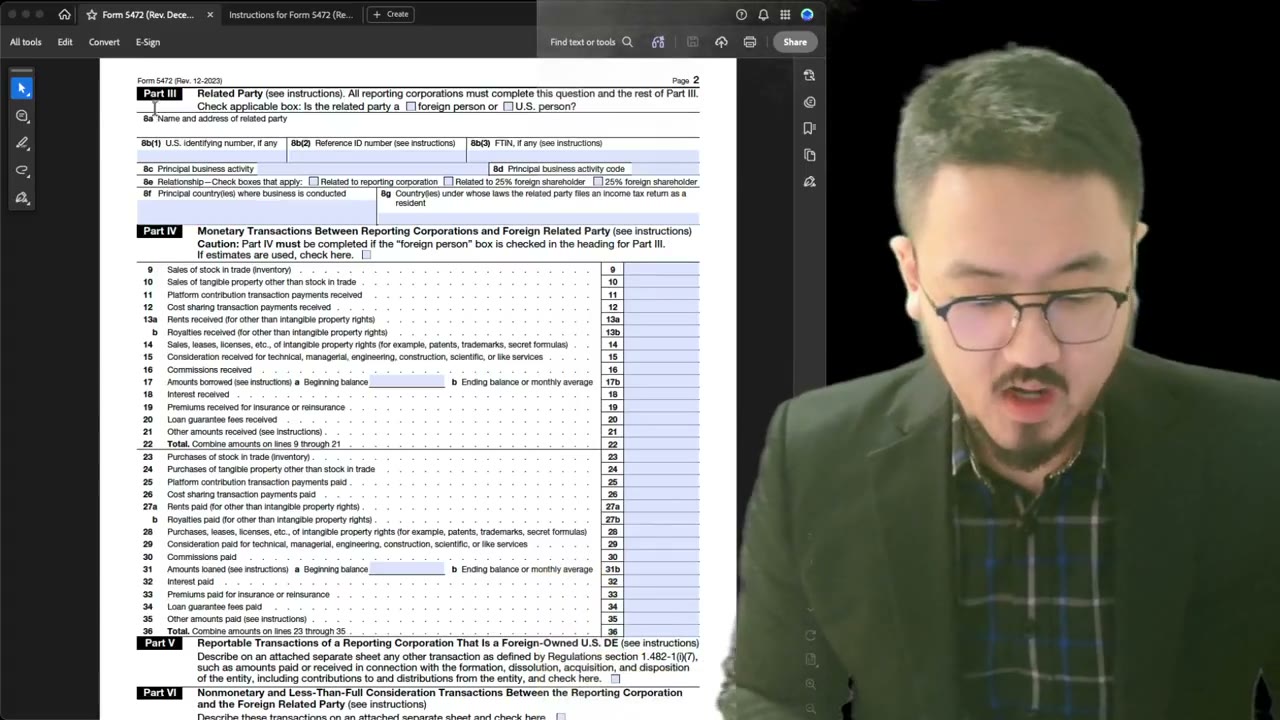

Why the Distinction Matters: ECI

If Item 1o (principal country of business) is the U.S., the IRS reads this as a signal that the LLC has Effectively Connected Income (ECI) to a U.S. trade or business. ECI triggers actual U.S. income tax obligations — potentially Form 1120-F territory, not just pro forma 1120.

If Item 1o is a foreign country, the IRS reads it as: no U.S. trade or business → no ECI → no U.S. income tax owed. This is the desirable outcome for most foreign owners, but only if it's true. Don't lie here. If your business genuinely operates in the U.S. (you have a U.S. office, U.S. employees, U.S. clients you actively serve), the answer is the U.S. and you need to deal with the ECI implications, possibly with a different filing structure.

The Wording Trap to Avoid

If you read Item 1n quickly and write "Singapore" (or wherever you live), the IRS gets a Form 5472 claiming the corporation files income tax as a resident of Singapore — which is nonsensical for a U.S.-incorporated LLC, and triggers a processing flag.

Slow down on this field. Read both 1n and 1o together. Recognize that 1n is asking about the corporation's residency (always USA for U.S.-formed LLCs), and 1o is asking about the actual operating country (often a foreign country for offshore-operated LLCs). The pair tells the IRS the full picture.

Frequently Asked Questions

What if my LLC genuinely has dual residency for some reason?

Extremely rare for single-member LLCs. If you genuinely have a tax treaty resident-tie-breaker situation, consult a CPA — the standard Form 5472 doesn't capture multi-jurisdictional residency well, and you may need supplementary disclosures.

Is there a difference between 'United States' and 'United States of America' on the form?

Both are accepted by the IRS processing system. "United States" is shorter and equally unambiguous, which is why it's the standard.

Can I put 'N/A' for Item 1o if my LLC is dormant?

Avoid N/A — IRS forms processing often flags blank-looking responses. Use the country where the owner resides as a reasonable default for a dormant LLC, since that's where the (minimal) business decisions happen.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

8:25

8:25Form 5472 Part I: Why the Reporting Corporation Files Income Tax as a U.S. Resident

3:35

3:35Form 5472 Part III: Why You Must Fill Even If You Already Did Part II

Form 5472 Explained — What It Is, Who Must File, and How It Works

Form 5472 Explained: What It Is, Who Must File, and How It Works (2025-2026)

2:10

2:10Pro Forma 1120 + Form 5472: Why the IRS Requires This Filing (Information, Not Tax)

2:20

2:20Pro Forma 1120 + Form 5472: What Counts as a Reportable Transaction with Your LLC

2:05

2:05