Form 8857: When You May Qualify for Innocent Spouse Relief (Part 1)

Key Takeaways

- You must not have known about your spouse's unreported income or false deductions

- Simply disagreeing with a tax bill does not qualify — specific criteria must be met

- The IRS considers your education, involvement in finances, and whether you benefited

- Common scenario: spouse runs a business and hides income without your knowledge

- File Form 8857 as soon as you become aware of the issue

Qualification Requirements

Not every disagreement with a tax bill qualifies for innocent spouse relief. The IRS has specific criteria that must be met. The primary requirement is that there was an understatement of tax due to your spouse's unreported income or false deductions — and you did not know about it.

The key word is 'innocent' — you genuinely had no knowledge of the errors. If you knew your spouse was hiding income or inflating deductions and signed the joint return anyway, you generally will not qualify.

Common Qualifying Scenarios

Consider this scenario: a married couple files jointly. One spouse, Alex, runs a small business and makes $30,000 in unreported sales. The other spouse trusts Alex to handle all tax matters and signs the joint return without knowing about the hidden income. Two years later, the IRS audits the return and assesses additional tax plus penalties.

In this case, the unknowing spouse can apply for innocent spouse relief because: there was an understatement of tax (unreported income), the spouse did not know about it, and it would be unfair to hold the innocent spouse liable.

Factors the IRS Considers

The IRS examines several factors when evaluating innocent spouse claims: your education and business experience, the extent of your involvement in the family finances, whether you significantly benefited from the understatement, and whether you had reason to know about the errors. The IRS also considers whether you have been deserted by or are separated from your spouse.

Frequently Asked Questions

What if I suspected something was wrong but signed the return anyway?

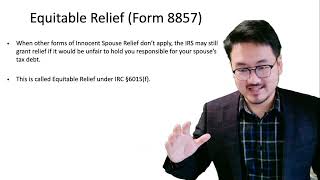

If you had reason to know about the understatement, your claim may be denied under the classic innocent spouse rules. However, you might still qualify for equitable relief under IRC §6015(f) if it would be inequitable to hold you liable given all facts and circumstances.

Does filing for innocent spouse relief affect my current spouse?

If you are still married, the IRS will notify your spouse of the request and allow them to respond. This can create tension, but the filing is necessary to protect your rights.

IRS Form 8857 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 8857 Innocent Spouse Relief

5:44

5:44Form 8857: When You May Qualify for Innocent Spouse Relief (Part 2)

7:32

7:32Form 8857: IRC Section 6015(f) Equitable Relief Explained (Part 2)

7:32

7:32IRC 6015(f) Equitable Relief for Innocent Spouse (Part 2)

6:18

6:18Form 8857: IRC Section 6015(f) Equitable Relief Explained (Part 1)

3:28

3:28Form 8857 Introduction: What Is Innocent Spouse Relief?

Form 8857 Innocent Spouse Basics Guide