Form 8857: IRC Section 6015(f) Equitable Relief Explained (Part 2)

Key Takeaways

- Equitable relief is the most flexible innocent spouse provision — no single factor decides

- Divorce or separation strengthens your case; still living together weakens it

- Economic hardship is a powerful factor — document your financial situation

- Be thorough and truthful — omitting unfavorable facts will backfire

- Knowledge or reason to know about errors is the most critical factor

Equitable Relief: How the IRS Decides Fairness

Under IRC §6015(f) equitable relief, the IRS weighs multiple factors to determine if it would be unfair to hold you liable. No single factor guarantees approval — the IRS evaluates the overall situation. Your marital status matters: being divorced or separated strengthens your case, while still living together with your spouse weakens it.

Key Factors the IRS Considers

The IRS examines whether you knew or had reason to know about the understatement, whether you received significant benefit from it, whether your spouse abused you or maintained financial control, your mental or physical health status, and whether you made a good-faith effort to comply with tax laws in subsequent years.

Economic hardship is also a major factor — if paying the liability would prevent you from meeting basic living expenses, the IRS is more likely to grant equitable relief. Documentation of your financial situation strengthens this argument.

Making Your Best Case

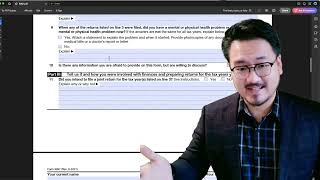

When applying for equitable relief, be thorough and truthful. Include all supporting documentation: divorce decrees, financial records showing limited access to family finances, evidence of abuse or control, medical records if applicable, and documentation of current financial hardship. Do not omit facts that hurt your case — the IRS will discover them, and dishonesty undermines your entire request.

Frequently Asked Questions

Can I get equitable relief if I knew about some issues?

Possibly. The IRS weighs the totality of circumstances. Even if you had some knowledge, factors like abuse, economic hardship, or your spouse's financial control may still support granting relief.

How long does the equitable relief process take?

The process typically takes 6-12 months, though complex cases can take longer. The IRS may request additional documentation during the review.

IRS Form 8857 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 8857 Innocent Spouse Relief

6:18

6:18Form 8857: IRC Section 6015(f) Equitable Relief Explained (Part 1)

7:32

7:32IRC 6015(f) Equitable Relief for Innocent Spouse (Part 2)

5:44

5:44Form 8857: When You May Qualify for Innocent Spouse Relief (Part 2)

4:56

4:56Form 8857: When You May Qualify for Innocent Spouse Relief (Part 1)

3:28

3:28Form 8857 Introduction: What Is Innocent Spouse Relief?

Form 8857 Equitable Relief Factors Guide