Form 8857: IRC Section 6015(f) Equitable Relief Explained (Part 1)

Key Takeaways

- Equitable relief is the fallback when classic relief and separation of liability don't apply

- Can address both understatements (wrong return) AND underpayments (unpaid correct return)

- No fixed time deadline — but file promptly for best results

- The IRS evaluates the overall fairness of holding you liable

- Designed to handle real-world complexity that stricter rules don't cover

What Is Equitable Relief (IRC §6015(f))?

Equitable relief is the safety net of innocent spouse provisions. If you do not qualify for classic innocent spouse relief or separation of liability, equitable relief provides a third option when it would simply be unfair to hold you responsible for your spouse's tax errors.

The IRS designed this provision to address real-world complexity — life is not black and white, and the tax code should not force innocent people to pay for their spouse's mistakes just because they do not fit neatly into the stricter relief categories.

When Equitable Relief Applies

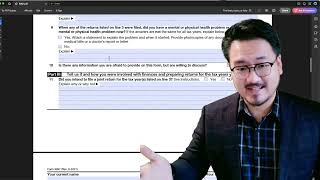

Equitable relief applies in two situations: when there is an understatement of tax (your spouse reported less tax than owed) or an underpayment of tax (the return was correct but the tax was not paid). Unlike classic innocent spouse relief, equitable relief can address underpayment situations — making it the only relief option when the return was accurate but your spouse failed to pay.

There is no fixed time limit for equitable relief requests, unlike the 2-year deadline for classic relief and separation of liability. However, filing promptly is always advisable.

Frequently Asked Questions

What is the difference between understatement and underpayment?

Understatement means the return was incorrect (unreported income or false deductions). Underpayment means the return was correct but the tax shown on the return was not fully paid. Classic innocent spouse relief only addresses understatements; equitable relief can address both.

Do I need a lawyer for equitable relief?

While not required, a tax professional or attorney can significantly strengthen your case. They can help identify relevant factors, gather documentation, and present your case effectively to the IRS.

IRS Form 8857 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 8857 Innocent Spouse Relief

7:32

7:32Form 8857: IRC Section 6015(f) Equitable Relief Explained (Part 2)

7:32

7:32IRC 6015(f) Equitable Relief for Innocent Spouse (Part 2)

5:44

5:44Form 8857: When You May Qualify for Innocent Spouse Relief (Part 2)

4:56

4:56Form 8857: When You May Qualify for Innocent Spouse Relief (Part 1)

3:28

3:28Form 8857 Introduction: What Is Innocent Spouse Relief?

Form 8857 Equitable Relief Factors Guide