IRS Publication 538: Worked Examples for Calendar Year, Fiscal Year, Short Tax Year

Key Takeaways

- Publication 538 defines tax years: calendar (default), fiscal, or short (less than 12 months)

- Tax year is adopted by filing the first income tax return — extensions and EIN don't establish it

- Short tax year happens when entity wasn't in existence for the entire year (formation or dissolution)

- Publication 538's example: formed July 1 → first tax year is July 1 – December 31

- Mirror example: dissolved July 23 → final tax year is January 1 – July 23 (same year)

Diving Into Publication 538: The Accounting Period Definitions

Publication 538 is structured around two big themes: accounting periods (which tax year you use) and accounting methods (cash vs. accrual). For foreign-owned LLC owners filing the pro forma 1120 + Form 5472, the accounting period chapters are the relevant ones.

Key definitions from the publication:

- **Calendar year**: 12 consecutive months beginning January 1 and ending December 31 - **Fiscal year**: 12 consecutive months ending on the last day of any month except December (or a 52–53 week tax year) - **Short tax year**: any tax year of less than 12 months

How You Adopt a Tax Year

You adopt a tax year by filing your first income tax return using that tax year. Filing an application for extension, employer ID number paperwork, or estimated tax doesn't establish a tax year. The first actual income tax return is the establishing act.

For a foreign-owned single-member LLC, this means: your first pro forma Form 1120 + Form 5472 effectively establishes your tax year. Whatever beginning and ending dates you enter on that first filing become your LLC's adopted tax year going forward.

Calendar Year Is the Default

For most people, the calendar year is the natural default — January 1 to December 31. Publication 538 confirms this is the standard 12-month tax year, the one most U.S. individuals and many entities use without thinking about it.

Foreign-owned LLCs almost always use the calendar year unless there's a specific reason to use a fiscal year (uncommon for single-member LLCs). The owner's home country tax year may or may not align with the U.S. calendar year, but the LLC's tax year is a separate decision from the owner's personal tax year.

Short Tax Year Trigger: Not Existing for the Entire Year

Publication 538 explicitly addresses the short tax year trigger: "A short period tax return may be required when you (as a taxable entity) are not in existence for the entire year, or you change your accounting period."

So if your entity didn't exist for the entire year (you formed it mid-year, or dissolved it mid-year), a short period tax return is required. The general rule: even when an entity wasn't in existence for the entire year, a return is still required for the time it WAS in existence. Filing requirements and tax computations are generally the same as for a full tax year ending on the last day of the short period.

Worked Example from Publication 538

Publication 538 provides a classic worked example:

"XYZ Corporation was organized on July 1 and elected a calendar year as its tax year. The corporation's first return will cover the short period from July 1 through December 31."

That's the formation scenario. The mirror example for dissolution:

"A calendar year corporation that dissolved during the year — the final return will cover the short period from January 1 through the date of dissolution (e.g., July 23)."

Both examples follow the same rule: enter the actual beginning and ending dates of the entity's existence during the tax year. The IRS has no special form for short tax years — you use the same Form 1120, just with shorter date ranges in the tax-year fields.

Why Foreign Owners Should Know This

For foreign owners forming their first U.S. LLC, the short tax year for the formation year is almost universal — entities are rarely formed exactly on January 1. So your very first pro forma 1120 + Form 5472 filing will likely be a short tax year filing.

Publication 538's worked example is the direct template: enter the formation date as the beginning, December 31 as the ending, check the "initial return" box, file by the next April 15 (or June 15 with foreign extension). Done.

Frequently Asked Questions

If I form the LLC on December 30, do I file for those two days?

Yes — even two days of existence requires the filing for that short tax year. You'd enter the dates December 30 – December 31, check initial return, and file by the next April 15. The filing is mostly zeros for such a short period, but the obligation exists.

Can I avoid a short first year by waiting to apply for an EIN?

The tax year is established when you file your first return, not when you get the EIN. So delaying the EIN doesn't change the LLC's existence date for tax purposes. The LLC's first tax year starts on its state formation date regardless of EIN timing.

Does the short tax year impact when I file?

No — same deadlines as full tax years. The filing for a short tax year ending December 31, 2025, is due April 15, 2026 (June 15 with the foreign extension), the same as a full 12-month year ending December 31, 2025.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Tax Basics & Filing Requirements

2:25

2:25Short Tax Year: When It Happens and Why It Still Counts as a Full Tax Year

1:34

1:34IRS Publication 538: Accounting Periods, Methods, and Short Tax Years Reference

3:15

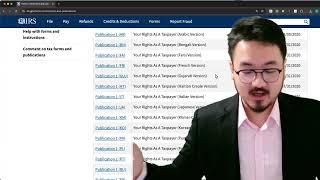

3:15How to Find and Download IRS Forms, Publications, and Instructions

7:17

7:17Standard vs Itemized Deduction: Important Catches Part 1

5:43

5:43Standard vs Itemized Deduction: Important Catches Part 2

When Schedule C Applies to a Foreign-Owned LLC Owner