IRS Publication 538: Accounting Periods, Methods, and Short Tax Years Reference

Key Takeaways

- Publication 538 is the IRS reference for accounting periods, methods, short tax years, and fiscal year elections

- Always use the latest revision — check the cover date and the Future Developments page on IRS.gov

- For foreign-owned LLCs, chapters 1-3 cover almost everything you'll encounter; the rest is for complex scenarios

- It's authoritative as a plain-language summary, but the actual legal source is the Internal Revenue Code (Title 26)

- Most short tax year and accounting method questions on Form 1120 can be answered by Publication 538 chapter 1 or 2

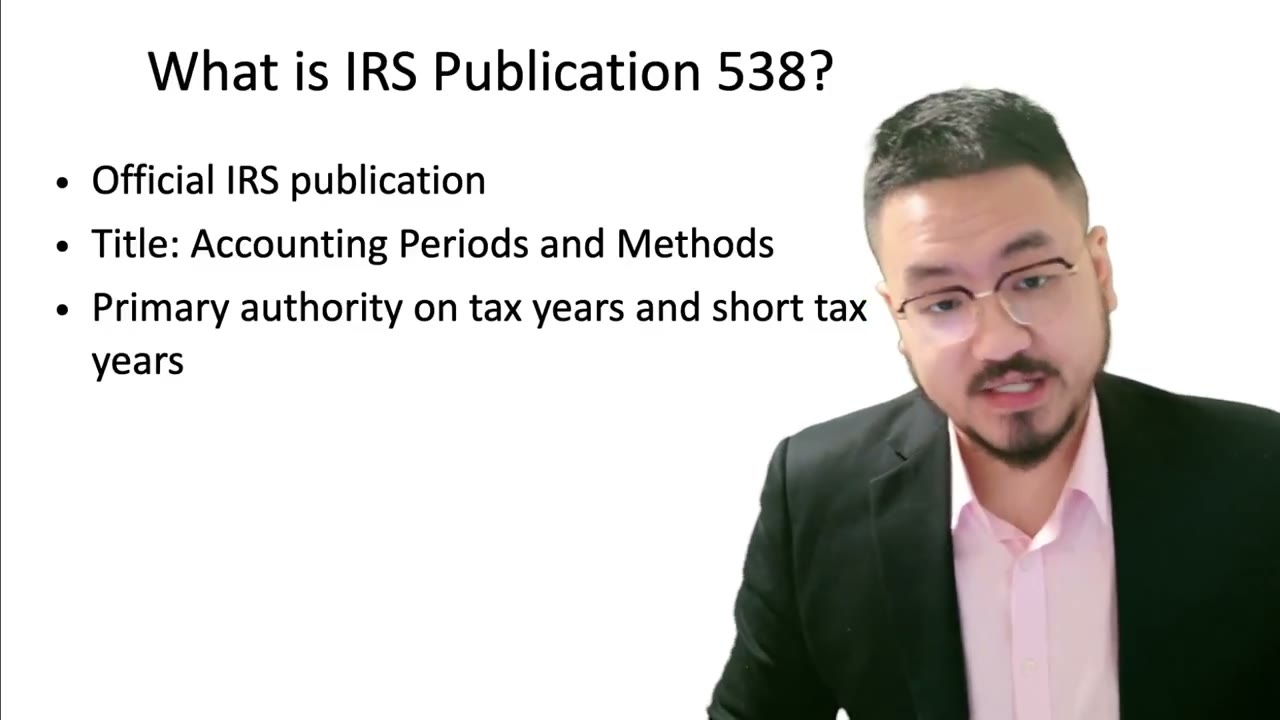

What IRS Publication 538 Actually Is

IRS Publication 538 ("Accounting Periods and Methods") is the foundational reference document for understanding how the IRS treats tax years — calendar years, fiscal years, short tax years, accounting periods, accounting methods (cash vs. accrual), and changes between any of those. If you've ever stared at a Form 1120 field asking for your "tax year" and wondered whether the IRS has specific rules for what counts as one, Publication 538 is where the answer lives.

For foreign-owned LLC owners filing the pro forma Form 1120 + Form 5472 combination, Publication 538 is the source document for short tax year rules (relevant the year the LLC was formed and the year it dissolves), accounting period changes (if you ever change your year-end), and basic accounting method elections (if you're filing the first time and need to declare cash vs. accrual).

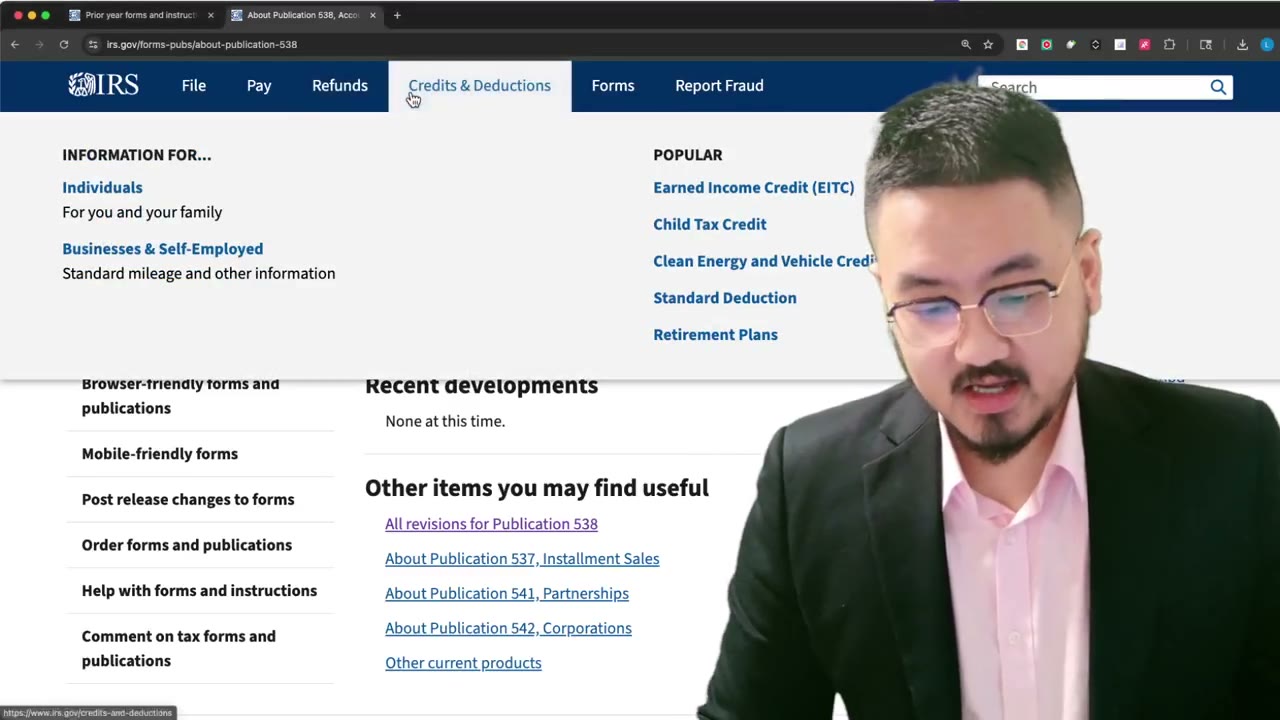

How to Find the Current Version

Always use the latest revision. IRS publications are updated periodically as the tax code changes, and an outdated version can give you the wrong answer on rules that have shifted. Find Publication 538 on IRS.gov by searching "Publication 538" — the official URL is irs.gov/forms-pubs/about-publication-538. The landing page shows the current revision date and links to the PDF.

Before relying on a version, check two things. First, the revision date on the cover (look for "Rev. Month-Year"). Second, the "Future Developments" page at the start of the publication — that section flags any pending changes the IRS expects to publish in the next revision. If you see notes about upcoming changes that affect your scenario, you may need to wait for the next revision or consult a CPA.

When You'll Actually Reference Publication 538

Most foreign LLC owners don't need to read Publication 538 cover-to-cover. The chapters that matter are typically:

- Chapter 1 (Accounting Periods): defines what a tax year is, when you can use a fiscal year instead of a calendar year, and what counts as a short tax year. This is the chapter you want when filling in Form 1120's tax year fields.

- Chapter 2 (Short Tax Year): covers when a short tax year arises (first year of operation, last year before dissolution, year of accounting period change), how to compute it, and how it affects deduction limits and depreciation.

- Chapter 3 (Accounting Methods): cash vs. accrual, when you can elect each, and the rules for switching. Most single-member foreign-owned LLCs use the cash method.

The rest of the publication covers more complex scenarios — inventory accounting, long-term contracts, installment sales — that rarely apply to passive foreign-owned LLCs filing the pro forma 1120 + Form 5472.

Why It's the Reference, Not the Source of Truth

Publication 538 is an IRS plain-language summary. It's authoritative for understanding the rules, but the actual legal source is the Internal Revenue Code (Title 26 of the U.S. Code) and the Treasury Regulations. If you're in a complex situation — a CPA disagrees with the publication, or you're considering a structure that doesn't fit a standard example — the IRC and regulations are the controlling authority.

For 99% of foreign-owned LLC scenarios, Publication 538 is sufficient. The structures are well-trodden ground and the publication's examples cover the common cases. Save the IRC dive for genuinely unusual situations like accounting-method elections, mid-year ownership changes, or atypical fiscal years.

Frequently Asked Questions

Where do I find Publication 538?

On the IRS website at irs.gov/forms-pubs/about-publication-538. The landing page shows the current revision and links to the official PDF.

Does Publication 538 cover foreign-owned LLCs specifically?

No — it covers accounting periods and methods in general, applicable to any U.S. entity. Foreign-owned LLCs use the same rules as domestic LLCs for these questions; the foreign ownership doesn't change which tax year or accounting method is available.

Which chapter is most relevant for the pro forma 1120 + Form 5472 filing?

Chapter 1 (Accounting Periods) for the tax-year fields, and chapter 2 (Short Tax Year) if your LLC was formed mid-year. Together they answer almost every Form 1120 tax-year question that comes up in this filing.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Tax Basics & Filing Requirements

3:15

3:15IRS Publication 538: Worked Examples for Calendar Year, Fiscal Year, Short Tax Year

3:15

3:15How to Find and Download IRS Forms, Publications, and Instructions

8:07

8:07Essential IRS Forms and Due Dates Quick Reference Guide

2:25

2:25Short Tax Year: When It Happens and Why It Still Counts as a Full Tax Year

When Schedule C Applies to a Foreign-Owned LLC Owner

When Schedule C Applies to a Foreign-Owned LLC Owner (2025-2026)

ITIN Supporting Documents Guide