Short Tax Year: When It Happens and Why It Still Counts as a Full Tax Year

Key Takeaways

- Short tax year = any tax period less than 12 months (typically formation year or dissolution year)

- Even a 1-month short tax year is still a tax year with full filing obligations

- Foreign-owned LLCs formed mid-year file Form 5472 for that short year, on the standard deadline

- IRS Publication 538 is the authoritative reference for accounting periods, short tax years, and methods

- Always check IRS.gov for the latest Publication 538 revision — tax rules evolve

What Is a Short Tax Year?

A short tax year is any tax year that covers less than 12 months. The IRS defines it strictly: if your return covers a period shorter than a full calendar year, it's a short tax year under their rules.

This matters because most U.S. tax filings assume a 12-month tax year (calendar or fiscal). When your filing covers a shorter period — typically the first year after entity formation or the last year before dissolution — special rules apply for date entry, deduction limits, and depreciation.

When a Short Tax Year Occurs

Three common scenarios trigger a short tax year:

- **First year of operation**: an entity that's formed mid-year has a short first tax year from the formation date through year-end. Example: LLC formed July 1, 2025, on a calendar tax year → first tax year is July 1 – December 31, 2025.

- **Final year of operation**: an entity dissolved mid-year has a short final tax year from January 1 through the dissolution date. Example: LLC dissolved July 23, 2026, on a calendar tax year → final tax year is January 1 – July 23, 2026.

- **Accounting period change**: if you change your tax year (uncommon for LLCs, but possible), the transition year may be short to bridge between old and new year-ends.

Short Tax Years Still Count as Tax Years

Even though a short tax year is less than 12 months, it's still a tax year — and triggers all the standard filing obligations. A foreign-owned LLC formed mid-year still files Form 5472 for that short tax year, even though it covers only a few months.

This trips up new owners who think "I only operated for 3 months, so I don't need to file until next year." Wrong. The 3-month short tax year is its own filing period with its own deadlines (typically the standard April 15 / June 15 for the year after the short tax year ends).

Why Publication 538 Is the Reference

IRS Publication 538 ("Accounting Periods and Methods") is the authoritative reference for short tax year rules. The publication explains:

- The definition (less than 12 months) - When short tax years arise (formation, dissolution, accounting period change) - How to compute the short period - Special treatment for deduction limits (often pro-rated for short years) - How depreciation is affected

It's a plain-language summary of the underlying Internal Revenue Code rules — easier to read than the IRC itself but still authoritative.

Where Foreign LLC Owners See This

For foreign-owned single-member LLC owners, the short tax year question comes up when filling Form 1120's tax-year fields. The form has a section asking for the beginning and ending dates of the tax year — and a checkbox to indicate "initial return" or "final return."

If this is your LLC's first year (initial return), check that box and enter the dates from formation through year-end. If it's the dissolution year (final return), check that box and enter dates from January 1 through the dissolution date. The structure is the same whether your tax year is 12 months or short.

Tax Professionals Update Knowledge Constantly

The video author also notes — as a side comment — that tax professionals have a continuing education requirement precisely because IRS rules evolve. Publications get revised, tax law amendments shift treatment of specific scenarios, and what was correct last year may be partially outdated this year. The IRS publishes updated versions of Publication 538 periodically; always check the IRS.gov page for the current revision before relying on a quoted rule.

Frequently Asked Questions

If my LLC was formed July 1 and dissolved December 15 the same year, is that a short tax year?

Yes — and it's both an initial and a final return in the same period. The tax year is July 1 – December 15. Check both the initial return and final return boxes on Form 1120 and explain in a cover statement.

Do I file twice if I have a short first tax year followed by a normal full year?

Yes — one Form 5472 (and pro forma 1120) for each year. The short first year gets one filing; the next full year gets another. Each is its own complete filing.

Does a short tax year reduce my filing obligations or penalties?

No. Short tax year just changes the dates on the filing. The $25,000 failure-to-file penalty applies the same way as for a full tax year. The pro-rating only applies to certain deductions and depreciation, not to penalties.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Tax Basics & Filing Requirements

3:15

3:15IRS Publication 538: Worked Examples for Calendar Year, Fiscal Year, Short Tax Year

7:17

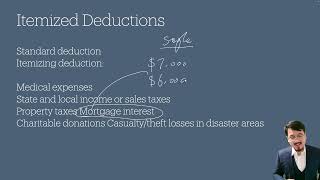

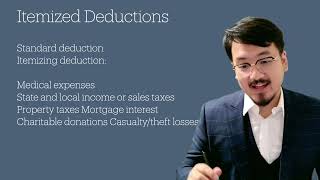

7:17Standard vs Itemized Deduction: Important Catches Part 1

5:43

5:43Standard vs Itemized Deduction: Important Catches Part 2

6:42

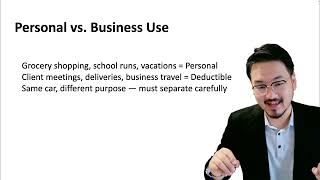

6:42Startup with One Car: Business and Personal Use Tax Rules

1:34

1:34IRS Publication 538: Accounting Periods, Methods, and Short Tax Years Reference

When Schedule C Applies to a Foreign-Owned LLC Owner