Pro Forma Form 1120 for Foreign-Owned LLCs: What to Fill and What to Skip

Corporate return flow (Form 1120)

How a C corporation reports income and computes its tax.

Determine corporate status

Default for corporations, or via a Form 8832 election.

Prepare Form 1120

Report income, deductions, and credits for the year.

Compute and pay tax

Apply the corporate rate and any estimated-tax payments.

File by the deadline

Submit by the corporate return due date.

Key Takeaways

- A foreign-owned U.S. DE uses Form 1120 as a pro forma attachment vehicle for Form 5472.

- Only limited identifying information is required on the pro forma Form 1120.

- These filings use a dedicated fax or mailing address, not the normal Form 1120 address.

- A minimal form still carries serious filing risk.

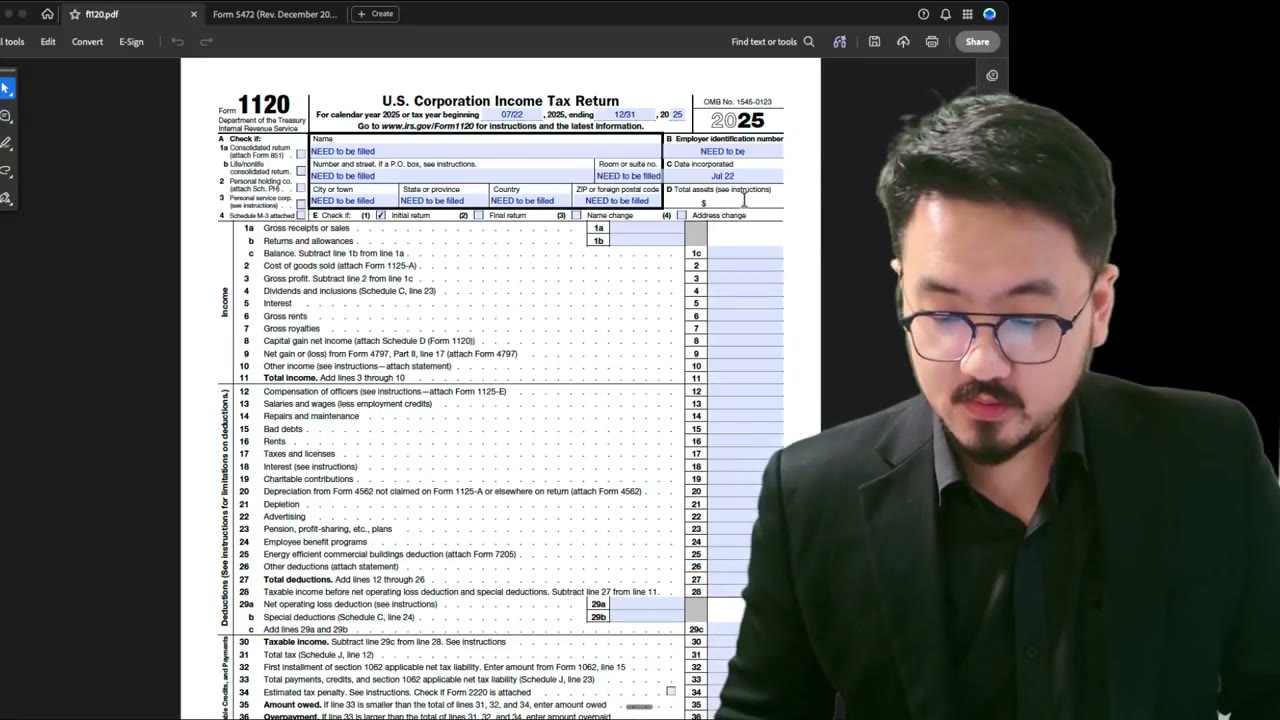

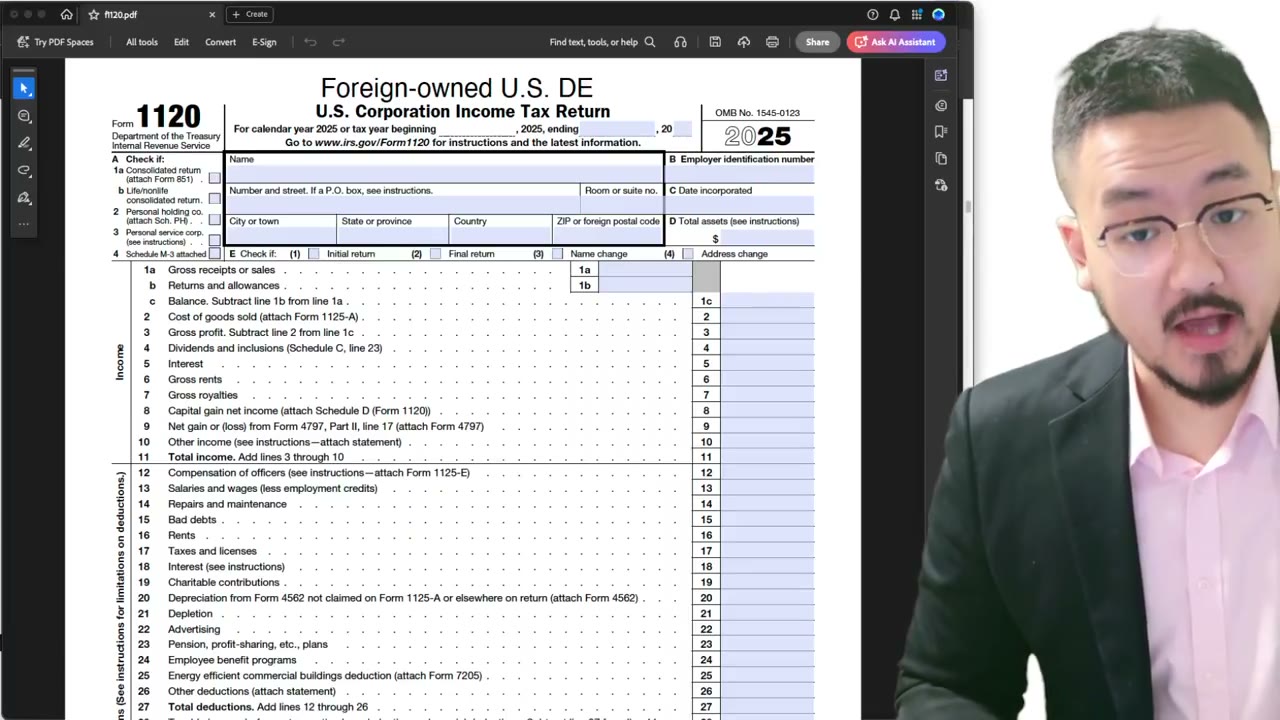

For a foreign-owned U.S. disregarded entity, the Form 1120 is mostly a cover form

The Form 5472 instructions are unusually explicit here. A foreign-owned U.S. disregarded entity does not suddenly have a normal corporate income tax return because of Form 5472. Instead, it files a pro forma Form 1120 with Form 5472 attached, and the only information required on the Form 1120 is the entity's name and address plus items B and E on the first page.

This is why founders should stop copying generic Form 1120 tutorials written for domestic operating corporations.

What to fill, what to skip, and how to submit it

The special filing instructions also say 'Foreign-owned U.S. DE' should be written across the top of the Form 1120. The package must use the dedicated filing route listed in the Form 5472 instructions, either the special fax number or the special Ogden mailing address. These filers do not use the standard Form 1120 mailing address.

That submission detail matters. A correctly prepared package sent to the wrong place is still a bad compliance outcome.

Why this pro forma filing still needs serious attention

The fact that most of Form 1120 is left blank leads some founders to treat the filing casually. That is a mistake. The pro forma return is the attachment vehicle for Form 5472, and the penalty system still applies if the package is late, incomplete, or misfiled. If more time is needed, the entity can request an extension using Form 7004.

The pro forma Form 1120 is minimal, but the consequences of mishandling it are not.

Frequently Asked Questions

Does a foreign-owned LLC fill out a full corporate Form 1120 for the Form 5472 package?

No. The instructions say only the name and address plus items B and E on page 1 are required for the pro forma Form 1120 used by a foreign-owned U.S. DE.

Where do I send the pro forma Form 1120 with Form 5472?

The Form 5472 instructions provide a dedicated fax number and Ogden mailing address specifically for foreign-owned U.S. disregarded entities.

Should I write anything special on the Form 1120 cover page?

Yes. The instructions say 'Foreign-owned U.S. DE' should be written across the top of the Form 1120.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:30

2:30Pro Forma Form 1120: Do You Fill Every Section? (Foreign-Owned DE)

Form 1120 Explained — What It Is, Who Files, and How It Works

Form 1120 Explained: What It Is, Who Files It, and How It Works (2025-2026)

3:35

3:35Form 1120 Item D: Total Assets and Why You Must Fill It Despite Pro Forma Status

Pro Forma Form 1120 Top Page Guide

Pro Forma Form 1120 Top Page Guide for Foreign-Owned LLCs (2025-2026)

2:31

2:31Does Capitalization Matter on IRS Forms? ALL CAPS vs Lowercase (Form 1120 and 5472)

1:55

1:55