Fixing Late or Missed FBARs: Delinquent Filing & Backfile

How to clean up past-due FinCEN 114 reports — the Delinquent FBAR procedures vs Streamlined, the BSA E-Filing backfile mechanics, the six-year statute, who actually files for a foreign-owned LLC, and the post-Bittner non-willful penalty.

Disclaimer: This is independent research and educational analysis, compiled from the IRS Delinquent FBAR and Streamlined pages, the IRS/FinCEN FBAR materials, the Internal Revenue Manual, and the U.S. Code (31 U.S.C. sections 5314 and 5321), current to mid-2026. It is not legal or tax advice, and a delinquent-FBAR fix turns on intensely fact-specific willfulness, residency, and filer-mapping questions. Anyone weighing a disclosure — especially where there are Schedule B issues, prior adviser warnings, or possible willfulness — should consult a qualified attorney or tax adviser before filing.

Key Takeaways

- The first decision is DFSP vs Streamlined: the Delinquent FBAR Submission Procedures fit only when the foreign-account income was already reported and tax paid; if income was omitted, DFSP is the wrong lane and you analyze the Streamlined procedures (or, for willful facts, the Criminal Investigation Voluntary Disclosure Practice).

- There is no paper backfile track anymore — every late or amended FBAR is filed electronically through FinCEN's BSA E-Filing System, and you must select a reason for filing late on the cover page.

- The normal cleanup window is six years of FBARs, because the IRS Appeals manual sets the assessment statute (ASED) for FBAR failure-to-file — willful or non-willful — at six years from the FBAR due date.

- A domestic LLC is itself a United States person for FBAR even if it is disregarded and wholly owned by a nonresident alien — so the FBAR filer is not always the income-tax filer; map the entity, the signers, and the income before choosing a lane.

- After Bittner v. United States (2023), the non-willful penalty is per report, not per account, and the IRM caps total non-willful penalties across open years at 50% of the highest aggregate balance; FBAR penalty merits cases go to district court or the Court of Federal Claims, not the Tax Court.

1. The fork in the road — DFSP or Streamlined

FBAR is a Title 31 reporting system, not an income-tax schedule. Its legal base is 31 U.S.C. section 5314, implemented by 31 C.F.R. section 1010.350, which requires each United States person with a financial interest in — or signature or other authority over — foreign financial accounts to report annually when the aggregate value exceeds $10,000 at any time during the calendar year. The threshold is cumulative across accounts and indifferent to income: an account that earned no interest is still fully reportable.

When you discover missed years, the first decision point is what actually went wrong. If all foreign-account income was already properly reported and the tax paid, a late FBAR plus a reasonable-cause narrative may fit the IRS's Delinquent FBAR Submission Procedures (DFSP). If foreign-account income was omitted from the return, DFSP by itself is generally the wrong lane, and you instead evaluate the Streamlined Filing Compliance Procedures (if the conduct was non-willful) or the IRS Criminal Investigation Voluntary Disclosure Practice (VDP) if willfulness is a concern.

This guide is about fixing the past. If you only need the current-year basics — who files and by when — start with our FBAR overview. If your problem is unreported foreign income across several years, the Streamlined guide walks the SDOP/SFOP mechanics in depth. Here we focus on the decision between those lanes and the backfile mechanics the IRS rarely spells out in one place.

2. When the Delinquent FBAR procedures actually fit

Narrow by design — and not an amnesty contract

The DFSP page is narrow. It is aimed at taxpayers who do not need VDP or Streamlined to file delinquent or amended returns, who have not filed a required FBAR, who are not under IRS civil examination or criminal investigation, and who have not already been contacted by the IRS about the delinquent FBARs. The mechanics are short but specific: review the instructions, include a statement explaining why the FBAR is late, file all delinquent FBARs electronically through BSA E-Filing, and select a reason for filing late on the cover page of the electronic form.

That simplicity does not make DFSP an amnesty. The page is procedural, not a closing agreement. If a late FBAR is later examined, the real protection is the reasonable-cause standard. The current Internal Revenue Manual says a non-willful penalty should not be imposed if the violation was due to reasonable cause and accurate delinquent or amended FBARs are filed — and the IRS's general penalty-relief guidance describes reasonable cause as ordinary business care and prudence under all the facts and circumstances.

The practical rule for foreign-owned LLC owners is straightforward. If the foreign accounts merely created an FBAR duty and all income was already on filed returns, DFSP plus a credible reasonable-cause record may be the right fix. If the accounts also caused underreported interest, dividends, capital gain, Subpart F, GILTI, or PFIC income, you are in amended-return territory and should analyze Streamlined first, not DFSP.

3. How to backfile FBARs now — BSA E-Filing, step by step

The current filing channel is the FinCEN BSA E-Filing System. FinCEN says the FBAR must be filed electronically, and the IRS says not to file it with your federal income tax return. Individuals can use the no-registration filing option; institutions and professional filers register and file through the same platform. If electronic filing is genuinely impossible, the IRS directs filers to FinCEN contacts to explore an alternative — there is no ordinary paper backfile track anymore, even for old report years.

The historical year does not send you back to historical paper forms. Through the old paper era, FBARs were filed on Treasury Form TD F 90-22.1 with a June 30 due date; FinCEN then moved FBAR onto BSA E-Filing and made FinCEN Form 114 the operative electronic successor. Since the 2016 calendar year, the annual due date has been April 15 with an automatic extension to October 15. You backfile every missing year on today's electronic form regardless of how old the report year is.

What you select on the form depends on the lane. For an ordinary delinquent FBAR under DFSP, include a statement explaining why the FBARs are late and select a late-filing reason on the electronic cover page. For a Streamlined submission, the IRS gives exact instructions: file the six delinquent FBARs electronically, select 'Other' as the reason for filing late, and enter 'Streamlined Filing Compliance Procedures' in the explanation box.

Do not attach the certification to the FBAR. The IRS is explicit that the Form 14653 or Form 14654 certification belongs with the paper tax-return package mailed to Austin, not with the electronic FBAR itself.

- File every missing year on FinCEN Form 114 via BSA E-Filing — no paper, no historical forms.

- DFSP: attach a late-reason statement and select a late-filing reason on the cover page.

- Streamlined: select 'Other' and type 'Streamlined Filing Compliance Procedures' in the explanation box.

- Keep, for each account, the name, number, institution name and address, account type, and maximum value — generally for five years from the FBAR due date.

4. How many years — the six-year statute

How far back you backfile depends on the lane, but both converge on six years. Under Streamlined, the answer is fixed by the program: six years of delinquent FBARs for the most recent years whose due date has passed. Outside Streamlined, the practical benchmark is also usually six years, because the IRS Appeals manual states that the assessment statute (ASED) for failure to file an FBAR — whether willful or non-willful — is six years from the FBAR due date.

The due-date arithmetic matters. For calendar years 2015 and earlier, the FBAR was due June 30 of the following year; for 2016 and later, it is due April 15 of the following year. Appeals gives a concrete example: a 2019 FBAR due April 15, 2020 has an assessment statute expiring April 15, 2026 — and the automatic six-month extension does not move that date. That six-year civil-penalty window is why six years is the normal operational cleanup period.

Two further timing rules round out the picture. After the IRS assesses an FBAR penalty, the government generally has two years to bring a civil action to collect it, measured from the later of the assessment date or the date a related criminal judgment becomes final. And the IRS has FBAR-specific consent procedures to extend the assessment period — so a long-running case can stretch beyond the default six years by agreement.

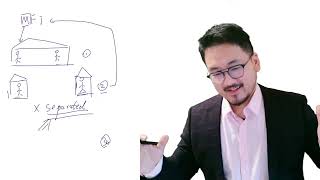

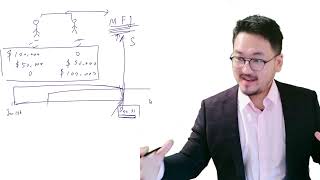

5. Who is the FBAR filer — entity, signers, and spouses

A domestic LLC is itself a US person

For a foreign-owned LLC the single most important point is that the FBAR filer is not always the income-tax filer. The regulation defines a United States person to include an entity — including a limited liability company — created or organized under U.S. law. So if a Delaware, Wyoming, or other domestic LLC holds a foreign bank or brokerage account whose aggregate value crosses $10,000, the LLC itself can have an FBAR filing duty even if it is disregarded for income tax and wholly owned by a nonresident alien.

The flip side is the owner. A foreign individual owner who is not a U.S. citizen, not a resident alien under section 7701(b), and otherwise not a U.S. person does not become personally subject to FBAR solely because he owns a domestic LLC or can sign for its account — the rule reaches United States persons, and domestic-LLC status does not transform a nonresident-alien owner into one. (A U.S. person who owns more than 50% of an entity can, separately, have an FBAR financial interest under the indirect-ownership rule.)

Signature authority is the common trap in closely held LLCs. The regulation separately requires FBAR reporting by a United States person who can control the disposition of money or assets in a foreign account by direct communication with the institution — even with no ownership stake. The exceptions are narrow (regulated banks, certain SEC/CFTC registrants, and the like), and a small foreign-owned LLC usually fits none of them. So if the LLC's U.S.-resident manager or employee can instruct the bank, that person may have an individual FBAR duty on top of the entity's.

Joint accounts work differently than many expect. The regulation says that when an account is in the name of more than one person, each United States person named has a financial interest in it. A U.S.-person spouse on a joint foreign account with a nonresident-alien spouse generally reports the joint account if the threshold is met — while the NRA spouse has no individual FBAR duty unless that spouse is also a U.S. person. FinCEN's operational materials recognize spouse filing authorizations through Form 114a, but the single-FBAR-for-both-spouses rule is narrow and should be checked against the current line-item instructions at filing time.

6. Penalties after Bittner — per report, not per account

The Supreme Court's 2023 decision in Bittner v. United States changed the math for non-willful penalties. The Court held that the best reading of the Bank Secrecy Act treats the failure to file a legally compliant annual report as one violation carrying a maximum non-willful penalty of $10,000 — not a separate $10,000 for each account omitted from that one report. IRS examination guidance now reflects that: the current IRM says examiners will, in most non-willful cases, recommend one non-willful penalty per violation, and it caps total non-willful penalties across all open years at 50% of the highest aggregate balance of the related accounts. The reasonable-cause exception remains available, and the statutory amounts are subject to annual inflation adjustments for post-2015 violations.

Willful exposure is far harsher, and Bittner did not soften it. Under 31 U.S.C. section 5321(a)(5)(C), the statutory maximum for a willful violation is the greater of $100,000 or 50% of the account balance at the time of the violation — again subject to inflation adjustment in practice. The IRM continues to treat recklessness and willful blindness as forms of willfulness, and specifically notes that false or unanswered Schedule B foreign-account questions, combined with other facts, can support a willfulness finding. That distinction is exactly why the gatekeeping choice between DFSP/Streamlined and VDP is, at bottom, a willfulness analysis.

Because willfulness drives everything, be honest about it before you file. Choosing a non-willful lane on willful facts turns the submission itself into evidence. If the accurate characterization is reckless, willfully blind, or knowing, the IRS points those taxpayers to VDP, not DFSP or Streamlined.

7. FBAR vs Form 8938 — two filings, different law

Form 8938 is not a substitute for the FBAR, and many cleanup cases involve both. The IRS comparison chart says the Form 8938 requirement does not replace or affect the duty to file FinCEN Form 114 — both may be required for the same year. The triggers differ sharply: FBAR generally uses the $10,000 aggregate-account test, while Form 8938 uses much higher thresholds that vary by filing status and residence.

The scope and the procedural law also diverge. FBAR reaches foreign financial accounts and signature authority; Form 8938 reaches specified foreign financial assets — including many non-account investment assets — but generally does not require reporting based solely on signature authority. FBAR is a Title 31 filing with its own six-year civil-penalty regime. Form 8938 is a Title 26 filing attached to the income-tax return, and 26 U.S.C. section 6501(c)(8) can hold the income-tax assessment period open until three years after the required information is furnished — while section 6501(e)(1)(A)(ii) can produce a six-year income-tax statute when more than $5,000 of omitted gross income is attributable to assets that should have been reported under section 6038D.

The practical upshot: a complete FBAR cleanup often forces a parallel look at 8938 and the income-tax statute. Fixing the Title 31 report without confirming the Title 26 position can leave the income-tax assessment window open far longer than the FBAR's six years.

8. Where FBAR penalty fights are litigated

On forum selection, FBAR penalty merits cases are generally not Tax Court cases. The IRS Appeals manual states that the venues to challenge FBAR penalties are the United States district courts and the Court of Federal Claims — not the United States Tax Court. That is why the major modern FBAR authorities are Supreme Court, circuit, district-court, and Court of Federal Claims decisions rather than ordinary Tax Court deficiency cases.

That distinction has real consequences for how a disputed assessment plays out. Unlike an income-tax deficiency — which a taxpayer can usually contest before paying by petitioning the Tax Court — an FBAR penalty dispute typically reaches a court through collection litigation or a refund posture in district court or the Court of Federal Claims. It is a different procedural world, and one more reason to get the lane and the certification right at the filing stage rather than counting on a friendly forum later.

Public enforcement after Bittner is clearer on procedure than on settlement volume. The Examination and Appeals manuals were both revised to incorporate Bittner guidance, and DOJ has continued to prosecute offshore-account cases. What the official record does not provide is a nationwide public dataset of post-Bittner FBAR settlements or a published count of non-willful assessments reduced after the decision — so any claim about settlement statistics should stay cautious and procedural rather than numerical.

9. A clean cleanup — the order of operations

Put the pieces together in order. First, map three facts: the entity (does a domestic LLC hold the foreign account?), the signers (can a U.S.-resident manager or employee instruct the bank?), and the income (was foreign-account income reported on the relevant returns?). Those three answers — not the number of accounts — decide whether you are in DFSP, Streamlined (SDOP or SFOP), or VDP territory.

Second, pick the lane honestly. All income reported, no exam, never contacted about the FBARs, non-willful conduct: DFSP with a reasonable-cause statement. Omitted income, non-willful: Streamlined. Reckless, willfully blind, or knowing conduct: stop and consider VDP with counsel before filing anything.

Third, execute the mechanics. Backfile every covered year on FinCEN Form 114 through BSA E-Filing, selecting the correct late-filing reason (or 'Other' + 'Streamlined Filing Compliance Procedures' for a streamlined package), and keep the certification with the paper return package — never with the FBAR. Then build the file as though an examiner will read it: the complete submission set, e-file confirmations, proof of mailing for any paper package, the tax and interest computations, and the account statements and valuation support behind every number. Because these procedures are intensely fact-specific — and willfulness and residency questions turn on the details — anyone with Schedule B exposure, prior adviser warnings, or possible willfulness should consult a qualified attorney or tax adviser before filing.

DFSP vs Streamlined vs VDP at a glance

| Feature | Delinquent FBAR (DFSP) | Streamlined (SDOP/SFOP) | Voluntary Disclosure (VDP) |

|---|---|---|---|

| When it fits | FBAR only; all income already reported and tax paid | Unreported foreign income, but conduct was non-willful | Willful conduct with criminal exposure |

| Returns required | None — FBARs only | 3 years of returns + certification (14654/14653) | Typically 6 years of returns under a CI process |

| FBAR years to backfile | Usually 6 (the ASED window) | 6 (fixed by the program) | Generally 6 under the disclosure terms |

| Late-reason on Form 114 | Select a late-filing reason + statement | "Other" + "Streamlined Filing Compliance Procedures" | As directed by the CI disclosure process |

| Penalty posture | No structured penalty; reasonable cause is the defense | 5% offshore penalty (SDOP) or none (SFOP) | Defined civil penalty framework; criminal protection |

Related on ForeignLLCTax

Primary sources

- IRS — Delinquent FBAR Submission Procedures

- IRS — Report of Foreign Bank and Financial Accounts (FBAR)

- IRS — Streamlined Filing Compliance Procedures (overview)

- IRS — U.S. taxpayers residing in the United States (SDOP)

- IRS — U.S. taxpayers residing outside the United States (SFOP)

- IRS — Comparison of Form 8938 and FBAR requirements

- IRS CI — Voluntary Disclosure Practice

- Cornell LII — 31 U.S.C. § 5314 (FBAR reporting requirement)

- Cornell LII — 31 U.S.C. § 5321 (FBAR civil penalties & 6-year statute)

- Cornell LII — 31 C.F.R. § 1010.350 (who must report foreign accounts)