Short Tax Year Mechanics: Annualization & Reporting Implications

Key Takeaways

- Annualization (§443) doesn't apply to pro forma Form 1120 — no income to annualize

- Calendar year, fiscal year, and short year are three distinct concepts that can overlap

- Each tax year (short or full) gets its own Form 5472 — don't combine periods

- Short-year filings get more IRS attention statistically — keep documentation

- Form 1128 (Application to Adopt, Change, or Retain a Tax Year) is required for accounting period changes

Annualization — What It Means and When It Applies

"Annualization" is the IRS adjustment that scales a short-year income figure up to a 12-month equivalent for tax-rate calculations. The mechanic: take the short-year income, multiply by 12 / number of months in the short year, and apply the tax rate to the annualized amount — then prorate the resulting tax back to the short period.

For foreign-owned LLCs filing pro forma Form 1120: annualization doesn't apply. The pro forma has no income, no deductions, no tax computation. The pro forma is filed for the short period exactly as-is.

Annualization matters for real corporate returns (Form 1120 with actual income) and for short-year individual returns (Form 1040 in dissolution / change-of-status scenarios). It's a §443 mechanic that foreign-owned DE filers don't need to worry about.

Calendar Year vs Fiscal Year vs Short Year

Three distinct concepts:

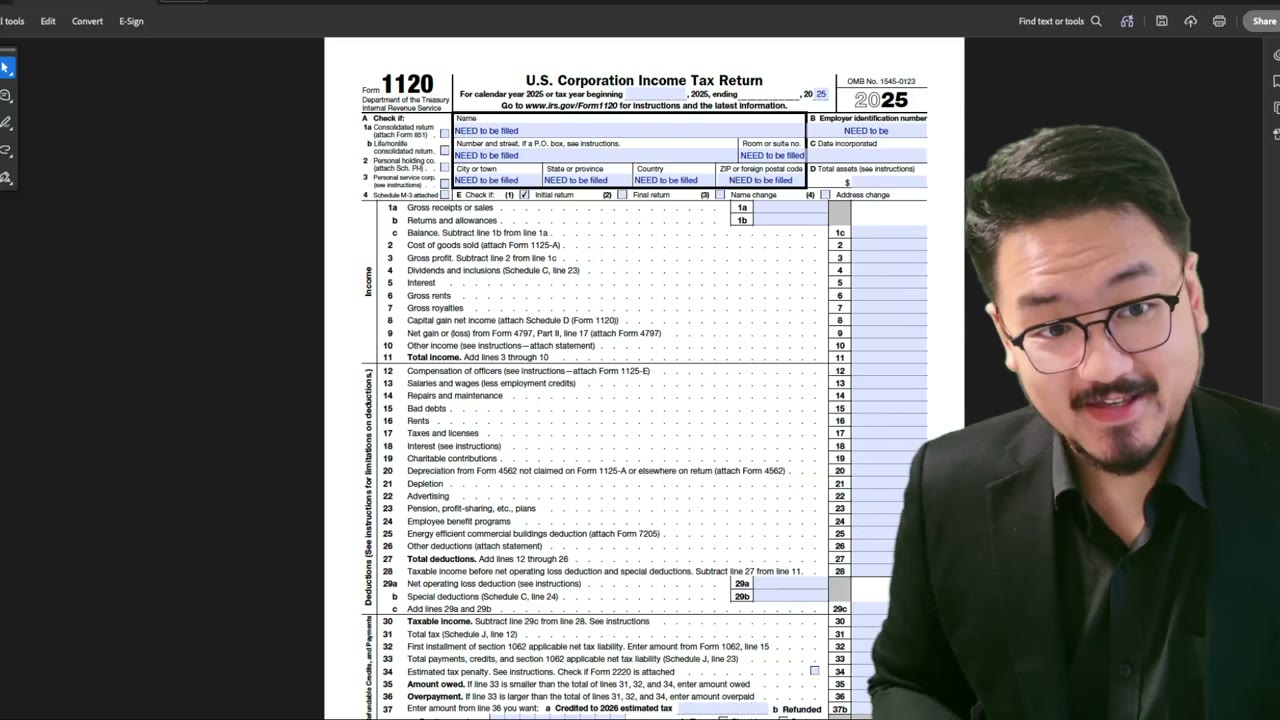

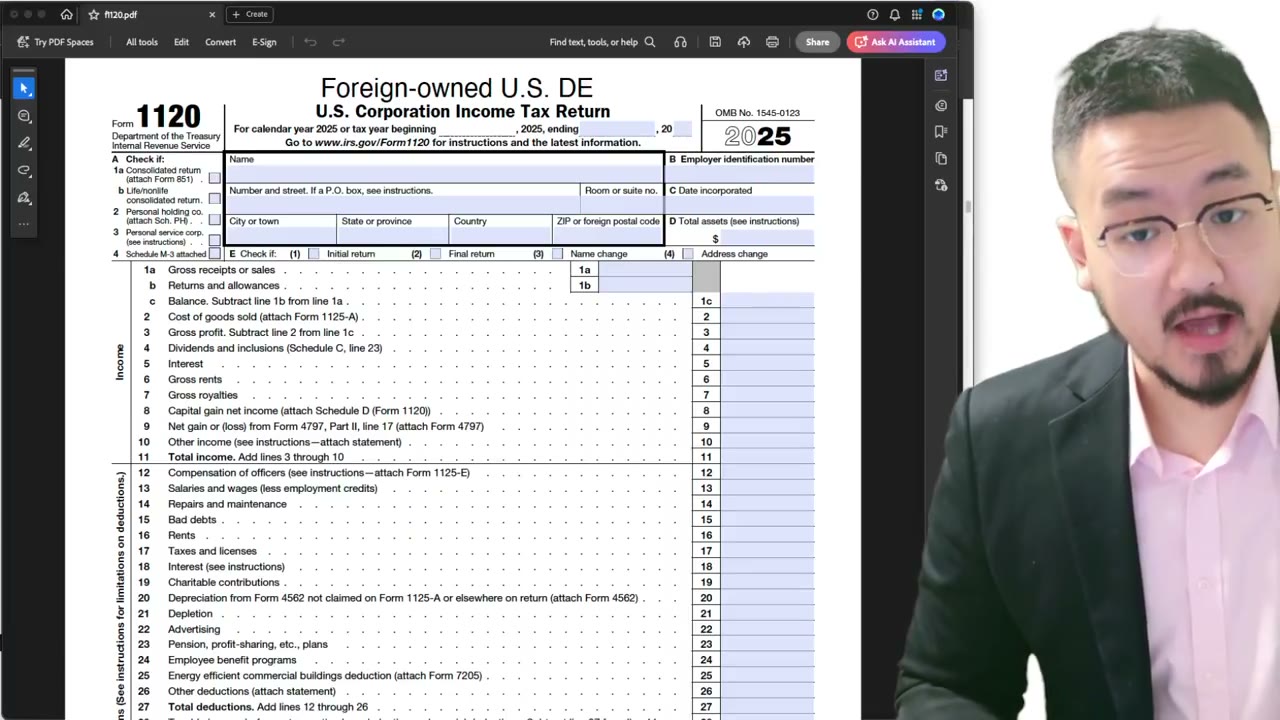

Calendar year: January 1 - December 31. Default for individuals and most small LLCs. The Form 1120 line at the top says "For calendar year [YEAR]" — check that or fill the year.

Fiscal year: Any 12-month period ending on the last day of a month other than December. Common for businesses with seasonal cycles (e.g., a July-to-June fiscal year for an Australian-controlled LLC matching the Australian tax year). Requires IRS approval via Form 1128.

Short tax year: Less than 12 months. Triggered by first year, final year, or accounting period change. Always requires explicit beginning and ending dates on the form.

These are not mutually exclusive — your first calendar year can also be a short tax year. The labels describe different aspects of the same period.

How Short Years Interact with Form 5472 Reporting

Form 5472 reports transactions between the reporting corporation (your LLC) and related parties during the reporting period. For a short year, the reporting period is the short year — not the full calendar year.

If you formed your LLC on October 15, 2025 and contributed $50,000 of capital on November 1, 2025, that contribution is reported on the short-year Form 5472 for October 15 - December 31, 2025.

If you made a second contribution of $30,000 on January 5, 2026, that's a new tax year (calendar year 2026) — reported on the next year's Form 5472, not on the short year.

Don't combine multiple periods into one Form 5472. Each tax year has its own form.

Common Audit Triggers in Short-Year Filings

Short-year filings get more IRS attention than full-year filings, statistically. Reasons:

1. First-year filings are inherently incomplete data points — examiners want to verify the formation was legitimate and the entity is who they say they are.

2. Dissolution-year filings are the last opportunity to assess any tax due before the entity disappears. Examiners review for unreported income, undistributed gains, or final-year transactions that don't fit normal patterns.

3. Accounting period changes raise suspicion of timing manipulation — moving income into one period to avoid tax in another. Even for pro forma filings (no tax), this gets scrutiny.

Keep documentation supporting the short-year facts: formation documents (for first year), dissolution paperwork (for final year), Form 1128 approval letter (for period change). Have it ready in case the IRS asks.

Frequently Asked Questions

Do I need to annualize anything on my pro forma 1120?

No. The pro forma has no income, no deductions, no tax. There's nothing to annualize. Annualization is a §443 mechanic for real corporate returns with income.

Can I file a short-year return on extension via Form 7004?

Yes. Form 7004 (Application for Automatic Extension of Time to File) works for short-year returns the same as full-year. The extension is 6 months from the original due date.

If my LLC formed and dissolved in the same calendar year, do I file two returns?

Yes. One short-year initial return covering formation to dissolution, marked as both 'Initial return' and 'Final return' on Form 1120. Combine the periods into a single short-year filing only if they're contiguous.

How do I report transactions that span the end of a short year?

Allocate by the date of each transaction. A capital contribution on December 15 belongs to that year's short return; a contribution on January 5 belongs to next year's. The transaction date controls, not the planning date.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:00

2:00What Is a Short Tax Year? Definition & Basics for Form 1120 Filers

2:30

2:30Form 1120 Tax Year Demo: Beginning, Ending & Short-Year Filings

2:56

2:56Form 1120 Short Tax Year: How to Enter Beginning and Ending Dates (Foreign Owners)

1:55

1:55Form 1120 Short Tax Year: How to Fill the Begin/End Dates and Initial Return Box

Form 1120 Filing Deadlines, Extensions, and Payment Rules

Form 1120 Filing Deadlines and Extension Rules for C Corporations (2025-2026)

LLC Elected as C-Corp — Filing Requirements and Special Rules