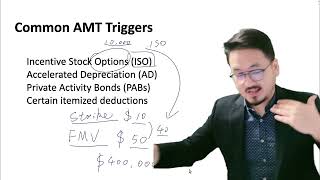

Accelerated Depreciation and AMT: Common AMT Trigger

Key Takeaways

- Regular tax uses faster MACRS depreciation; AMT uses slower methods

- The difference creates a timing adjustment that can trigger AMT

- Most impactful for businesses with large depreciable asset purchases

- This is a timing difference — total depreciation is the same over the asset's life

- AMT paid due to depreciation timing may be recoverable through future AMT credits

Accelerated Depreciation and AMT

The U.S. tax system uses MACRS (Modified Accelerated Cost Recovery System) for depreciation, which allows businesses to recover the cost of assets faster in earlier years. Under the regular tax system, you might use 200% declining balance depreciation. Under the AMT system, depreciation is generally calculated using 150% declining balance or straight-line methods.

This difference in depreciation speed creates a temporary timing difference between regular tax and AMT, potentially triggering AMT in the years when accelerated depreciation is highest.

Why This Matters for Business Owners

If your business has significant depreciable assets — equipment, vehicles, machinery — the accelerated depreciation deductions that reduce your regular tax may simultaneously increase your AMT exposure. This is particularly relevant for capital-intensive industries like manufacturing, technology infrastructure, and real estate.

The good news is that this is a timing difference, not a permanent one. Over the life of the asset, total depreciation is the same under both systems. The AMT paid in early years may generate credits that can be recovered in later years.

Frequently Asked Questions

Does Section 179 also trigger AMT?

Section 179 expensing is generally allowed for both regular tax and AMT purposes, so it typically does not create an AMT adjustment. However, the interaction between Section 179, bonus depreciation, and overall AMT calculations can be complex.

Is post-2017 property affected?

The TCJA changed depreciation rules (including 100% bonus depreciation), which has altered the AMT impact of depreciation for property placed in service after 2017. As bonus depreciation phases down, the AMT impact of depreciation timing differences may increase again.

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Alternative Minimum Tax (AMT)

5:18

5:18ISO and AMT: How Incentive Stock Options Trigger AMT

4:08

4:08Private Activity Bonds and AMT: What Investors Need to Know

4:22

4:22Alternative Minimum Tax (AMT) Explained Simply

3:55

3:55Why the Alternative Minimum Tax Exists: A Brief History

5:33

5:33AMT Credit Carryforward: Recovering Alternative Minimum Tax Paid

AMT Foreign Tax Credit and Form 8801 Guide