Form 5472 Attachment: Sample Disclosure for a Formation-Only Year (Stripe Atlas)

Key Takeaways

- A simple no-activity attachment can be a single paragraph describing just the formation contribution

- Always include: date, type (capital contribution), amount in USD, related party name, brief context

- Cite the Treasury regulation for the transaction type (§1.6038A-2(b)(5) for contributions)

- End with "No other reportable transactions occurred during this tax year" if true — explicit closure

- Sign and date the attachment yourself (no IRS template); attach to the main filing package, never send separately

A Concrete Example: Just a Formation Contribution

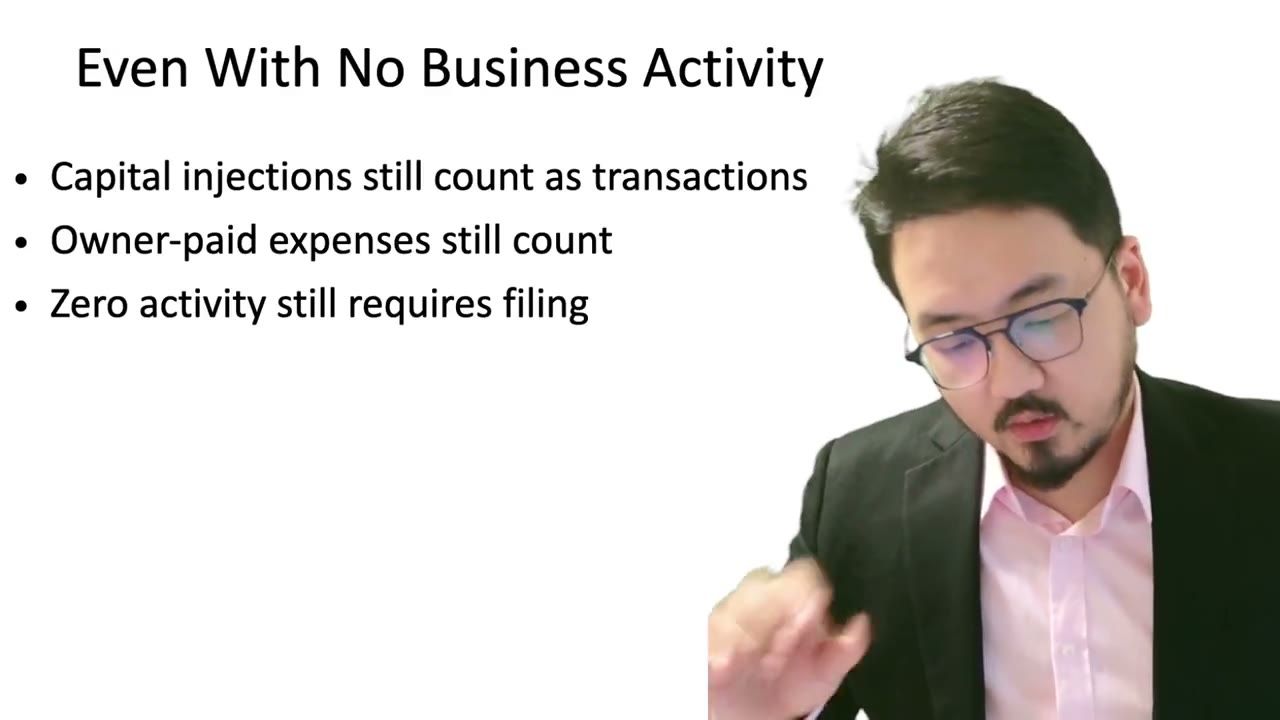

Let's work through the simplest case: a foreign owner formed an LLC during the tax year using a service like Stripe Atlas, paid the formation fee personally, and had no other transactions for the rest of the year. The attachment can be very short.

The story: the LLC didn't exist yet when the formation fee was paid (no EIN, no bank account), so the foreign owner advanced the $250 service fee out of personal funds. The LLC didn't reimburse the owner. Under the typical accounting, this is a capital contribution.

Sample Disclosure Text

Here's a complete, ready-to-use disclosure for the formation-only scenario:

---

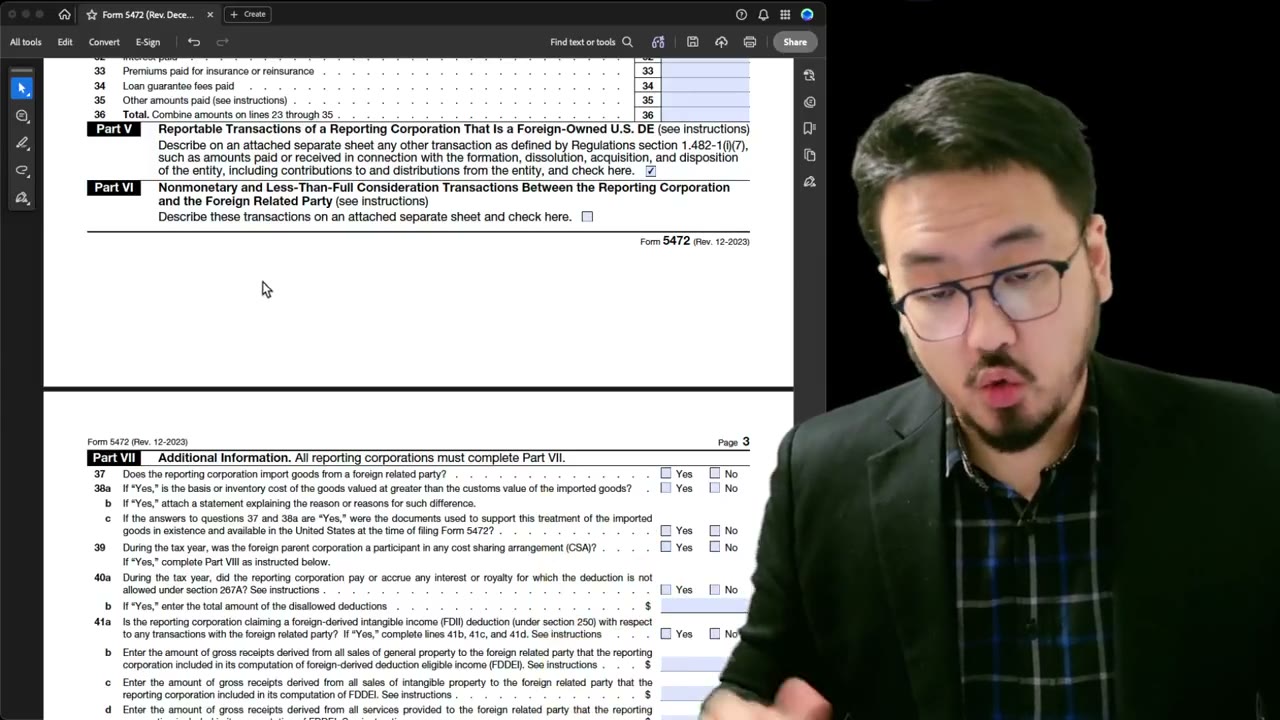

Attachment to Form 5472 — Other Reportable Transactions Under Treasury Regulation §1.6038A-2

Report of Transactions of a Foreign Corporation That Is a Foreign-Owned U.S. Disregarded Entity

Tax Year: 2025

Reporting Corporation: [LLC Legal Name]

EIN: 12-3456789

Description of Reportable Transaction:

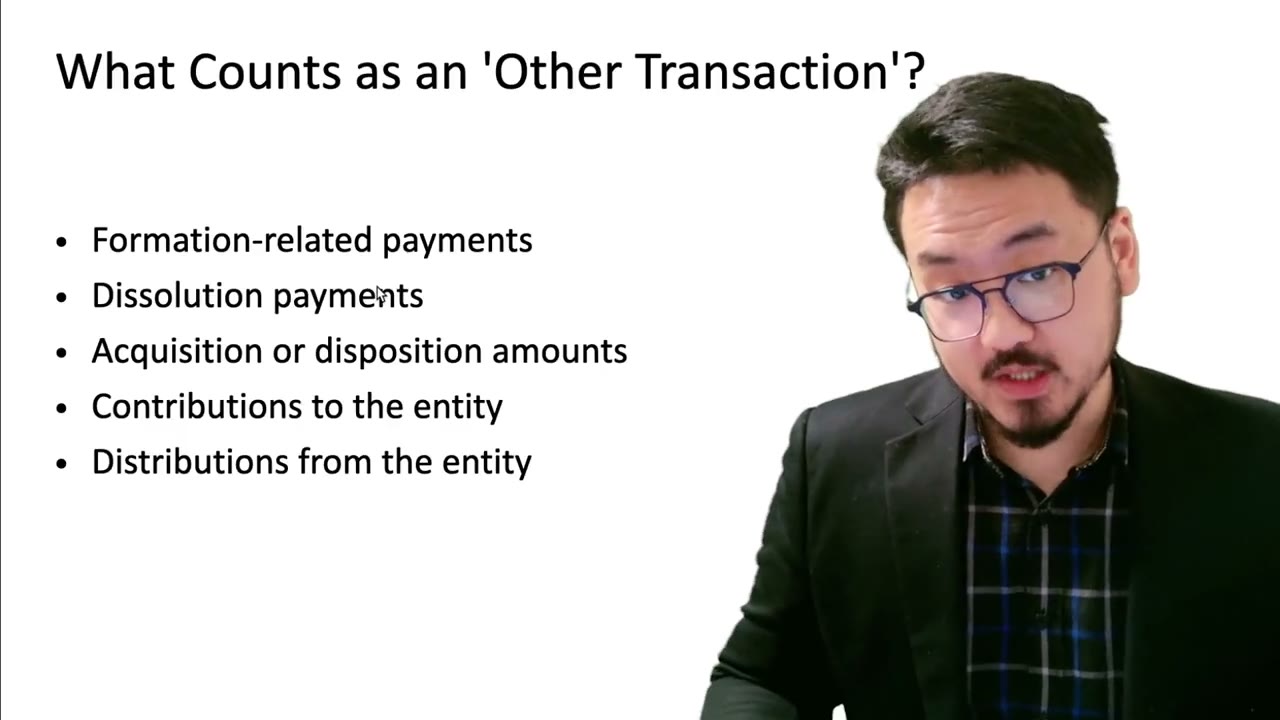

During the tax year, the sole foreign owner [Owner Name] paid $250 USD directly to Stripe Atlas on behalf of the LLC for formation services. This payment was made before the LLC obtained an EIN or opened a bank account. The LLC did not reimburse the owner for this payment. This payment is treated as a capital contribution under Treasury Regulation §1.6038A-2(b)(5).

No other reportable transactions occurred during this tax year.

Date: [Filing Date]

Signed: [Signature]

Name: [Owner Name]

Title: Owner

---

That's a complete attachment for a no-activity LLC with only a formation cost. Short, specific, signed.

Including Registered Agent Fees in the Same Attachment

If the owner also paid registered agent fees during the year (typical $50–$200), expand the same attachment:

"During the tax year, the sole foreign owner [Name] paid $200 USD directly to [Registered Agent Service Name] on behalf of the LLC for registered agent services. This payment was made from personal funds without reimbursement and is treated as a capital contribution under §1.6038A-2(b)(5)."

Add this as a second paragraph under the description section. The structure stays the same; the volume of disclosure scales with the volume of transactions.

Date, Type, Amount — The Required Trinity

Each transaction needs the three core data points: date, type, amount. The video's framing: you already have the type (capital contribution) from the regulation, you need the date (when the payment happened) and the amount (in USD).

Dates can be specific ("July 15, 2025") or approximate ("during July 2025"). Amounts must be in USD, even if the underlying payment was in another currency — convert at the spot rate on the transaction date if needed.

For very small recurring payments (e.g., a $9/month bank account fee paid for 12 months), you can summarize as "total of $108 during 2025 in monthly bank fees" without listing each month.

Related Party: Sole Foreign Owner [Name]

Always identify the related party by their full name. "The sole foreign owner" alone isn't enough — the IRS wants the specific identity. "The sole foreign owner, [First Name Last Name], who is a citizen and tax resident of [Country]" is the gold standard.

If you have a reference ID number, you can include it: "the sole foreign owner, [Name] (Reference ID: WANG-LLC-25)." This ties the attachment to the Part II/Part III identification on the form itself.

Sign the Attachment, but No IRS Sign Field

Unlike Form 1120 (which has a structured signature field), the attachment has no IRS-defined signature field. You add the signature yourself at the bottom, with: date, signature, name, title.

The signature confirms the attachment is part of the filing under penalty of perjury — same legal weight as the main form's signature. Some practitioners skip the attachment signature; the IRS hasn't always enforced this, but the safe practice is to include it.

Attach to the Fax/Mail Package

If faxing, the attachment is just one of the pages in the assembled PDF you fax. Include it in the page sequence: pro forma Form 1120 (first), Form 5472 (next), attachment (last). The IRS fax intake system reads the whole package as one filing.

If mailing, the attachment is the last document in the envelope. Stack them in the same order: 1120, 5472, attachment. Use a paperclip or staple to keep them physically together; the IRS processing center sometimes shuffles loose pages.

No separate envelope or filing — the attachment travels with the main filing as a unified package.

Frequently Asked Questions

Is a one-paragraph attachment really enough for a single-formation-cost year?

Yes — if it includes all four required elements (amount, nature, related party, factual detail) and the explicit closure statement. The IRS doesn't reward length; they reward clarity and completeness.

Can I leave out the reference ID if I included it on the main form?

You can, but redundancy doesn't hurt. Including the reference ID in the attachment makes it self-contained and traceable if it ever gets separated from the main form package.

What if I forget to attach the §1.6038A-2 supplementary document?

The filing is considered incomplete, which can trigger the $25,000 failure-to-file penalty. If you realize after sending, send a supplementary filing immediately with a brief cover letter explaining the omission and including the missing attachment. Don't wait for the IRS to notice.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

3:55

3:55Form 5472 Attachment: Document Structure, Treasury Regulation Citation, Signature

3:15

3:15Form 5472 §1.6038A-2 Attachment: Required Elements and Disclosure Examples

1:55

1:55Pro Forma 1120 + Form 5472: Why Dormant LLCs Still Owe the $25,000 Filing

5:00

5:00Form 5472 Attachment: Capital Contribution vs. Loan, Distribution, Dissolution Payments

Form 5472 Part VI — Do You Need a Statement About the Owner-Manager Relationship?

Form 5472 Part VI Attachment: Owner-Manager Nonmonetary Transaction Disclosure

3:25

3:25