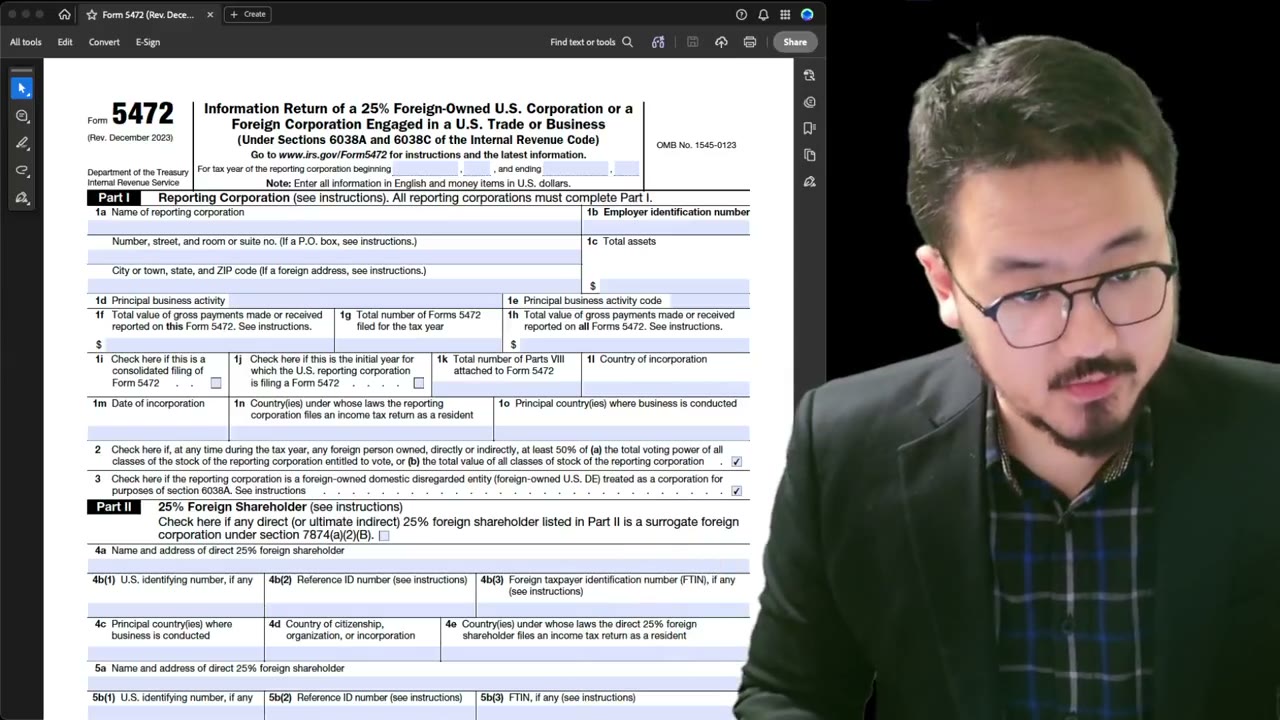

Form 5472 §1.6038A-2 Attachment: Required Elements and Disclosure Examples

Key Takeaways

- The §1.6038A-2 attachment is often more substantive than Part IV for foreign-owned single-member LLCs

- Four required elements: amount, nature, related party, sufficient factual detail

- Treat the attachment as a narrative document — paint the picture so the reviewer sees the full context

- Apply the disclosure requirement to all reportable transactions, including small recurring ones (can be summarized)

- No IRS template; create your own document with clear title, headers, and signature

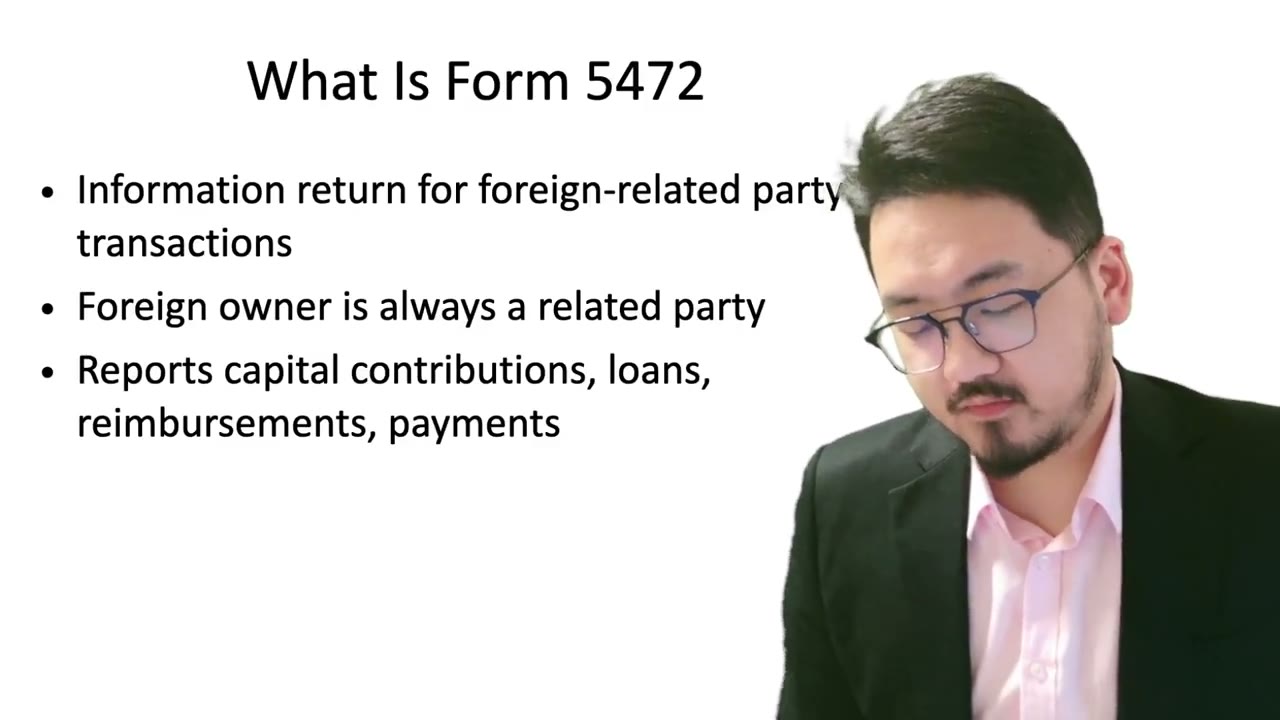

The "Other Transactions" Attachment — Surprisingly Important

The supplementary attachment under Treasury §1.6038A-2 has a misleadingly bland name ("other transactions"), but for foreign-owned U.S. disregarded entities (DEs), it's arguably more important than the structured Part IV line items.

For a typical foreign-owned single-member LLC, the monetary transactions on Part IV are often small or zero. The substance of the filing — the cross-border financial story the IRS actually cares about — lives in this attachment.

What Must Be Disclosed in the Attachment

Per the regulation, the attachment must include:

- **Amount paid or received** in the transaction - **Nature of the transaction** — what kind of transaction it was (capital contribution, loan, distribution, etc.) - **Identification of the related party** — by name and (if applicable) reference ID/TIN - **Sufficient factual detail** to make the transaction comprehensible to the IRS reviewer

The last element is the most subjective. "Sufficient factual detail" means enough context that a reader who knows nothing about your business can understand what happened. Not a one-liner; not a thesis; somewhere in between.

Why You Should Tell a Story, Not Just List Numbers

The video's framing: "I'm telling the story — I'm painting the picture for the IRS person who will look at this." This isn't a romantic flourish; it's practical advice.

IRS reviewers see thousands of Form 5472 attachments. The ones that get processed quickly without follow-up are the ones that read like a coherent narrative: what the LLC is, who the foreign owner is, what kinds of transactions happened, why they happened in business terms, and how the dollar amounts trace back to specific events. A pure data dump ("Transaction 1: $300, contribution; Transaction 2: $150, contribution") gets flagged for review because the reviewer can't see the bigger picture.

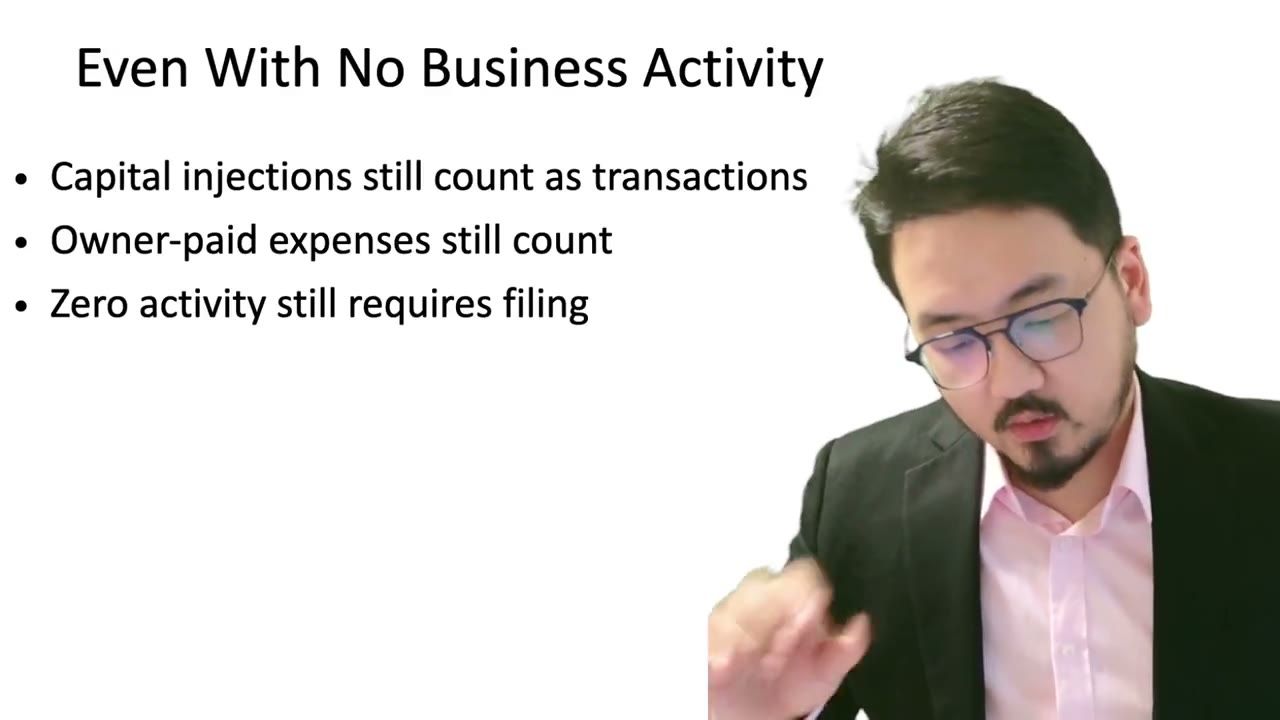

Apply to Every Transaction, Not Just the Big Ones

The attachment requirement applies to every reportable transaction, not just the largest ones. A $300 capital contribution to cover state franchise tax needs the same four elements (amount, nature, related party, factual detail) as a $300,000 capital injection.

For very small recurring transactions, you can summarize: "During the tax year, the foreign owner paid registered agent fees totaling $200 ($100 in March, $100 in September) on the LLC's behalf, treated as capital contributions." That captures all four elements without listing each transaction separately.

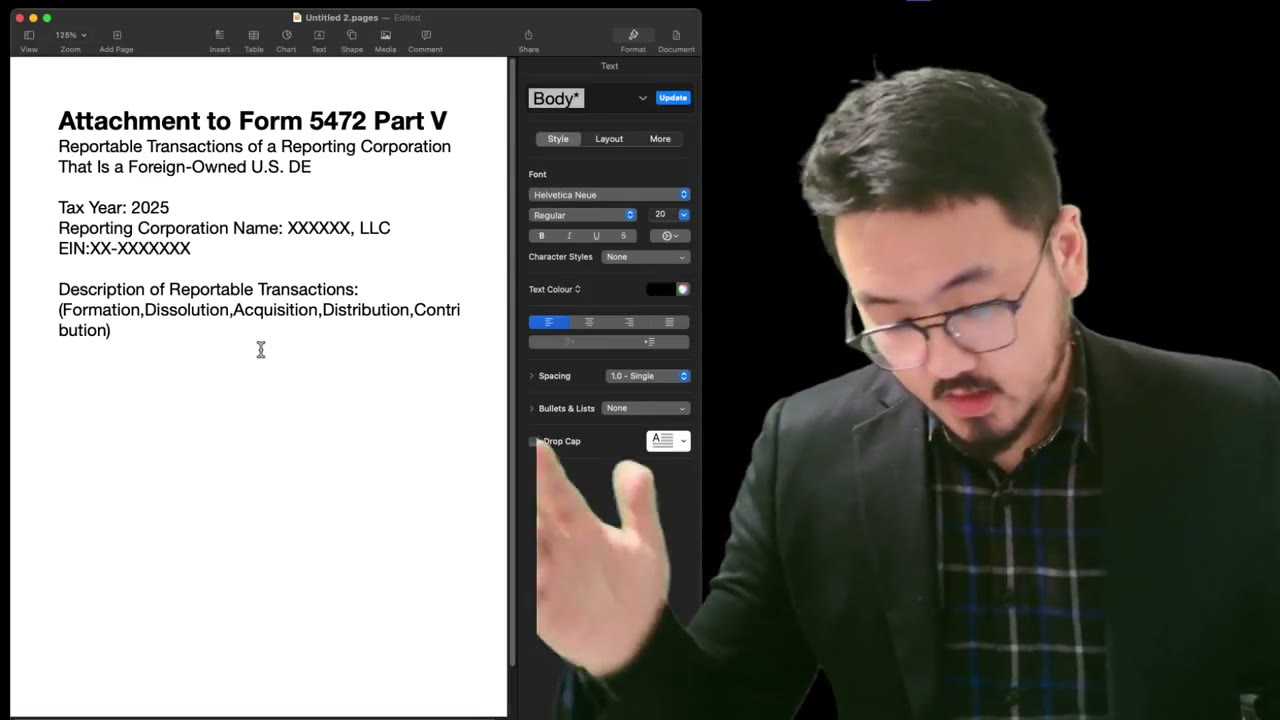

The Attachment Is Made by You (No IRS Template)

The IRS doesn't provide a template for this attachment. You create the document yourself, in plain text or PDF, with whatever formatting helps the reviewer.

A practical structure: title at the top ("Attachment to Form 5472 — Other Reportable Transactions Under §1.6038A-2"), tax year and reporting corporation name, EIN, then the body content. Add section headers if you have multiple transaction types. Sign and date at the bottom (same person who signed Form 1120 / Form 5472).

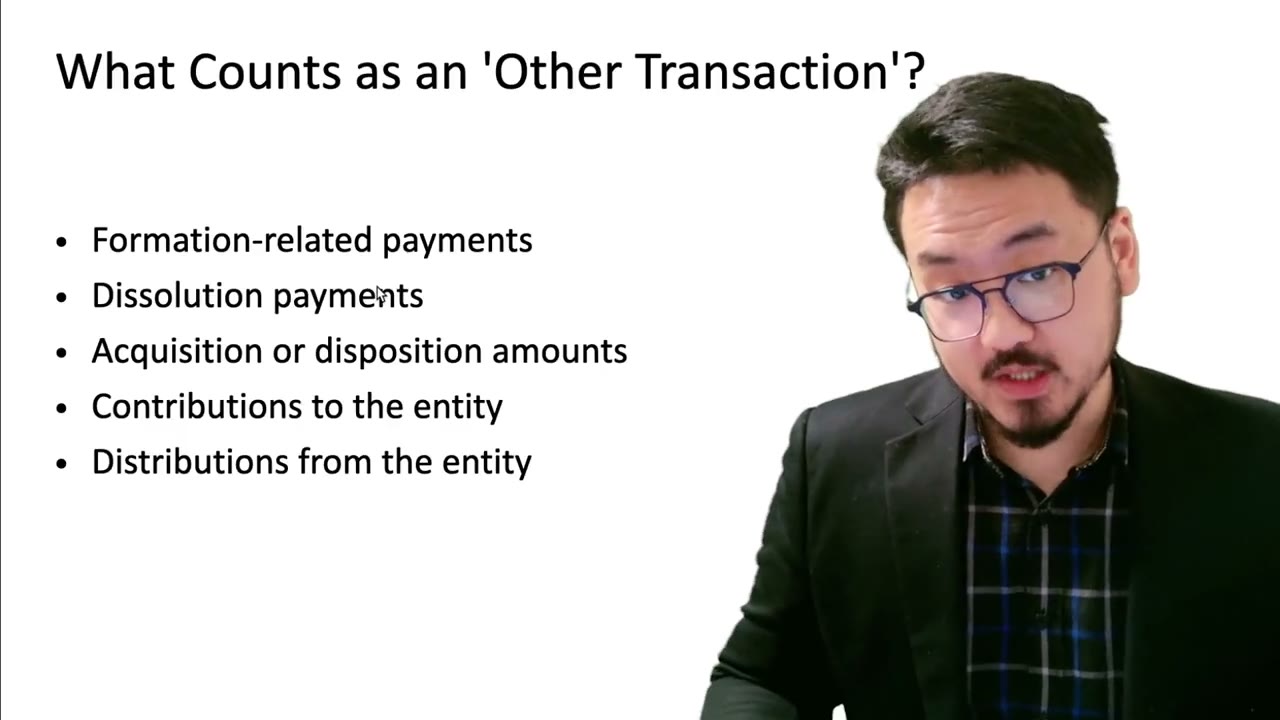

Practical Examples of Reportable "Other Transactions"

Examples that should always be reported in the attachment:

- **Formation costs paid by the owner** (Atlas, doola, attorney fees) — capital contribution - **State franchise tax paid by the owner personally** — capital contribution - **Registered agent fees paid by the owner** — capital contribution - **Owner advances funds for any business expense** — capital contribution or loan, depending on intent - **LLC distributes profits or excess capital back to owner** — distribution - **Dissolution payments back to owner** — distribution at dissolution - **In-kind transfers of equipment or intellectual property** — capital contribution (with valuation) - **Cross-border accommodations** (owner uses LLC's resources for personal use, or vice versa) — depending on facts

Frequently Asked Questions

How long should the attachment be?

Long enough to convey the story; usually 1–3 pages for a single-member LLC. For complex multi-transaction filings, 3–10 pages is common. Don't pad — clarity matters more than length.

Can the attachment be the same format as the Form 5472 PDF?

Sure — but it can also be a separate Word doc or plain text PDF. The IRS accepts any readable format. Just make sure the attachment is clearly labeled and pages are numbered so it doesn't get separated from the Form 5472 it accompanies.

Do I need to sign the attachment separately?

Yes — sign and date the attachment at the bottom, using the same signature as on Form 1120. This confirms the disclosures are made under penalty of perjury, same as the rest of the filing.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

2:20

2:20Pro Forma 1120 + Form 5472: What Counts as a Reportable Transaction with Your LLC

5:15

5:15Form 5472 Attachment: Sample Disclosure for a Formation-Only Year (Stripe Atlas)

3:55

3:55Form 5472 Attachment: Document Structure, Treasury Regulation Citation, Signature

1:55

1:55Pro Forma 1120 + Form 5472: Why Dormant LLCs Still Owe the $25,000 Filing

2:10

2:10Form 5472: Why the §1.6038A-2 Attachment Is Mandatory (Don't Skip)

5:00

5:00