Form 5472 Attachment: Capital Contribution vs. Loan, Distribution, Dissolution Payments

Key Takeaways

- Even "no activity" LLCs almost always have reportable transactions: formation contributions, franchise tax, registered agent fees

- Capital contributions = inflows (owner pays in); distributions = outflows (LLC pays back to owner)

- Dissolution distributions are reportable — the last transaction is often the biggest

- Each transaction needs date, type, amount, brief description in the attachment

- Default to capital contribution over loans unless you have specific tax reasons; loans require interest + documentation

Even a No-Activity LLC Has Reportable Transactions

The most common scenario for foreign-owned single-member LLCs is also the most misunderstood: "I had no business activity this year." To the IRS, that's almost always wrong — because the act of forming the LLC itself involves reportable transactions.

When you formed the company, you contributed startup capital. That contribution is a reportable transaction between you (foreign related party) and the LLC (U.S. reporting corporation). And if at any point you distributed some funds back to yourself, that's another reportable transaction in the opposite direction.

Capital Contributions and Distributions — Always Reportable

These two are the bread-and-butter reportable transactions for a single-member LLC:

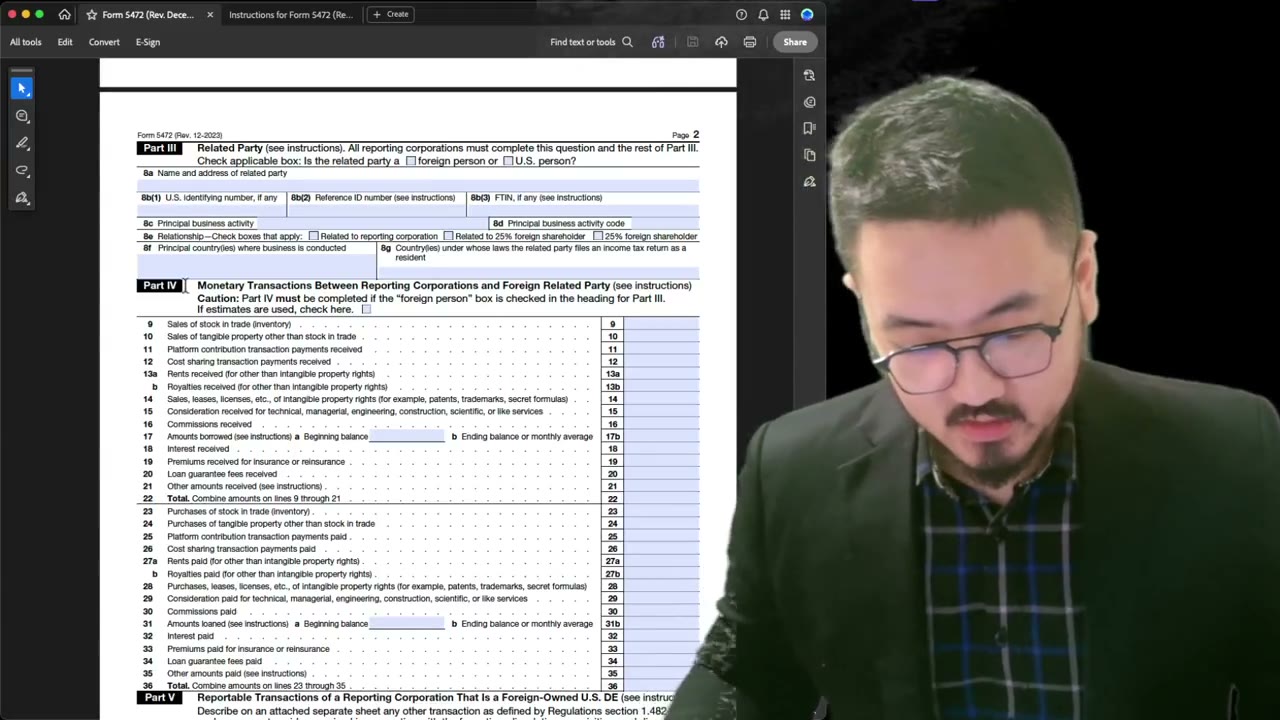

- **Capital contribution**: owner pays in funds (formation fee, working capital injection, expense reimbursement converted to capital). Reported as an inflow to the LLC from the related party (you).

- **Distribution**: LLC pays out funds back to the owner (distribution of profits, return of capital, dissolution proceeds). Reported as an outflow from the LLC to the related party.

Every dollar that moves between you and the LLC fits one of these two buckets, plus the loan/interest bucket if you've structured anything as a loan.

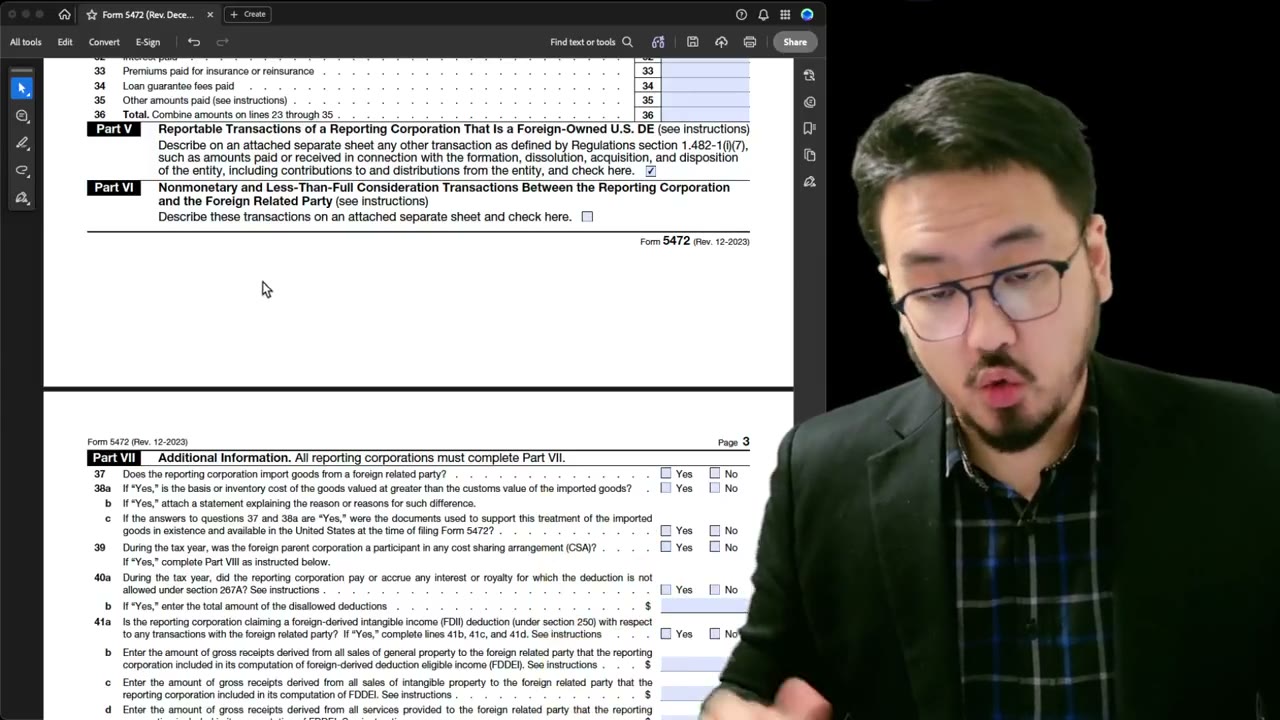

Dissolution Payments Are Reportable Too

If the LLC is dissolved during the tax year, the final liquidating distribution back to the owner is a reportable transaction. This is the last transaction the LLC ever has — and it's often the largest, because dissolution typically returns all remaining assets to the owner.

Report it under "distribution" in your supplementary attachment, with the dollar amount and the date of dissolution. The IRS uses this to confirm the LLC's lifecycle: it was formed (contributions reported in earlier years), it operated (whatever transactions in interim years), and it dissolved (final distribution in the final year). The cycle should be balanced and traceable across years.

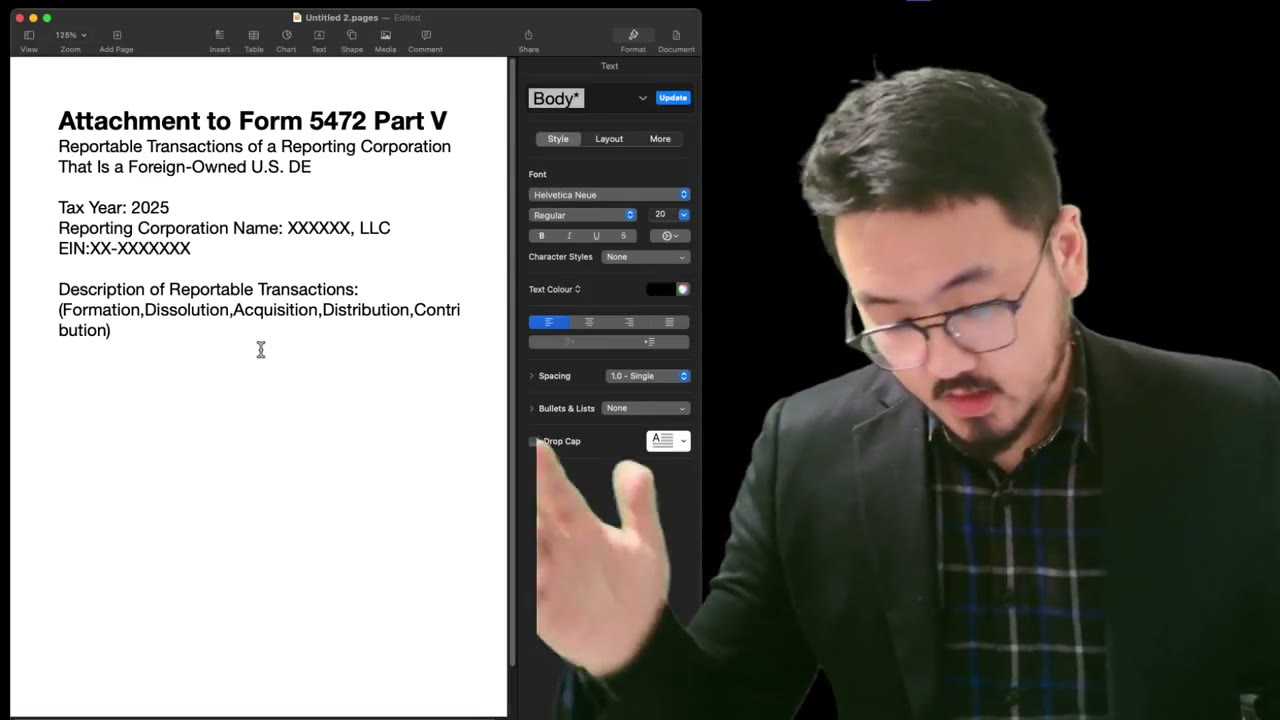

Describe Each Transaction Clearly

For each reportable transaction in the attachment, include:

- **Date** of the transaction - **Type** (contribution, distribution, loan, etc.) - **Dollar amount** - **Brief description** of what triggered it (e.g., "capital contribution at formation," "distribution of excess working capital," "dissolution payment")

Dates matter. The IRS sometimes asks for the timing within the year because tax treatment can vary (mid-year contributions vs. year-end distributions, etc.).

A Worked Example: Owner Contributes, Then Distributes

Setup: foreign owner forms a Delaware LLC in March 2025. Contributes $100,000 in startup capital. By October, the LLC has experienced operations and the owner decides to distribute $20,000 back to themselves.

Form 5472 disclosure (in the attachment):

Transaction 1: Capital contribution. Date: 2025-03-15. Amount: $100,000 USD. Description: "Initial capital contribution by sole foreign owner [Name] to LLC operating account at formation."

Transaction 2: Distribution. Date: 2025-10-22. Amount: $20,000 USD. Description: "Distribution of excess working capital to sole foreign owner [Name]."

This level of detail makes the cross-border flow comprehensible to the IRS reviewer. Both legs are disclosed, both with date/amount/description.

Capital Contribution vs. Loan — Pick One

When you advance funds to the LLC, you have a structural choice: treat it as a capital contribution (equity) or as a loan (debt). Most foreign owners prefer capital contribution because it's simpler — no interest, no repayment schedule, no separate documentation.

Loans require: market-rate interest (the IRS's Applicable Federal Rate), formal loan documentation (promissory note), and consistent treatment over the loan life. If you informally call something a loan but never charge interest or document repayment, the IRS may reclassify it as a contribution anyway.

My suggestion: default to capital contribution unless you have a specific tax reason to prefer the loan structure (often related to future repayment without distribution tax consequences). Ask your CPA when in doubt.

Tell the Story, Don't Just List

The attachment's purpose is narrative disclosure. Don't just list transactions in a table — explain them in context. The IRS reviewer needs to understand: what kind of business is this LLC, who is the foreign owner, what was the relationship between the transactions and the business, was anything unusual happening (formation, dissolution, acquisition, major investment).

For a routine single-member LLC, the narrative is short and uneventful. For complex scenarios, the narrative is longer and more detailed. Either way, the narrative is what makes the disclosure complete in the IRS's view.

Frequently Asked Questions

What if I made small ongoing contributions throughout the year (e.g., paying monthly fees)?

Summarize them in the attachment as a single line: "During tax year 2025, the owner paid registered agent fees totaling $200, treated as capital contributions." Or list each transaction if you want maximum detail. Both are acceptable.

Should I categorize informal owner-funded expenses as loans or contributions?

Capital contributions, almost always. Unless you intend (and document) repayment with market-rate interest, the IRS will reclassify informal "loans" as contributions anyway. Save the loan structure for situations where you genuinely plan repayment.

What if I distributed funds but the LLC didn't earn anything (it's a return of capital)?

Still report as a distribution in the attachment. Note in the description: "Distribution of contributed capital (no operating income generated)." The IRS understands return-of-capital distributions; just disclose them clearly so it's not mistaken for income distribution.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

1:55

1:55Pro Forma 1120 + Form 5472: Why Dormant LLCs Still Owe the $25,000 Filing

2:20

2:20Pro Forma 1120 + Form 5472: What Counts as a Reportable Transaction with Your LLC

4:55

4:55Form 5472 Part IV: Inflows, Outflows, and Where Capital Contributions Go

3:15

3:15Form 5472 §1.6038A-2 Attachment: Required Elements and Disclosure Examples

3:55

3:55Form 5472 Attachment: Document Structure, Treasury Regulation Citation, Signature

5:15

5:15