Installment Sale Interest and Ineligible Property Guide (2025-2026)

Installment sale reporting path

How gain from a sale paid over time is reported across years.

Confirm installment treatment

At least one payment is received after the year of sale.

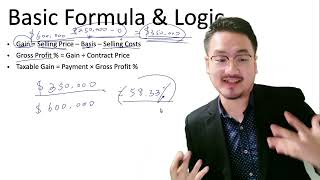

Compute the gross profit ratio

Determine the share of each payment that is taxable gain.

Report gain as payments arrive

Recognize the gain portion in each year a payment is received.

Track the remaining balance

Carry the outstanding installment obligation forward each year.

Key Takeaways

- Deferred payments alone do not make a sale eligible for the installment method.

- Marketable securities and loss sales are classic examples of ineligible installment treatment.

- Inadequate stated interest can be recharacterized as unstated interest or OID.

- The note terms should be tax-tested before the deal closes.

Not every deferred-payment sale qualifies for Form 6252 treatment

Publication 537 says the installment method cannot be used for stock or securities traded on an established securities market and cannot be used for sales at a loss. The publication also says inventory and dealer property are ineligible in the business-sale allocation rules. That means 'I got paid over time' is not the legal test.

The first question is always whether the property and the gain pattern qualify. Only then does payment timing begin to matter.

If the note does not charge enough interest, the tax law may write interest into it anyway

Publication 537 says that if an installment contract does not provide for adequate stated interest, part of the principal may be recharacterized as interest. Under section 483 this becomes unstated interest, and under section 1274 it can become original issue discount. The seller must reduce the stated selling price and increase interest income accordingly.

That means a low-interest note does not usually convert interest into capital gain. It often just creates recharacterization work.

The cash-flow schedule and the tax schedule should be built together

When founders negotiate private notes, they often model only closing cash and future installments. A better process models principal, stated interest, potential unstated-interest adjustments, and whether any property class is barred from installment treatment in the first place. That prevents the common mistake of closing a commercial deal whose tax reporting story was never actually tested.

Form 6252 works best when the note, the asset class, and the tax characterization all agree from day one.

Frequently Asked Questions

Can I report a public-stock sale on Form 6252 just because I received payments over time?

No. Publication 537 says stock or securities traded on an established securities market cannot use the installment method.

What if my installment note charges very little interest?

Publication 537 says part of the principal may be recharacterized as interest under the unstated-interest or OID rules.

Can a loss sale be reported on the installment method?

No. Publication 537 says sales at a loss are not reported on the installment method and the loss is taken in the year of sale if otherwise deductible.

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Installment Sales (Form 6252)

Form 6252 Business Sale Allocation Guide

Form 6252 Business Sale Allocation Guide (2025-2026)

Form 6252 Related-Party Second Sale Guide

Form 6252 Related-Party Second Sale Guide (2025-2026)

5:44

5:44Installment Sale Calculation: Step-by-Step Form 6252 Guide

4:18

4:18Installment Sales Introduction: Form 6252 Basics

Section 1446(f) Partnership Interest Sale Guide

Section 1446(f) Partnership Interest Sale Guide for Foreign Partners (2025-2026)

U.S. Sales Trips and ECI Risk for Foreign SaaS Founders