Form 6252 Business Sale Allocation Guide (2025-2026)

Installment sale reporting path

How gain from a sale paid over time is reported across years.

Confirm installment treatment

At least one payment is received after the year of sale.

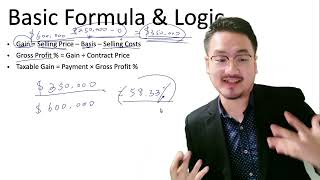

Compute the gross profit ratio

Determine the share of each payment that is taxable gain.

Report gain as payments arrive

Recognize the gain portion in each year a payment is received.

Track the remaining balance

Carry the outstanding installment obligation forward each year.

Key Takeaways

- A business sold under one contract must still be broken into separate asset classes for tax purposes.

- The residual method and asset-by-asset gain analysis drive the reporting.

- Inventory, losses, and depreciation recapture are not treated the same as eligible installment gain.

- Form 6252 should be supported by a detailed sale-allocation workpaper.

A business sale on installments is never just one asset sold slowly

Publication 537 says the installment sale of an entire business for one overall price under a single contract is not the sale of a single asset. It also says the residual method must be used to allocate the sale price among the business assets. That means founders selling a company or a business line cannot compute one gross-profit percentage across everything and call it finished.

The contract may have one headline price, but the tax treatment is built asset by asset.

Allocation decides which pieces can use the installment method and which cannot

Publication 537 says the seller must allocate selling price and payments among assets sold at a loss, assets eligible for the installment method, and assets ineligible for the installment method such as inventory and dealer property. The same publication also says depreciation recapture is reported in full in the year of sale, even if the payments arrive over time.

That is why business-sale calculations often surprise founders who expected all gain to spread across the note.

The right workpaper combines the asset schedule, section 1060 logic, and the payment stream

The tax file should show how the parties allocated the price, which assets are subject to ordinary-income recapture, and which remaining gain actually qualifies for installment reporting on Form 6252. When the books, purchase agreement, and tax return tell different allocation stories, later controversy becomes much more likely.

For a foreign founder selling a U.S. operation, this allocation workpaper is often the difference between an orderly exit and a messy amended-return season.

Frequently Asked Questions

Can I treat the sale of my entire business as one installment asset?

No. Publication 537 says the installment sale of an entire business is not the sale of a single asset and the price must be allocated among the business assets.

Does depreciation recapture stay on the installment method too?

No. Publication 537 says depreciation recapture is reported in full in the year of sale, even if installment payments continue later.

Does inventory qualify for installment-method treatment in a business sale?

No. Publication 537 lists inventory among the ineligible asset classes in the allocation analysis.

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Installment Sales (Form 6252)

Form 6252 Related-Party Second Sale Guide

Form 6252 Related-Party Second Sale Guide (2025-2026)

Installment Sale Interest and Ineligible Property Guide

Installment Sale Interest and Ineligible Property Guide (2025-2026)

5:44

5:44Installment Sale Calculation: Step-by-Step Form 6252 Guide

4:18

4:18Installment Sales Introduction: Form 6252 Basics

U.S. Sales Trips and ECI Risk for Foreign SaaS Founders

U.S. Sales Trips and ECI Risk for Foreign SaaS Founders (2025-2026)

Creator Merchandise Sales Through a Foreign-Owned LLC