Form 6252 Related-Party Second Sale Guide (2025-2026)

Installment sale reporting path

How gain from a sale paid over time is reported across years.

Confirm installment treatment

At least one payment is received after the year of sale.

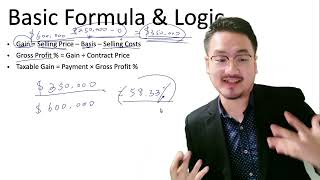

Compute the gross profit ratio

Determine the share of each payment that is taxable gain.

Report gain as payments arrive

Recognize the gain portion in each year a payment is received.

Track the remaining balance

Carry the outstanding installment obligation forward each year.

Key Takeaways

- A related person's resale within two years can accelerate gain back to the original seller.

- Controlled entities count in the related-person analysis.

- Depreciable property sold to certain related persons often cannot use installment reporting at all.

- The ownership and control map should be checked before the installment note is signed.

Related-party installment sales carry a built-in anti-deferral rule

Publication 537 says that when property is sold to a related person on the installment method and that related person later disposes of the property before all payments are made and within two years of the first sale, the original seller may have to treat the amount realized on the second disposition as if it had been received at that time. This is the second-disposition rule.

The rule exists because family or controlled-entity structures otherwise make it too easy to defer gain without a real economic delay.

Depreciable property sold to certain related persons is even riskier

Publication 537 says that sales of depreciable property to certain related persons generally cannot be reported on the installment method at all, unless the seller can show that no significant tax-deferral benefit will be derived and tax avoidance was not one of the principal purposes of the sale. That is a much harder factual lane than people assume.

In founder groups moving assets among entities, this rule often shuts down the hoped-for installment treatment before the note is even drafted.

Control relationships should be mapped before the agreement is signed

Publication 537 includes controlled entities in its related-person definitions. So the issue is not limited to immediate family members. Ownership graphs, manager control, and related entities all need to be tested before the seller relies on Form 6252.

If the ownership map is built after the transaction rather than before it, the tax memo is already late.

Frequently Asked Questions

What happens if my related buyer resells the property before paying me in full?

Publication 537 says you may have to treat part or all of the amount realized on that second sale as received by you at the time of the second disposition.

How long does the second-disposition related-party rule stay dangerous?

Publication 537 says the key period is within two years of the first disposition, subject to the rule's specific exceptions.

Can depreciable property be sold to a related person on the installment method?

Usually not. Publication 537 says those sales generally cannot use the installment method unless the seller can prove no significant tax-deferral purpose is present.

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Need Help Filing?

Contact us with your situation and we'll point you to the right path

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Installment Sales (Form 6252)

Form 6252 Business Sale Allocation Guide

Form 6252 Business Sale Allocation Guide (2025-2026)

Installment Sale Interest and Ineligible Property Guide

Installment Sale Interest and Ineligible Property Guide (2025-2026)

5:44

5:44Installment Sale Calculation: Step-by-Step Form 6252 Guide

4:18

4:18Installment Sales Introduction: Form 6252 Basics

Separate Form 5472 for Each Related Party Guide

Separate Form 5472 for Each Related Party Guide (2025-2026)

Cloud Folder Records Guide for Related-Party Transactions