What Is a Short Tax Year? Definition & Basics for Form 1120 Filers

Key Takeaways

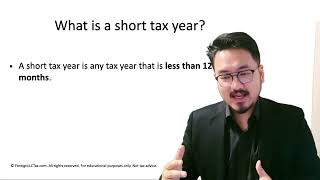

- A short tax year is any tax year less than 12 months

- First year, final year (dissolution), and accounting period change are the three common triggers

- Form 5472 + pro forma 1120 obligation applies to short years exactly like full years

- Due date is 15th day of 4th month after the short year's end (plus extensions)

- Always fill the tax year beginning + ending dates on Form 1120 — don't just check 'calendar year'

When Tax Year ≠ 12 Months

Most tax returns cover a full 12-month period — typically January 1 through December 31 for calendar-year filers. But the IRS sometimes requires a tax return for a shorter period. That shorter period is called a "short tax year."

A short tax year is any tax year less than 12 months. The IRS treats short-year returns differently from regular returns in subtle but important ways: due date calculation, election validity periods, and how income/deductions are annualized.

Why This Comes Up for Foreign-Owned LLCs

Foreign-owned LLCs hit short tax years in three common scenarios:

1. First year of operation. If you formed your LLC mid-year (e.g., October 15, 2025), your first tax year runs October 15 - December 31, 2025 — only 78 days. That's a short tax year.

2. Final year. If you dissolve the LLC mid-year (e.g., June 30, 2026), the final tax year runs January 1 - June 30, 2026. That's a short tax year.

3. Accounting period change. If you change from a calendar year to a fiscal year (or vice versa), the transition year is a short tax year. This is rare for foreign-owned LLCs but happens occasionally.

How a Short Year Affects Form 5472 Filing

The Form 5472 + pro forma 1120 obligation applies to short tax years the same as full tax years. If your LLC existed for 78 days in 2025, you still file Form 5472 for those 78 days. The §6038A $25,000 penalty applies if you don't.

The due date for a short-year return is based on the short year's end date. If your short year ends June 30, the return is due by the 15th day of the 4th month after — so October 15. If the foreign-owner extension applies, due dates shift accordingly.

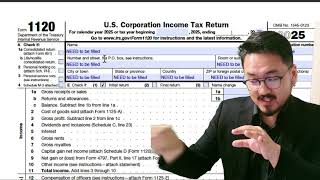

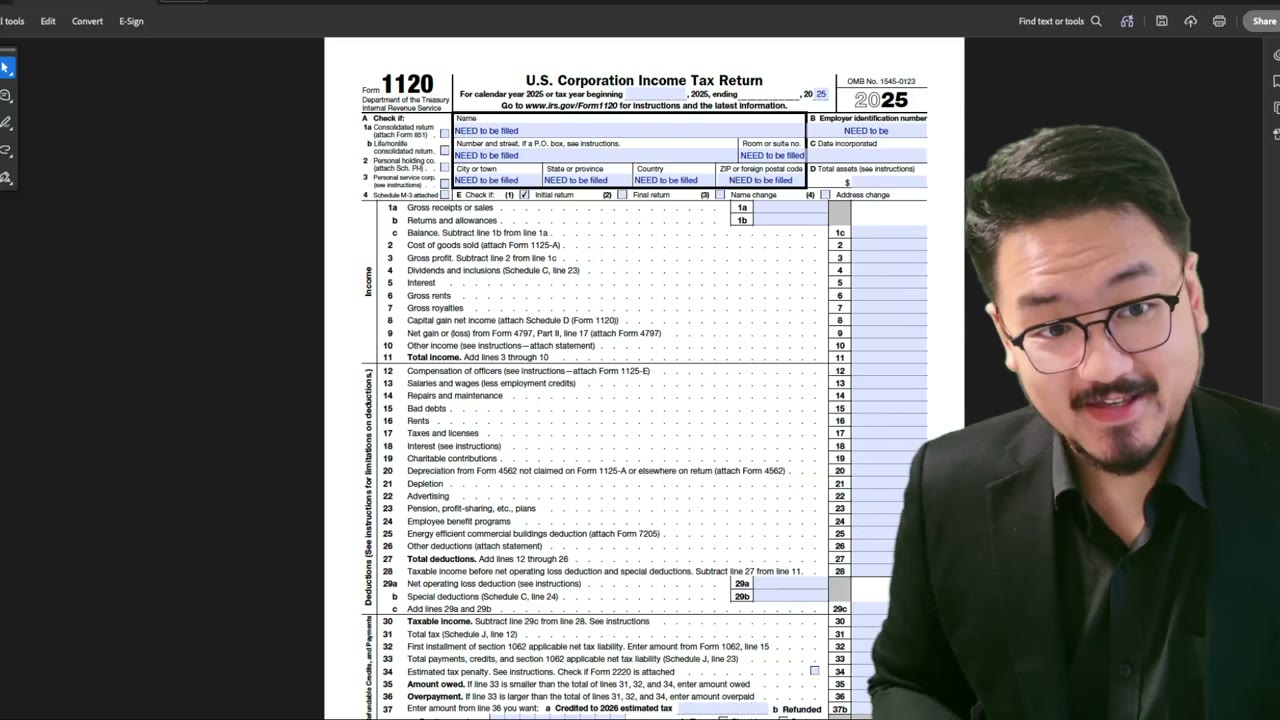

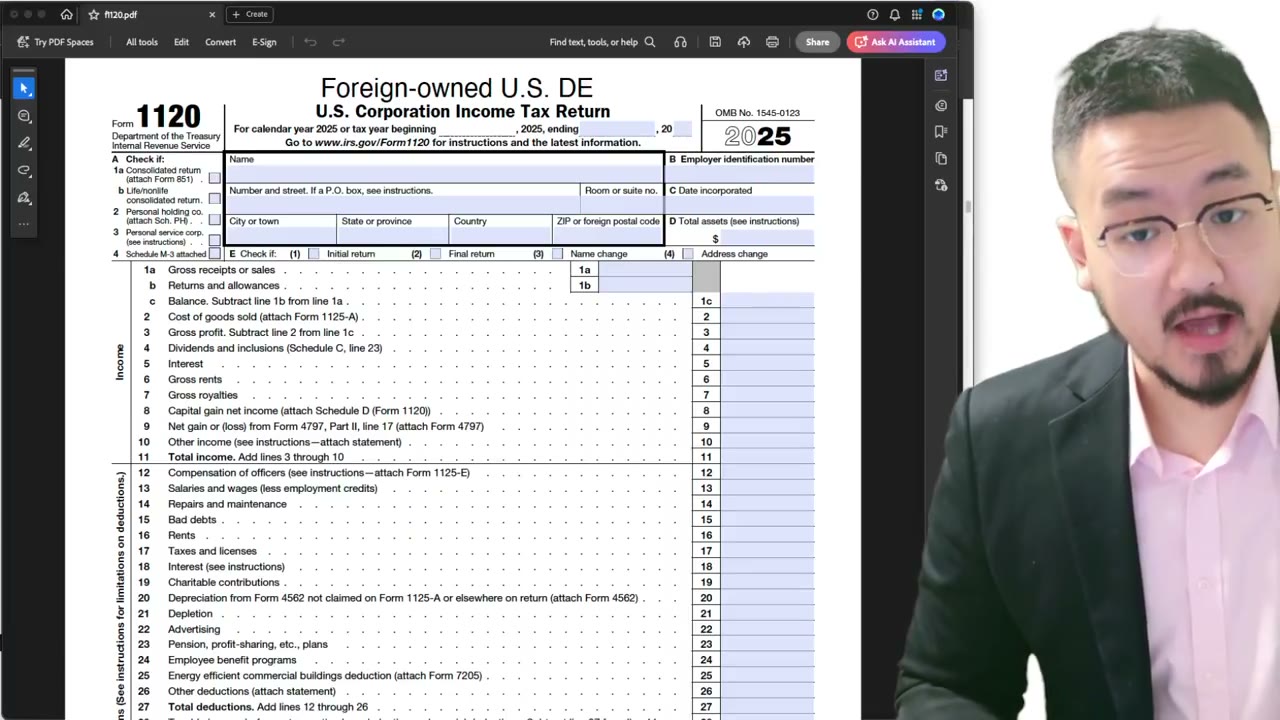

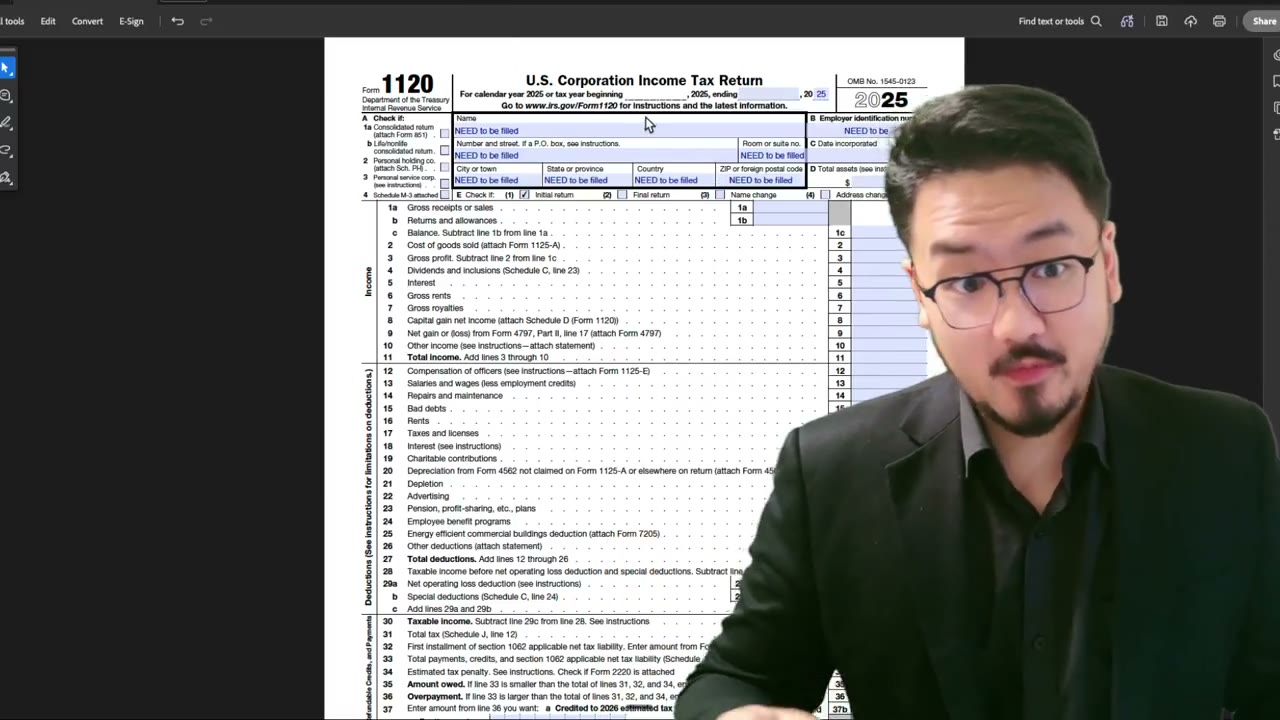

The tax year fields on Form 1120 and Form 5472 must reflect the actual short period. On Form 1120, that's the "For calendar year [YEAR], or tax year beginning [DATE], and ending [DATE]" line at the top of page 1. Fill the beginning and ending dates with the short period.

Three Real Scenarios

Scenario A — First year: LLC formed October 15, 2025. Tax year: October 15 - December 31, 2025 (78 days). File Form 5472 + pro forma 1120 by April 15, 2026 (the standard April 15 + extensions).

Scenario B — Dissolution year: LLC formed January 2020, dissolved June 30, 2026. Final tax year: January 1 - June 30, 2026 (181 days). File the final-year Form 5472 + pro forma 1120 by October 15, 2026 (15th day of 4th month after June 30).

Scenario C — Accounting period change: LLC operated on a calendar year for years; now switches to a fiscal year ending September 30. Transition tax year: January 1 - September 30 (273 days, less than 12 months). Requires IRS approval via Form 1128 (Application to Adopt, Change, or Retain a Tax Year), filed in advance. After approval, the short year filing proceeds normally.

Frequently Asked Questions

Is my first-year filing always a short tax year?

Yes, unless you happened to form your LLC on January 1 of a given year. Any other formation date during the year creates a short first tax year.

Do I need to annualize income for a short year?

For a pro forma Form 1120 (no income, no tax), annualization is moot — you have no income to annualize. For real corporate returns with income, IRC §443 may require annualization in some scenarios. Foreign-owned DEs filing pro forma do NOT need to annualize.

Does the §6038A $25,000 penalty apply to short-year filings?

Yes. The penalty is per Form 5472 per year — and a short tax year is a year for §6038A purposes. Missing a short-year filing triggers the same exposure as missing a full-year filing.

What if I had no transactions during the short year?

Filing is still required. Form 5472 must be filed even with zero reportable transactions, as long as the LLC existed during any portion of the year. The penalty applies to the failure to file, not to the failure to have transactions.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:00

2:00Short Tax Year Mechanics: Annualization & Reporting Implications

2:15

2:15When Does a Short Tax Year Happen? Triggers Explained for LLC Filers

2:30

2:30Form 1120 Tax Year Demo: Beginning, Ending & Short-Year Filings

2:56

2:56Form 1120 Short Tax Year: How to Enter Beginning and Ending Dates (Foreign Owners)

1:55

1:55Form 1120 Short Tax Year: How to Fill the Begin/End Dates and Initial Return Box

1:25

1:25