Pro Forma 1120 + Form 5472: What Counts as a Reportable Transaction with Your LLC

Key Takeaways

- For a single-member foreign-owned LLC, the owner is automatically the foreign related party

- Common "hidden" transactions: state franchise tax paid personally, registered agent fees, formation costs

- Capital contributions are reportable regardless of size — even $250 for Atlas formation counts

- Loans between owner and LLC are reportable and tracked separately from contributions (different tax treatment)

- Reimbursements (owner pays vendor, LLC repays) create reportable transactions in both directions

Form 5472's Real Purpose: Tracking Transactions With Related Parties

Form 5472 isn't about the LLC itself or its income. It's about transactions between the U.S. entity and any foreign related party. For a single-member LLC, the foreign owner is automatically the related party — because you own 100% of an entity, you are by definition related to it.

The form asks: what flowed between you and the LLC during the tax year? Money in (capital contributions, loans). Money out (distributions, loan repayments). Services provided. Reimbursements. Asset transfers. Each direction of flow is itemized so the IRS has visibility into the financial relationship.

Why Single-Member LLCs Always Have a Related Party

Some foreign owners think they don't have a "related party" because they're an individual, not another company. That's wrong. Under IRC §6038A, the owner of a disregarded entity is automatically a related party — the very fact of sole ownership creates the relation.

If you're a foreign person who owns 100% of a Delaware LLC, you are the foreign related party for that LLC's Form 5472. Every transaction between you and the LLC is reportable. There's no escape via the "I'm just one person" argument.

What If the LLC Has No Transactions?

In practice, some clients have no real business operations. They formed an LLC to hold intellectual property, or to be ready when a future project starts, or to maintain a U.S. business presence without immediate use. "No transactions" feels like the natural default.

But watch carefully — most LLCs that look transaction-free actually have some. The most common ones:

- Paying state franchise tax (Delaware annual fee, California franchise tax, etc.) — if you paid it from personal funds, that's a reimbursable expense, and either a reimbursement or a capital contribution depending on whether the LLC paid you back - Annual registered agent fees — same logic - LLC formation costs (Atlas, doola, Firstbase fees) — paid by the owner before the LLC existed; almost always a capital contribution - Bank account maintenance fees — if paid from a personal card

These are all reportable transactions, even though they feel like background noise.

Capital Contributions Are Reportable Transactions

When you first fund the LLC — pay the formation fee, deposit startup capital into the LLC's bank account, contribute equipment — that's a capital contribution from a foreign related party. Reportable.

The amount might be tiny ($250 for Atlas formation) or large ($50,000 for working capital), but the requirement to report doesn't depend on the size. Even a single capital contribution of $300 triggers the obligation to file Form 5472 with that contribution documented.

Loans Between Owner and LLC Are Reportable Too

If you lend money to the LLC (instead of contributing it as capital), the loan is a reportable transaction. The principal advance, the interest accruals, and any repayments — all reportable, in both directions.

Loans are technically distinct from capital contributions: loans must be paid back, capital contributions are equity. For tax purposes (especially eventual exit or dissolution), the distinction matters. The IRS expects the form to reflect the actual nature of the transaction — don't label a loan as a contribution to simplify the paperwork.

Reimbursements (Owner Pays, LLC Reimburses)

If you took a business trip for the LLC, paid for it on your personal credit card, and then the LLC reimbursed you from its bank account, that reimbursement is a reportable transaction. The flow is: owner advances funds (could be capital contribution or implicit loan) → LLC repays.

Similarly, if you paid a vendor on the LLC's behalf because the LLC didn't have a bank account yet, then the LLC later reimburses you, that's a reportable transaction loop. Document both legs (the initial advance and the reimbursement).

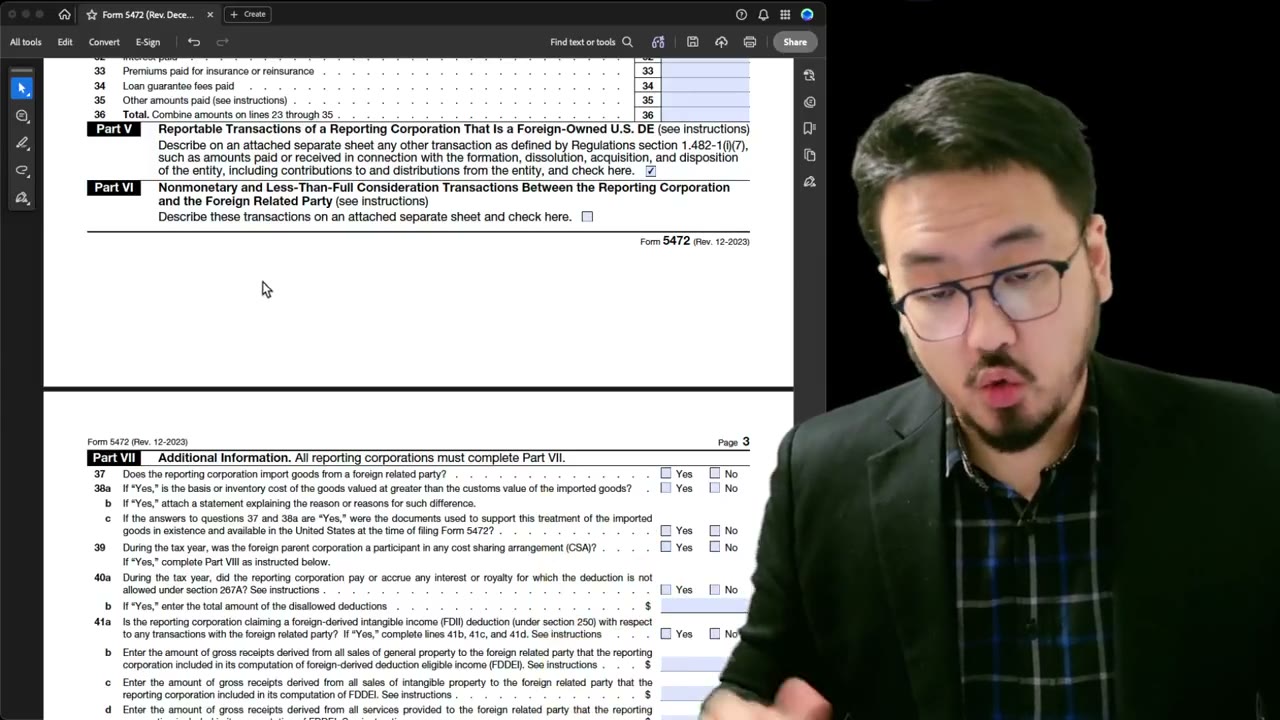

The Long List of Reportable Categories

Form 5472 Part IV lists the categories explicitly: sales/purchases of stock in trade, sales/purchases of tangible property, rents, royalties, interest, premiums received/paid, commissions, technical/managerial services, cost-sharing payments, platform contribution payments, and the catch-all "other amounts."

For a typical single-member LLC, most lines are zero. The active lines are usually capital contributions, distributions, and any inter-company services. But check every line — missing one because you assumed it was irrelevant is how filings get incomplete.

Frequently Asked Questions

I haven't paid the LLC anything this year. Do I still need to file?

Almost certainly yes. Check for hidden transactions: state franchise tax, registered agent fees, any expense you paid personally that benefited the LLC. If literally zero (no formation costs, no annual fees, no expenses), the filing is still required to declare zero — see the next video on this.

Should I categorize a $300 vendor payment as a capital contribution or a loan?

Default to capital contribution unless you intend (and document) the LLC to repay you. Loans require interest at the applicable federal rate, formal documentation, and consistent repayment treatment — more complex than most foreign-owned LLCs want. Capital contribution is the simpler choice unless you have a reason to prefer the loan structure.

Are personal investment returns (dividends from the LLC's stock holdings) reportable transactions?

Distributions of those returns to the owner are reportable. The investment returns themselves stay inside the LLC and aren't separately reportable as related-party transactions — they're internal LLC income. The reportable event is when money moves between owner and LLC.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

Form 5472 Explained — What It Is, Who Must File, and How It Works

Form 5472 Explained: What It Is, Who Must File, and How It Works (2025-2026)

3:15

3:15Form 5472 §1.6038A-2 Attachment: Required Elements and Disclosure Examples

1:55

1:55Pro Forma 1120 + Form 5472: Why Dormant LLCs Still Owe the $25,000 Filing

1:30

1:30Why You Can't E-File Form 5472 + Pro Forma Form 1120 (IRS Reasons)

1:25

1:25Pro Forma 1120 + Form 5472: The Required Combo Filing for Foreign-Owned LLCs

2:10

2:10