Form 5472 Part IV: Inflows, Outflows, and Where Capital Contributions Go

Key Takeaways

- Part IV is mandatory if you marked any foreign related party in Part III (which all foreign-owned LLCs do)

- Top half = inflows (money received by corporation); bottom half = outflows (money paid by corporation)

- Most common single-member LLC line: capital contributions go on Line 15 (other amounts received); distributions on Line 29

- Estimated amounts within ~70–125% of actual are OK — check the estimated box if using approximations

- Even a $250 formation fee is a reportable transaction — minimum threshold is essentially zero

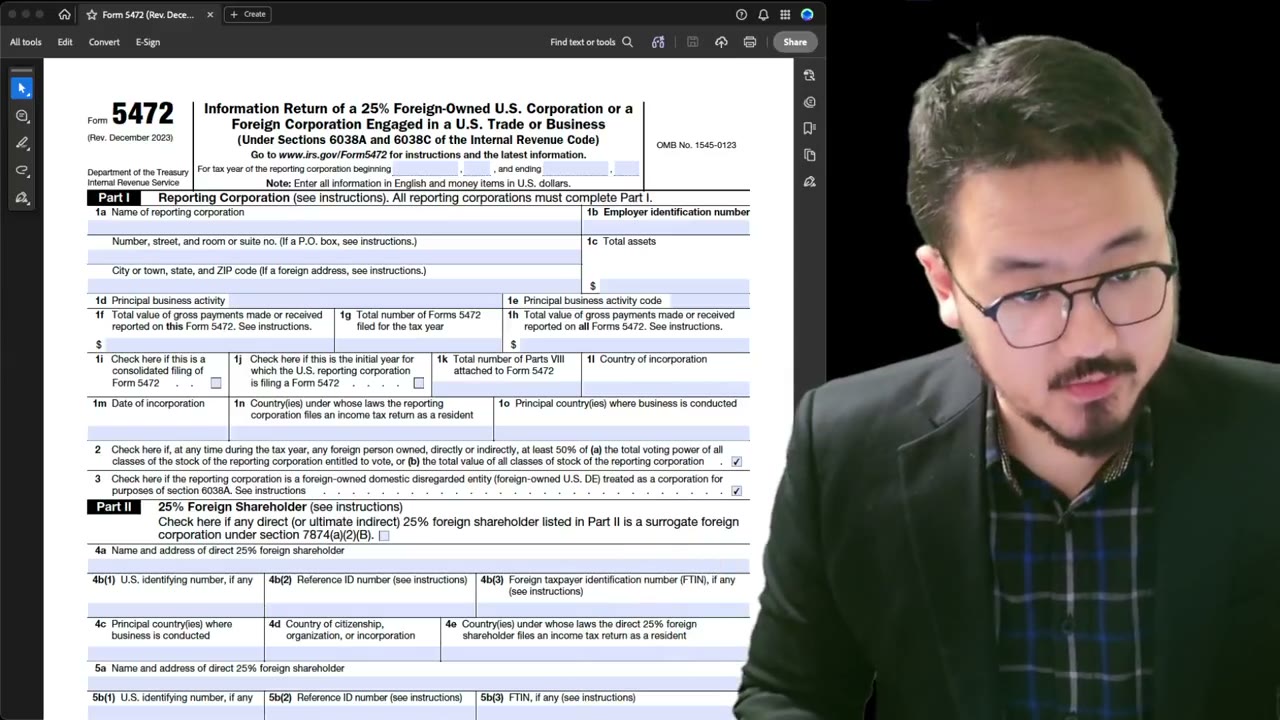

Part IV: Reportable Transactions — Inflows and Outflows

Form 5472 Part IV is where the actual money flow gets reported. It's split into two halves: inflows (money the reporting corporation received from the related party) and outflows (money the corporation paid to the related party). Each transaction type has its own line, and totals get computed at the bottom of each half.

Caution: Part IV Is Mandatory If the Foreign Person Box Is Checked

The instructions are explicit: "Part IV must be completed if the foreign person box is checked in the heading of Part III." Translation: if you identified any foreign related party in Part III (which you have, as a foreign-owned single-member LLC), Part IV is mandatory.

This catches first-time filers who think "I had no business, no income, no real transactions, so I'll skip Part IV." Wrong. The capital contribution to form the LLC counts. The state franchise tax paid by the owner counts. Any transaction at all counts. Part IV is mandatory; the only valid "zero" Part IV is if there were literally no transactions of any kind.

Estimated Amounts Checkbox

If you're using estimated values (because exact amounts weren't trackable, for example for very minor reimbursements), check the "estimated" box. The IRS allows estimates within a range (roughly 70%–125% of the actual amount) without penalty.

If you can determine the exact value, do — but for small ancillary transactions where exact reconciliation isn't worth the time, an estimate within range is acceptable. The checkbox signals to the IRS that the value is approximate.

Inflow Lines (Top Half of Part IV)

Inflows are transactions where the reporting corporation RECEIVED something from the related party. The line items:

- **Line 1**: Sales of stock in trade (the corporation sold inventory to the related party) - **Line 2**: Sales of tangible property other than stock in trade - **Line 3a/3b**: Platform contribution transaction payments / cost sharing payments received - **Line 4–10**: Rents, royalties, sales of intangible property, technical services, etc. - **Line 11**: Commissions received - **Line 12**: Amounts borrowed (loans from the related party to the corporation) - **Line 13–14**: Interest received, premiums received - **Line 15**: Other amounts received - **Line 16**: Total inflows (sum of lines 1–15)

For most single-member foreign-owned LLCs, the active inflow line is Line 12 (amounts borrowed) if the owner contributed capital that's structured as a loan, or Line 15 (other amounts received) for capital contributions that aren't loans.

Beginning and Ending Balances for Loans

Line 12 (amounts borrowed) is a balance-type field — you report the beginning balance, ending balance, and (often) the highest balance during the year. Example: if the LLC started the year owing the owner $0 in loans, and at year-end owes $600,000 (because the owner advanced funds during the year), report 0 beginning, 600,000 ending.

Average balance or interest computations may apply depending on the loan terms. Consult the Form 5472 instructions for the specific calculation.

Outflow Lines (Bottom Half of Part IV)

Outflows mirror the inflows but in the opposite direction. The corporation PAID something to the related party:

- **Line 17**: Purchases of stock in trade (corporation bought inventory from related party) - **Line 18–24**: Purchases of tangible/intangible property, rents paid, royalties paid, services paid, etc. - **Line 25**: Commissions paid - **Line 26**: Amounts loaned (corporation lent funds to related party) - **Line 27–28**: Interest paid, premiums paid - **Line 29**: Other amounts paid - **Line 30**: Total outflows (sum of lines 17–29)

The most common outflow line for single-member LLCs: Line 29 (other amounts paid) for distributions back to the owner.

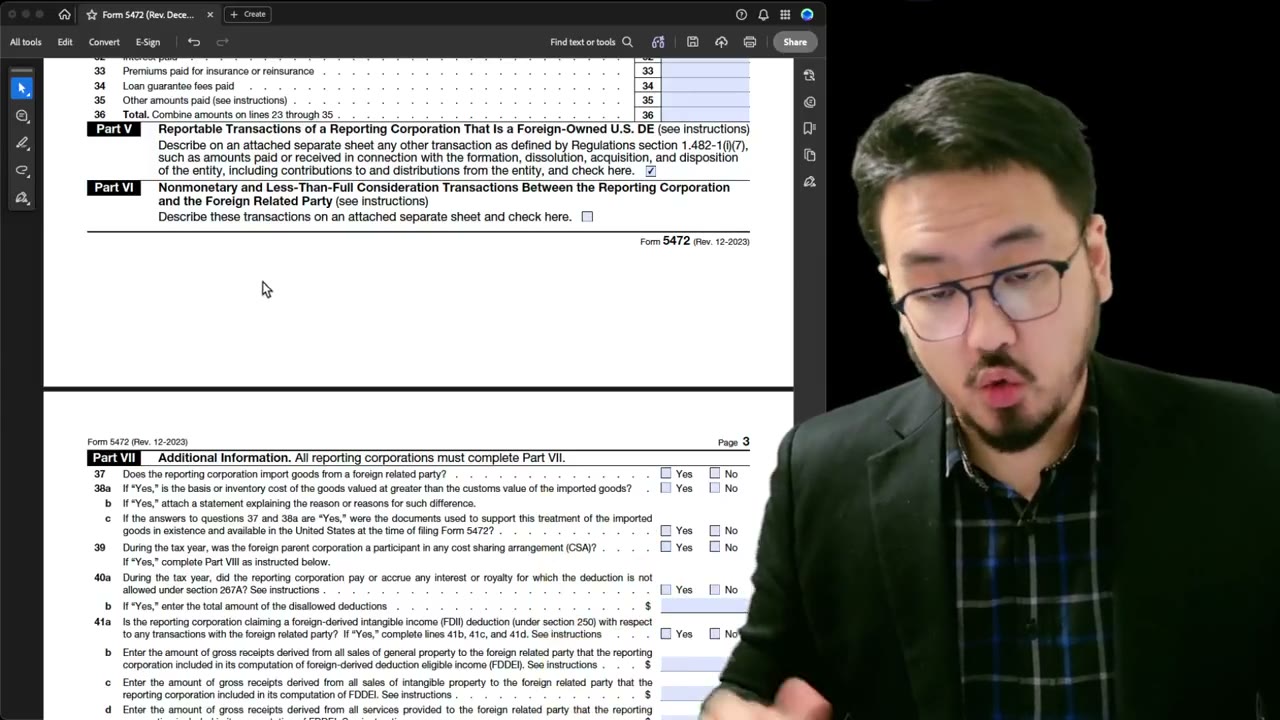

What Counts as Reportable in Each Category

The categories require some judgment. Examples that come up often:

- **Owner pays state franchise tax personally → contribution-type inflow**: report under Line 15 (other amounts received) with the description "capital contribution for franchise tax payment" - **LLC distributes profits or excess capital back to owner → outflow**: Line 29 (other amounts paid), described as "distribution to sole owner" - **Owner provides personal services to the LLC without compensation → typically not reportable** unless there's a formal agreement - **Reimbursement of expenses → inflow when owner advances + outflow when LLC reimburses**: both legs of the loop are reported separately

Why the High Penalty: This Is the Sensitive Part

The reason Form 5472's penalties are so steep is precisely because Part IV is the sensitive data — cross-border financial flows between a foreign individual and a U.S. entity. The IRS wants to see every dollar in and out, accurately classified, because that's the data point that could later signal transfer pricing issues, beneficial ownership concealment, or sanctions evasion.

Which is why "didn't fill Part IV because I forgot" or "my LLC was sleepy" don't get you off the hook. Even a $250 formation fee paid by the owner is a reportable transaction that must appear in Part IV (under Line 15, other amounts received). The minimum threshold for reportability is essentially zero.

Frequently Asked Questions

Where do I report a $300 capital contribution for state franchise tax?

Line 15 (other amounts received) on Part IV, with a description in the attachment like "Capital contribution by sole owner to cover Delaware franchise tax." The amount is $300; the related party is yourself.

How do I report a loan vs. a capital contribution?

Loans go on Line 12 (amounts borrowed) with beginning/ending balances. Capital contributions go on Line 15 (other amounts received) with the transaction amount. The classification depends on whether you intend (and document) repayment — loans must have repayment terms; contributions don't.

What if I have no transactions whatsoever — do I still file Part IV?

Yes. Fill the form with zeros in every line and check no "estimated" box. The IRS expects to see Part IV completed even with zeros to confirm the entity reviewed the categories. A blank Part IV looks like an incomplete filing.

IRS Form 5472 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file your foreign-owned LLC return?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 5472 & Foreign-Owned LLCs

2:20

2:20Pro Forma 1120 + Form 5472: What Counts as a Reportable Transaction with Your LLC

5:00

5:00Form 5472 Attachment: Capital Contribution vs. Loan, Distribution, Dissolution Payments

2:10

2:10Form 5472: Why the §1.6038A-2 Attachment Is Mandatory (Don't Skip)

3:15

3:15Form 5472 §1.6038A-2 Attachment: Required Elements and Disclosure Examples

3:55

3:55Form 5472 Attachment: Document Structure, Treasury Regulation Citation, Signature

Form 5472 Field-by-Field Guide for Foreign-Owned LLCs