When Does a Short Tax Year Happen? Triggers Explained for LLC Filers

Key Takeaways

- First-year filings are almost always short tax years — the formation date anchors the start

- Dissolution mid-year creates a short final tax year — check 'Final return' on Form 1120

- Accounting period changes require Form 1128 pre-approval — retroactive changes not allowed

- S-Corp election termination from adding a foreign owner triggers a short year (rare scenario)

- Each trigger requires different documentation — keep formation, dissolution, or Form 1128 paperwork ready for IRS

Trigger 1: First Year of Operation

Your LLC's first tax year almost always starts mid-year, making it a short tax year by definition. The first tax year begins on the date your Articles of Organization were filed with the state (the official formation date) and ends on the last day of your chosen tax year.

For most foreign-owned LLCs (calendar-year filers), the first tax year runs from the formation date through December 31. If you formed on October 15, 2025, your first tax year is October 15 - December 31, 2025 — 78 days.

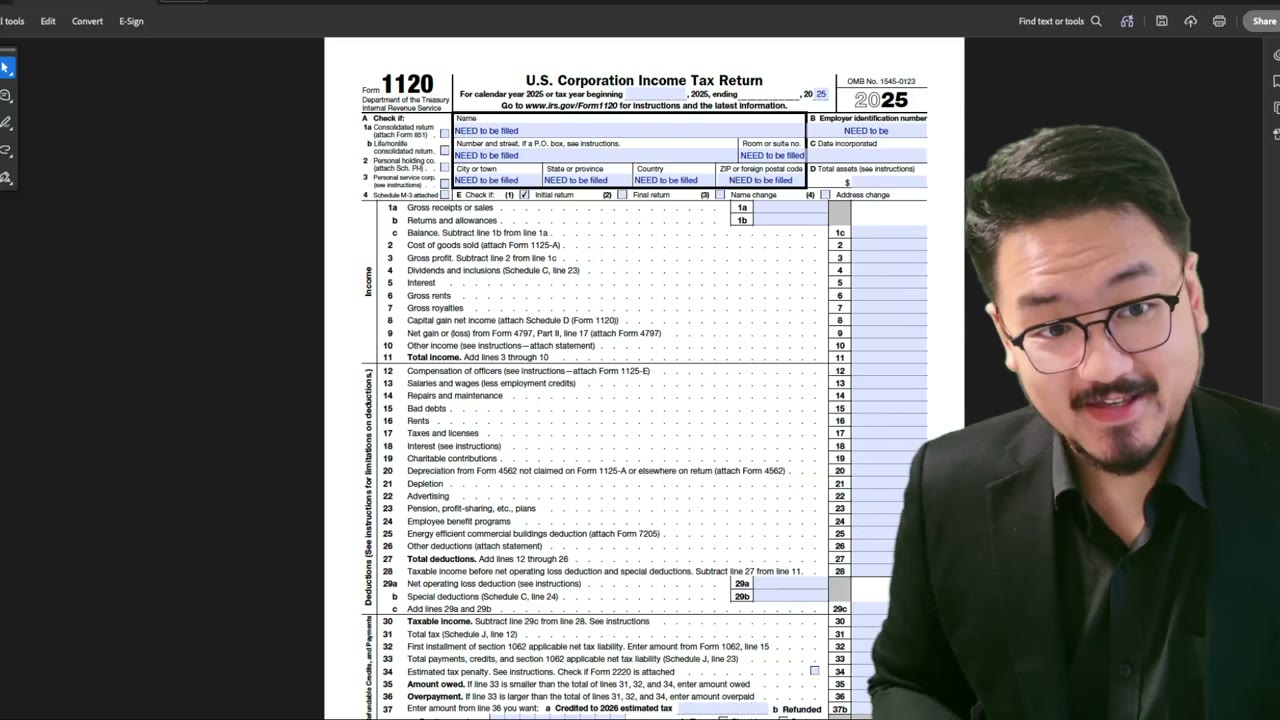

This is so common that most CPAs treat it as the default expectation. Form 1120 has Item E ("Date incorporated") specifically to anchor the start of the first tax year.

Trigger 2: Dissolution

If you dissolve your LLC mid-year, the final tax year runs from January 1 (or the prior year-end) through the dissolution date. Dissolution must be a formal act — filing Articles of Dissolution with the state where the LLC was formed, plus IRS notification.

The final tax year filing has special markings on Form 1120: check the "Final return" box at the top of page 1. The Form 5472 final-year filing should reflect any final reportable transactions (final capital distributions, debt cancellations, wind-down expenses).

Many foreign owners dissolve mid-year when they pivot to a different business structure (move to a C-Corp), wind down operations, or close down due to changed circumstances. The dissolution year is a short tax year by definition.

Trigger 3: Accounting Period Change

If you change your accounting period (calendar year → fiscal year, or fiscal year ending in one month → fiscal year ending in another), the transition year is a short tax year covering the period between the old year-end and the new year-end.

Example: An LLC operating on calendar year 2024 (ending December 31). It wants to switch to a fiscal year ending September 30. The transition year runs January 1 - September 30, 2025 — 273 days. After that, the LLC operates on the new fiscal year.

Accounting period changes require IRS pre-approval via Form 1128 (Application to Adopt, Change, or Retain a Tax Year). The form must be filed in advance of the change; retroactive changes are not allowed. For foreign-owned LLCs, period changes are rare — most stick to the default calendar year. But if you need one (e.g., to align with a foreign parent's fiscal year), Form 1128 is the path.

Trigger 4: S-Corp Election Termination (Rare for Foreign-Owned LLCs)

If an LLC previously elected S-Corp status (Form 2553) and that election is terminated (involuntarily, e.g., by adding a foreign owner who's ineligible to be an S-Corp shareholder), a short tax year may apply.

This is rare for foreign-owned LLCs because foreign owners can't be S-Corp shareholders — so the LLC wouldn't be an S-Corp in the first place. The scenario typically arises only if a U.S. citizen-owned S-Corp transfers shares to a foreign owner, triggering immediate S-Corp termination and a short year for the entity.

If you're in this situation, get a CPA involved. The S-Corp termination short year is more complex than the other three triggers and has different filing implications (Form 1120-S transitioning to Form 1120 plus Form 5472).

Frequently Asked Questions

What's the most common short-year scenario for foreign-owned LLCs?

First-year filings. Almost every foreign-owned LLC has a short first tax year because formations rarely happen exactly on January 1. The first filing covers formation date through year-end.

Do I need to mark 'Initial return' on a first-year filing?

Yes, check the 'Initial return' box at the top of Form 1120. This tells the IRS this is the LLC's first filing. The 'Initial return' marking signals to processing that there's no prior-year data to compare against.

Can I avoid a short first year by waiting to file until December 31?

No. The tax year is defined by when the LLC was legally formed, not when you file the return. If your Articles of Organization were filed October 15, your first tax year started October 15 regardless of when you submit Form 5472. You can extend the due date with Form 7004, but the tax year itself is fixed.

Do all four triggers apply to foreign-owned LLCs?

Triggers 1-3 are common. Trigger 4 (S-Corp termination) is theoretical because foreign owners can't be S-Corp shareholders to begin with. If you're a U.S. partner in an S-Corp who transfers shares to a foreign person, get a CPA — the resulting termination has multiple compliance threads beyond just the short year.

IRS Form 1120 Instructions

Official IRS source on irs.gov

Listen on Spotify

Money & Tax Talk with Rippa — 5/5 rating

Never miss an IRS deadline

Get free email reminders for Form 5472, state annual reports, quarterly estimated tax, and OBBBA rule changes — built for foreign-owned LLC owners. No spam. Unsubscribe anytime.

We respect your privacy. No spam, ever.

Need to file Form 5472 + pro forma 1120?

Skip the CPA bill. Our guided wizard builds your IRS-ready filing package, step by step.

Includes its walkthrough video pack

Start filing →

Ask the AI tools, free

Tax Return Drafter, Catch-Up Planner, Form Reviewer, IRS Notice Decoder — purpose-built AI tools, no signup needed.

Free tier · BYOK Anthropic/OpenAI for power use

Browse tools →

Starting your foreign-owned LLC?

Vetted partners we use ourselves: doola & Firstbase for formation, Mercury for banking, Alohi for IRS faxing.

No-fluff recommendations, no Northwest

See partners →

More on Form 1120 Corporate Tax Return

2:00

2:00What Is a Short Tax Year? Definition & Basics for Form 1120 Filers

1:55

1:55Form 1120 Short Tax Year: How to Fill the Begin/End Dates and Initial Return Box

Form 1120 Initial, Final, and Short-Period Return Guide

Form 1120 Initial, Final, and Short-Period Return Guide (2025-2026)

2:00

2:00Short Tax Year Mechanics: Annualization & Reporting Implications

2:30

2:30Form 1120 Tax Year Demo: Beginning, Ending & Short-Year Filings

2:56

2:56